After 2025, all designs related to BTC will revolve around one name — SEC.

It's not just targeting 'air coins', but everything that **'looks like a yield certificate'**: LST, LRT, RWA yield notes, and even some Wrapped BTC.

The problem is stuck here:

Is it a commodity?

Or is it a security?

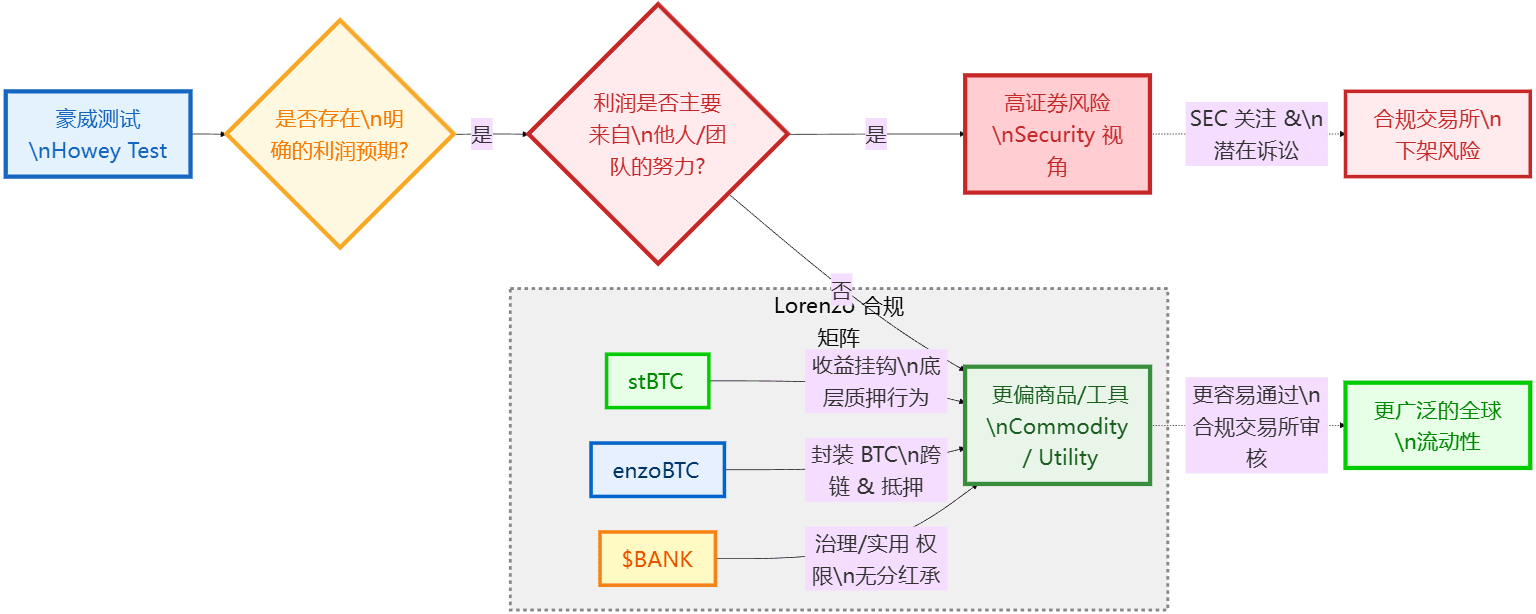

Under the microscope of the Howe test, many Wrapped assets are in a kind of 'Schrodinger's state' — before being sued, no one can clearly say whether they are securities or not. The result is: some Yield Tokens were delisted by compliant exchanges in one fell swoop, and liquidity evaporated instantly.

Lorenzo Protocol chose to be open-ended. Instead of cramming all rights, benefits, and governance into a single token, it used a three-part structure of "stBTC + enzoBTC + BANK" to carve out a safe corridor between regulation and innovation.

