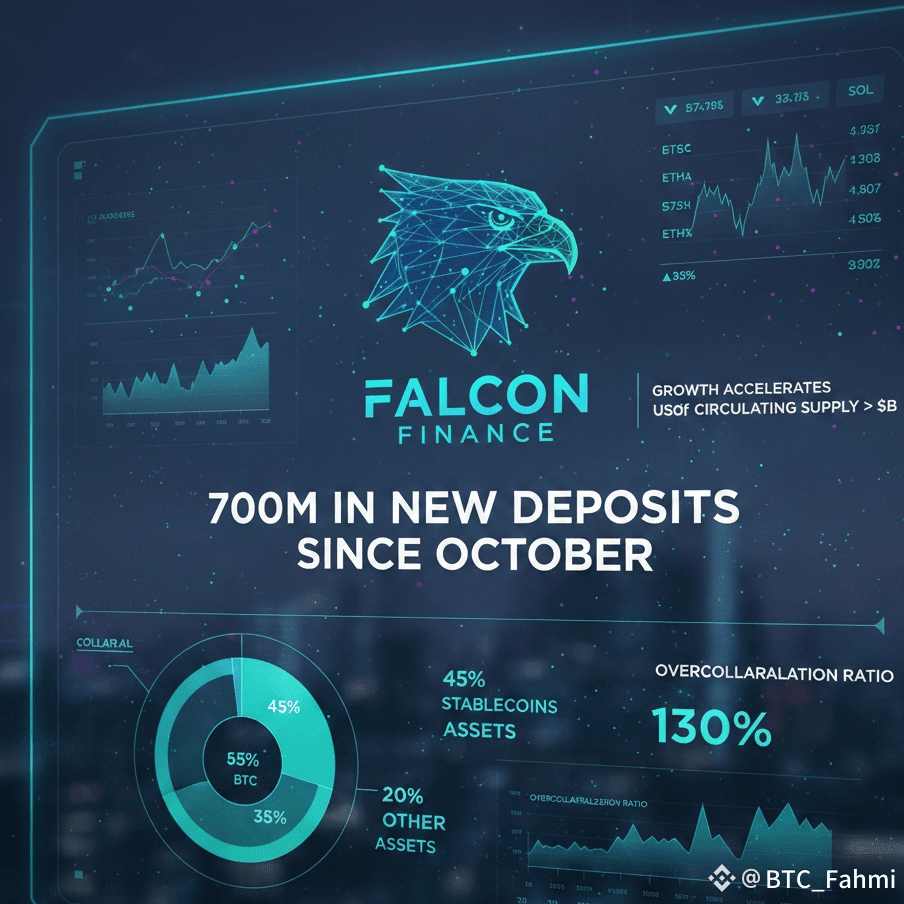

If you’ve been watching stablecoin and DeFi flows since Q4 kicked off, you’ve probably seen Falcon Finance and its synthetic dollar USDf creeping into your feed more and more. The big inflection point came on October 10, 2025. During a sharp market drawdown that flushed a lot of leverage out of majors, Falcon reported more than $700 million in new deposits and fresh USDf minting in a very short window. Shortly afterward, USDf’s circulating supply pushed past $2 billion.

For a stablecoin-style product, that’s not just “number go up.” USDf is an overcollateralized synthetic dollar, which is a fancy way of saying users lock up other assets BTC, ETH, SOL, stablecoins, even some real-world-asset tokens and mint a dollar-pegged token against them. “Overcollateralized” means you post more value than you borrow, so if you mint $1,000 of USDf you might be locking $1,300 or more in collateral. That design is meant to create a buffer against price moves in the underlying assets.

The October spike in deposits didn’t happen in a vacuum. By mid-November, Falcon rolled out a full transparency and risk-management framework around USDf. There’s now a public Transparency Dashboard that shows, in near real time, how much collateral sits behind the system, how overcollateralized USDf is, and what the reserves are made of Bitcoin, Ethereum, Solana, various stablecoins, and tokenized US Treasury bills, among others. The dashboard also breaks down how much sits with regulated custodians versus on-chain multisig wallets.

