Every cycle has a moment where traders stop hunting the next 2x and start asking a boring question: where can I park size without getting wrecked? That’s why yield-bearing dollars keep pulling attention whenever volatility spikes, especially in a market tape. Falcon Finance just gave that narrative a jolt by showing a dedicated $10 million insurance fund on its transparency dashboard, with the page timestamped 05 Dec 2025.

Here’s the tape. FF is around $0.1167 with a $273.06M market cap and roughly $27.65M in 24h volume on Binance’s price page. Binance also shows FF up 8.83% over the last 24 hours, which tells you sentiment is still twitchy. CoinGecko shows a -9.23% move over 7 days.

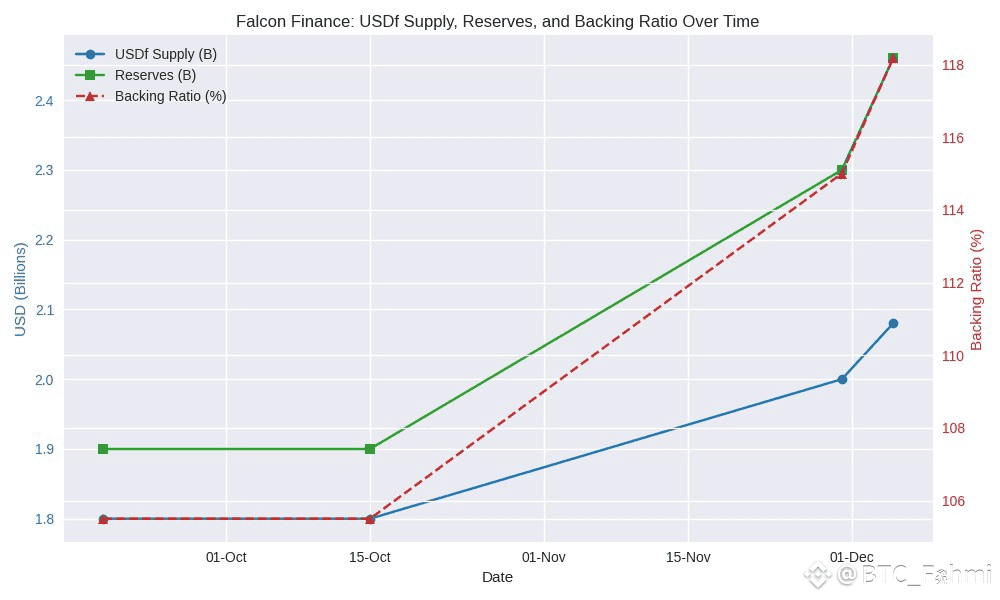

What’s actually happening? USDf is an overcollateralized synthetic dollar, meaning you lock up more than $1 of assets to mint about $1 of USDf. Think of it like taking a loan where the shopkeeper insists you leave two guitars behind to borrow the value of one. Falcon’s dashboard shows $2.46B in total reserves backing $2.08B USDf supply, a protocol backing ratio of 118.17%, and an sUSDf-to-USDf value around $1.0859. The insurance fund is there for tail events, the stuff models miss.

The other reason this matters is receipts. On the same dashboard, Falcon lists weekly reserve reports dated 02 Nov 2025, 09 Nov 2025, 16 Nov 2025, 23 Nov 2025, and 30 Nov 2025, plus a quarterly audit report dated 28 Jul 2025. Then on 04 Dec 2025, Falcon published an interview spelling out how it thinks about scaling, risk, and what “success” looks like in Q1 2026.

Adoption is showing up in chunky numbers, not just tweets. Falcon’s tokenomics post, published 19 Sept 2025 and updated 15 Oct 2025, said USDf had reached $1.8B circulating with $1.9B in TVL. The 05 Dec 2025 dashboard snapshot shows USDf supply at 2.08B with $2.46B reserves. Binance Research notes more than $50M liquidity on Curve and more than $35M on Uniswap for USDf swaps.

Here’s the technical bit, in trader English. Falcon says it generates yield with a market-neutral strategy stack, basically trying to earn without taking a big directional bet. On the dashboard, the strategy allocation is 61% options-based strategies, 21% positive funding farming plus staking, 5% statistical arbitrage, 3% spot/perps arbitrage, 2% cross-exchange arbitrage, 5% negative funding farming, and 3% extreme movements trading. Basis traders know the promise and the blowups.

Tokenomics are unusually readable. The official post puts total supply at 10B FF, allocated 35% to ecosystem, 24% to foundation, 20% to core team and early contributors with a 1 year cliff and 3 year vesting, 8.3% to community airdrops and launchpad sale, 8.2% to marketing, and 4.5% to investors with the same vesting. Binance Research adds that reported day 1 circulating is 23.40% and day 1 real float is 18.00%.

So what’s ahead in Q1 2026? Falcon’s 04 Dec 2025 interview gives three priorities: expand real-world assets as collateral, push staking vaults that pay USDf yield without new token emissions, and grow crypto collateral. It also sets targets: reach $5B total TVL, launch a fully compliant RWA line, secure two sovereign bond tokenization pilots, and become the exclusive yield provider for at least three retail platforms.

Competitors set the benchmark. Ethena sits around $6.9B TVL on DefiLlama, and USDe’s market cap is about $6.702B. Sky shows $7.043B TVL, and Frax Finance is closer to $541.98M.

My bull case has three legs. First, the balance sheet is transparent today: $2.46B reserves, 118.17% backing, and a visible $10M insurance fund. Second, if they execute even part of the Q1 plan and push TVL toward $3B, integrations get easier and liquidity tends to stick. Third, Falcon talks about routing a portion of protocol revenue to FF stakers in stable assets rather than relying on inflationary emissions.

The bear case deserves respect too. One, 61% options-based strategies means model and execution risk, and those only show up when markets gap. Two, synthetic dollars live and die by confidence, a single scare can trigger redemptions and liquidity stress. Three, regulation is a wild card, and “fully compliant” RWAs implies legal and operational complexity that can slow timelines.

Zooming out, Falcon is betting that the next wave of onchain dollars looks more like audited custody plus hedged carry than a yield farm. If you’re tracking it, the scoreboard is simple: USDf supply, backing ratio staying north of 110%, the cadence of weekly attestations, and progress toward $5B TVL.

So let me ask you: what would convince you the $10M insurance fund is more than a headline, a public stress test, three straight months of clean attestations, or USDf pushing past 3.0B supply while holding the peg?

@Falcon Finance #FalconFinance $FF