I started paying attention to Lorenzo because I kept noticing the same quiet pattern in crypto: every cycle, we build new ways to take risk, but the hard part is packaging that risk into something ordinary people can actually hold without living on a trading screen. Most “access” products in DeFi still assume you want to be your own hedge fund manager, stitching together vaults, perps, stables, and bridges and then pretending the glue is a strategy. When I first looked at Lorenzo’s On-Chain Traded Funds, what struck me wasn’t the yield pitch. It was the attempt to turn strategy itself into a clean object.

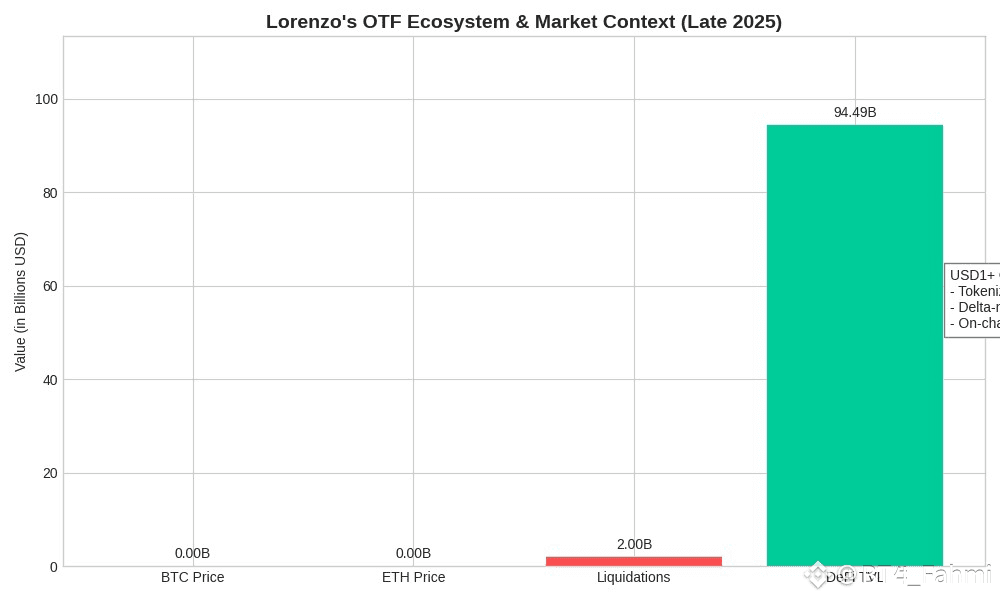

The timing helps explain why this feels different. Right now the market’s texture is jittery again. Bitcoin is around $91,451 today, after a sharp early-December selloff that pushed it under the high $80Ks intraday, and ETH is near $3,131. That kind of swing is not just a price chart story. It is a behavior story. Leverage builds up, liquidity thins, and then a weekend move forces everyone to pay attention at once. In late November, more than $2 billion in leveraged positions got wiped in a single 24-hour window, which is the kind of number that tells you this market still runs on crowded trades and mechanical exits.

Meanwhile DeFi’s own “confidence meter” has been cooling. Total value locked was recently cited around $94.49 billion, down from a local peak near $137 billion reached in mid-December of the prior cycle window. The point is not that TVL is destiny. It’s that the market keeps oscillating between experimentation and retreat, and every retreat punishes complexity. Anything that requires five dashboards and perfect timing gets abandoned first.

That’s the backdrop where an on-chain fund wrapper becomes more than marketing. In traditional finance, the hedge fund pitch is not “we have a trade.” It’s “we have a repeatable process, risk limits, execution plumbing, and reporting.” Most people never touch that world because the doors are heavy. Minimums commonly start at $100,000 and can run into the millions, and the comparison point is brutal: a typical mutual fund minimum is more like $1,000 to $2,500. Even if you can get in, the fee foundation is often “2 and 20,” meaning roughly 2% of assets every year plus 20% of profits, which is a structure designed for scarce access.

