Azu knows that when everyone sees 'USDf can be used at over 50 million merchants globally through AEON Pay,' the first reaction is often excitement: finally, it's not just moving around on the chain, but being able to swipe for a cup of coffee, buy a plane ticket, or send some living expenses to family. The official announcement details the path specifically—payments through the AEON Pay Telegram App, and it has already integrated with a bunch of mainstream wallets, covering both online and offline scenarios. It also mentions that the service will first land in Southeast Asia and then expand to markets like Nigeria, Mexico, Brazil, and Georgia. It sounds like the ultimate narrative of 'stablecoins entering life,' but I want to remind you: the truly mature usage is not 'I can spend,' but 'I need to do risk control before I spend,' because payment is essentially a pressure test of sending on-chain assets into the real settlement system.

The first thing is regional availability; you have to treat it as a 'variable that changes' rather than something that is permanently available once activated. The official statement is that it covers over 50 million merchants globally, but the rollout is market-specific, and local payment networks, channel compliance, and the onboarding progress of local partners may all affect 'whether you can use it today or still use it tomorrow.' In the same country, there may be situations where it is 'usable but not easy to use' or 'usable but only at specific merchants/specific paths' due to regulatory guidelines, channel maintenance, or even restrictions in certain high-risk industries. You need to clearly distinguish: being able to make a transaction and being suitable for long-term use as a daily payment tool are two completely different matters.

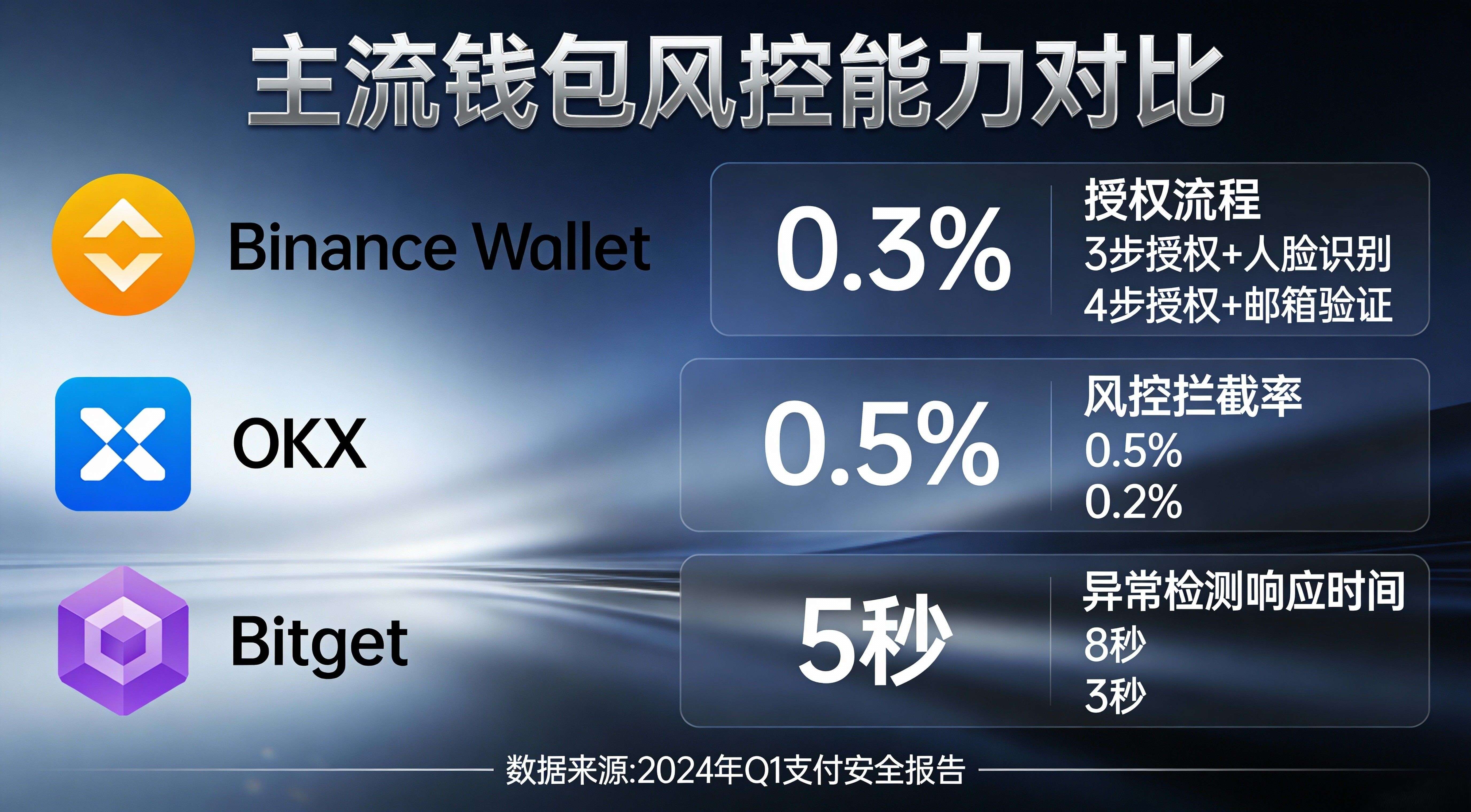

The second thing is the differences between wallets and channels; don’t misunderstand 'integrated many wallets' as 'the experience is the same.' The announcement mentions that the AEON Pay Telegram App will integrate wallets like Binance Wallet, OKX, Bitget, KuCoin, Solana Pay, TokenPocket, Bybit, etc., but different wallets may have completely different worlds in terms of authorization processes, risk control interceptions, fee displays, and failure rollback experiences. More realistically, although it's all called 'payment,' the underlying processes could involve QR code payments or bank transfer type channels, leading to differences in transaction speeds, failure probabilities, and the vouchers you need to retain. If you don’t first clarify 'which wallet I use, which channel I go through, and how to roll back when it fails,' when you really need to use money, you will find that the most painful part is not the extra 1% transaction fee, but that you have no idea where the problem lies.

The third thing is the boundaries of time and compliance: from on-chain assets to real-world settlement, there is a gray area in between that you think is smooth but actually has friction. Holding USDf on-chain does not mean that the real world will immediately recognize it; this involves exchange/settlement paths, processing times of channels, and the requirements of your jurisdiction for stablecoin payments, foreign exchange, and tax reporting. Many people only focus on 'Did I pay it out?' and do not pay attention to 'Do I need to record this stablecoin consumption? Does it involve cross-border payments? Does it trigger local reporting obligations?' When you use it as a long-term tool, compliance costs are not optional; they are the 'implicit fees' you must factor in in advance.

So the change in rules that this article wants to promote is very simple: upgrade from 'I can spend' to 'I do risk control before I spend.' Azhu's action advice for you is also very hardcore — for your first payment, don’t chase excitement; specifically use a small amount to do a test, treating it as a drill rather than consumption. You need to deliberately test three things: first, how high the success rate is, whether the money will be stuck if it fails, and how long it will take to get it back; second, how is the experience of receiving and confirming the payment, whether there is a noticeable delay from the time you initiate the payment until the merchant confirms it; third, from the perspective of your own jurisdiction, what reporting/compliance points this payment may involve, and whether you can retain clear evidence (screenshots, order numbers, on-chain records) for future reconciliation. As long as you successfully run these three things with a small amount, you will be closer to being a long-term player than 90% of those who 'see it and rush in.'