Wrapped BTC Dilemma under Howey Test

The Howey Test essentially asks three questions:

Are you investing money?

Did this money go into a common enterprise?

Do you expect to profit from the efforts of others?

If the answer to all of them is "Yes", then in the context of US regulation, you are not far from being classified as a "securities" entity.

This logic is extremely fatal when applied to a large number of yield-bearing assets:

You deposit BTC/ETH into a certain protocol;

The protocol team helps you run various strategies;

The white paper explicitly states "high returns" and "passive income";

→ It's hard not to see it as "profits expected from the efforts of others".

In Q3 of 2025, at least a dozen BTC yield notes and Ethereum LRT/yield certificates were delisted by several compliant exchanges because their yield attributes were described too explicitly, resulting in zero liquidity.

The conclusion is harsh:

If you're unsure which side your token is on in the Howe test,

Sooner or later, regulators will make the choice for you.

Lorenzo's dual-asset solution: stBTC and enzoBTC each fulfill their respective roles.

Lorenzo's approach is simple, yet extremely "lawyer-friendly":

Different financial attributes are broken down into different asset roles.

stBTC: Keep the "profits" properly locked in one room.

stBTC corresponds to the underlying BTC staking/re-staking behavior.

It is essentially closer to fixed-income notes/interest certificates:

You lend BTC to protocols to run strategies (such as Babylon staking, BTCFi arbitrage);

The agreement stipulates that the profits will be credited to stBTC.

You can understand stBTC as:

"I am the lender and have a receipt for that pledged BTC."

It inherently carries the expectation of returns, and will be treated more seriously in compliance and risk control.

It is also more suitable as:

Profit-generating instruments for activist firms/crypto-native funds;

Holders willing to accept more complex compliance disclosures.

enzoBTC: We only provide "packaging" and "passports," we don't sell stories.

Unlike stBTC, enzoBTC strives to be "de-financialized":

It primarily functions as a Wrapped BTC/Multi-Chain Circulation Certificate:

It is responsible for enabling BTC to "instantly move" between chains such as Bitlayer, BNB, and Arbitrum;

Used as collateral, transaction margin, or loan collateral;

No promises are made regarding specific returns.

It does not bind the agreement to the distribution of cash flow.

In short:

stBTC is based on "profit expectations".

enzoBTC combines "practicality + liquidity".

Add another layer, which is BANK:

Location-based governance + practicality (fee discounts, vault access, etc.)

The official statement avoids any "profit sharing promises".

This separation of roles allows Lorenzo to clarify its compliance issues:

Which part is "like debt": stBTC;

Which part is merely a "shell/tool" for BTC: enzoBTC;

Which part is the "operating system of the protocol": BANK.

From Howe Testing to Smart Contracts: How Compliance Is Written into Code

Lorenzo doesn't just write a few "non-securities statement" lines in the Pitch Deck and call it a day.

What they did was to dissect this compliance narrative and incorporate it into legal texts and contractual logic.

Core logic:

In the real world, this matrix roughly corresponds to three actions:

Legal level

Multichain Event Protocol Limited has established entities in jurisdictions such as the British Virgin Islands (BVI).

The white paper and legal statement repeatedly emphasize:

BANK / enzoBTC does not represent equity;

The team does not guarantee any price floor or fixed returns;

Secondary market prices are entirely determined by the market.

Contract layer

The profit distribution logic should be written between stBTC and the underlying position;

BANK's use cases focus on governance, fee discounts, and vault access, rather than "automatic dividends";

enzoBTC's role is primarily encapsulation and cross-chain bridging; it does not handle revenue recording.

Exchange communication layer

For compliant exchanges, this can be clearly explained:

If you want to profit → look at the stBTC side;

Want a BTC liquidity tool? → Listing on enzoBTC is easier to get approved.

To discuss governance tokens, we need to focus on the BANK's utility, not the equity tokens.

For institutional compliance departments, the biggest fear is being unable to "explain things clearly."