Crypto has tried to “democratize hedge funds” before, usually by turning a strategy into a token and calling it a day. The problem is that most of those tokens are either leverage in disguise or incentives in costume. Lorenzo’s framing is more disciplined: an OTF is meant to behave like a fund share, except the share lives on-chain, is non-custodial, and can be inspected in real time. That’s the surface level. Underneath, Lorenzo describes a Financial Abstraction Layer that routes deposits into defined strategies and issues tokenized units to represent a claim on that strategy. If you translate that into human language, it is trying to do what fund admin and prime brokerage do in TradFi, but with smart contracts replacing the back office.

The most interesting part is what this enables once the wrapper is credible. A fund share in the old world is trapped inside paperwork. A fund share on-chain is a building block. You can hold it, lend against it, use it as collateral, or combine it with other positions, all without asking permission from an administrator. That composability is the part people mention, but the deeper effect is standardization. If strategies can be expressed as consistent, inspectable “fund tokens,” then risk can be compared, priced, and moved around with less ceremony. The market stops being a pile of bespoke vaults and starts looking like a shelf of products.

A concrete example Lorenzo has pushed is its USD1+ OTF, tied to USD1 settlement and a receipt token often described as sUSD1+. Reports around the launch describe it as blending multiple yield sources such as tokenized U.S. Treasury collateral, delta-neutral trading, and on-chain lending into a single vehicle, with the user holding a token whose value reflects performance rather than relying on noisy rebases or emissions. The translation here matters. On the surface, it looks like “deposit stablecoins, receive a yield-bearing token.” Underneath, it is an allocation engine that is deciding how to turn your dollars into a stack of exposures you did not have to assemble yourself.

And then there’s the choice of what “dollars” means. USD1 is positioned as a fiat-backed stablecoin, and its issuer frames the backing as dollars and U.S. government money market funds, with 1:1 redeemability. Reuters has also described USD1 as backed by U.S. Treasuries, dollars, and cash equivalents, with third-party auditing mentioned in earlier coverage. Stablecoin plumbing can feel boring, but boring is a feature if you’re trying to build fund-like products. The moment the settlement asset is fragile, the “fund” is just another leveraged expression of trust.

Still, the risks are not subtle, and pretending otherwise would miss what’s really being built. If you take hedge-fund-like strategies and put them into a token, you don’t delete the underlying complexity. You concentrate it. Delta-neutral trading can blow up if hedges slip, counterparties fail, or funding rates flip faster than models expect. On-chain lending can be safe until it isn’t, because correlations in crypto love to converge during stress. We just watched how quickly forced unwinds can cascade, with multi-billion dollar liquidation bursts that rewrite price levels in hours. If an OTF holds components that depend on liquid derivatives markets, then in a real drawdown the token’s promise of “simple exposure” can turn into a simple way to discover you owned tail risk.

There’s also governance and disclosure risk. TradFi funds live under constraints that are annoying but clarifying: who can invest, what can be marketed, how valuations are struck, how conflicts are handled. On-chain funds inherit new transparency, but they also invite a new kind of opacity: the code is visible, yet the economic assumptions may be hidden in off-chain execution, oracle dependencies, or discretionary parameters. Even if everything is honest, the average holder may not understand what they are holding, which is the same old problem wearing a new interface.

The counterargument is that this is still better than the alternative. In DeFi today, most people either chase simple staking yields that can vanish, or they manually stack protocols and hope nothing breaks. At least an OTF forces strategies to be named, bounded, and monitored. At least it gives the market a chance to price a strategy token the way it prices risk everywhere else, with spreads, collateral haircuts, and real-time flows. If this holds, it could reduce the cultural addiction to improvisation that makes crypto feel thrilling and exhausting at the same time.

Zooming out, what Lorenzo is really pointing at is a broader pattern: finance keeps moving from relationships to instruments. Hedge funds were once access to a person and their network. Then they became access to a strategy and its infrastructure. Now, early signs suggest they might become access to a token that represents a strategy, with the infrastructure embedded underneath. That doesn’t mean everyone suddenly gets hedge fund returns. It means the shape of access changes, and the competition shifts from who can open doors to who can earn trust through transparent, repeatable behavior across market regimes.

The line I keep coming back to is simple: when strategies become tokens, distribution gets easier, but accountability gets harder to avoid.