On top of the live data, Falcon added weekly proof-of-reserves attestations by HT.Digital and quarterly assurance reports, plus smart-contract audits from firms like Zellic and Pashov. The idea is pretty straightforward: users shouldn’t have to guess what backs their “dollar,” or whether the contracts were only checked once before launch. In a sector still dealing with the hangover of opaque reserves and under-collateralized experiments, this “default-on transparency” angle is part of why traders and institutions are paying attention.

Under the hood, Falcon is positioning itself as “universal collateral infrastructure.” In plain English, they want any reasonably liquid asset to be usable as collateral to mint on-chain dollars that can then chase yield, provide liquidity, or plug into derivatives and RWA rails. As of early October, analyses from DWF Labs pointed to reserves peaking around $2 billion in total value locked (TVL), with roughly 45% in BTC and 35% in stablecoins, and the rest spread across DOGE, mBTC and a basket of smaller assets.

Those reserves are deployed into what most pro traders would recognize as delta-neutral or market-making style strategies: native staking on PoS chains, funding-rate arbitrage on perpetuals, basis trades between spot and futures, and cross-exchange arbitrage. The goal is to earn yield from spreads and fees rather than betting on direction. A recent performance snapshot put sUSDf, the yield-bearing version of USDf, at leading 7- and 30-day APYs around the high-single-digit range earlier in the year, and even higher on some regional listings later on well above typical DeFi stable yields.

Fundraising and listings have reinforced that growth story. By late September 2025, Falcon’s community sale had pulled in about $112.8 million in commitments, 28x oversubscribed versus a $4 million target, with over 190,000 participants. In October, Bitkub Thailand’s dominant regulated exchange listed the FF token with an FF/THB pair on October 29, giving Falcon direct access to Southeast Asia’s retail flow and highlighting USDf’s roughly $2B+ circulation and near-$2B TVL at that time. On top of that, multiple strategic investments in August and October pushed Falcon’s implied valuation into the $400M+ range.

Why is this trending now, when most traders are already spoiled for choice with stablecoins and yield wrappers? Partly, it’s timing. After several years of “trust us” stablecoins and yield schemes that blew up under stress, the market is rewarding projects that over-communicate their risk. Falcon’s playbook dashboards, weekly attestations, diversified collateral, strict admission rules for new assets leans directly into the post-2022 risk-off mindset, especially on the institutional side. If you’re a desk that has to explain its stablecoin exposure to a risk committee, being able to show third-party attestations and granular reserve data is a big deal.

From a trader’s perspective, the October “$700M in” moment is interesting because it happened during stress, not euphoria. Flows gravitated toward a product that promises conservative, mostly hedged yield rather than leveraged punts. That can be read as a vote of confidence or as crowded risk if everyone piles into the same trade. The collateral set still includes long-tail assets, even if capped, and the strategy stack is complex. You’re ultimately trusting that their risk systems, liquid staking choices, and exchange counterparties all behave when the next true black-swan hits.

If you’re trading or building around Falcon, the things worth watching aren’t just TVL or APY screenshots. Track the overcollateralization ratio on the dashboard during sharp drawdowns. Watch how fast positions get de-risked when volatility spikes. Pay attention to changes in collateral composition if BTC and stables start giving way to thinner names, that changes the risk profile. And, as always, keep an eye on where USDf is being integrated: money markets, perp venues, RWA platforms, and CEX listings all affect liquidity and reflexivity on the way up and the way down. None of this is financial advice, but if you’re going to trade or farm around a protocol that just pulled in $700M of fresh capital since October, it’s worth understanding what’s really driving that growth and what could unwind it just as quickly.

@Falcon Finance #FalconFinance $FF