Lorenzo's advantages are:

The role of each token can be explained in one sentence.

How should the funds be allocated? Who will hold stBTC, and who will receive enzoBTC and the bank?

For funds, a clear definition = hedging and configurability.

Aggressive funds: Holding stBTC, facing both potential gains and risks.

Objective: To overlay an additional yield curve on top of the BTC position;

Preferences:

Accept more "benefit disclosures" in the product brochure;

Accept volatility and regulatory disclosure requirements that are highly correlated with pledged returns.

Typical player:

Crypto native hedge funds;

A family office capable of making compliant filings;

An active manager who is very familiar with BTCFi and restaking strategies.

For conservative investors: Use enzoBTC as a "BTC pass".

Objective: To participate in BTCFi, cross-chain liquidity, and lending.

But I don't want to raise the compliance threshold to the "revenue notes" category;Preferences:

I prefer to view enzoBTC as a "multi-chain Wrapped BTC";

On the balance sheet, it is classified as "Digital Goods / Commodity Holdings".

Protocols and DeFi native players: simultaneously holding BANK

For this group of people, BANK is more about:

A combination of governance rights, fee rate rights, and priority access rights;

Enhance the efficiency of funds and influence within the Lorenzo ecosystem.

These three types of roles overlap, creating an interesting situation:

stBTC attracts smart money that is "willing to face regulatory oversight of returns";

enzoBTC targets long-term funds that "want BTC liquidity but don't want to get involved in yield disputes."

BANK is the "operating system token" that binds the long-term growth of the protocol.

While many BTC wrappers are still debating "what exactly is it?",

Lorenzo, at least in terms of narrative, provides a clear triangular coordinate system.

Comparing with competitors: It's not about evading regulation, but about learning to dance with it.

The instinctive reaction of many projects is:

"We are a DAO, without a subject";

"This coin was issued by the community; it has nothing to do with us."

"The contract has been decentralized, and the responsible party cannot be found."

In the short term, these words may buy some time during the bear market.

However, recent cases show that:

Regulators are increasingly turning their backs on the "DAO illusion";

The listing committee of the exchange is more concerned with:

Can you explain the legal attributes of a token?

Are there clear boundaries of responsibility and compliance pathways?

Lorenzo took a different path:

Do not pretend to be "ownerless";

It acknowledges that there is a real team and legal entity behind the agreement;

use "stBTC / enzoBTC / BANK three-tier structure + legal disclaimer"

In exchange for a sustainable, credible growth trajectory.

For players like you who follow BTCFi, this design has two direct implications:

What should be considered when determining a valuation?

It's not just about looking at whether APY is high or low, but about:

Whose name is on the title of "right to the proceeds"?

Does the profit logic correspond one-to-one with the legal text?

Who should be prioritized for removal from shelves?

When regulators began to close in...

Those tokens with ambiguous roles and unclear benefits,

They are usually among the first to be "risk isolated".

Web3 has evolved beyond a simple opposition of "regulation vs. decentralization."

Rather, it's about who can design a structure that can both grow and survive long within the gaps of the rules.

Lorenzo used stBTC and enzoBTC to demonstrate the Schrödinger's moment for Wrapped BTC.

I wrote down a relatively clear answer:

As for the profits, just keep them locked away in the stBTC room.

Liquidity and utility will be handled by enzoBTC;

The long-term value and governance of the agreement are concentrated in BANK.

When the regulatory sieve is shaken again in 2026,

Which BTCFi products will remain on the shelves of compliant exchanges?

It may not depend on APY, but rather on whether you have clearly defined "who I am" today.

I'm like someone who's determined to succeed by following a set pattern, constantly monitoring the BTCFi and Lorenzo lines.

Before the next shift in the BTC narrative,

Those who understand the structure are often better able to grasp the cycle.@Lorenzo Protocol #LorenzoProtocol $BANK