Recently, the hot topic of stablecoins is increasingly resembling traditional finance: OCC has been reported to be granting (or advancing) national trust bank license approvals to multiple crypto companies, pushing issuers into the 'quasi-financial institution' framework; senior officials of the Reserve Bank of India have publicly warned about the macro risks of stablecoins; the Bank of England is also adjusting its regulatory proposals for stablecoin reserve investments—it's evident that stablecoins are being treated as part of the currency system. (Axios)

The problem is that most people focus on 'audit/reserve/compliance', but overlook the real switch for stablecoins: the monetary policy button. In centralized stablecoins, this button is held by the board, regulatory interface, and banking system; but in decentralized stablecoins, this button is often held by the 'governance layer'. You think you are holding a 1:1 US dollar, but in reality, you are also betting: who can change its parameters, when to change them, and to what extent.

And this is precisely where USDD (Decentralized USD) deserves a re-examination. USDD 2.0 has already shifted from traditional algorithmic stablecoins to a structured path of CDP + over-collateralization, relying on collateral and mechanisms rather than faith for its anchor; but its long-term stability depends not only on collateral and the PSM (Peg Stability Module) but also on 'who is defining the risk boundaries'.

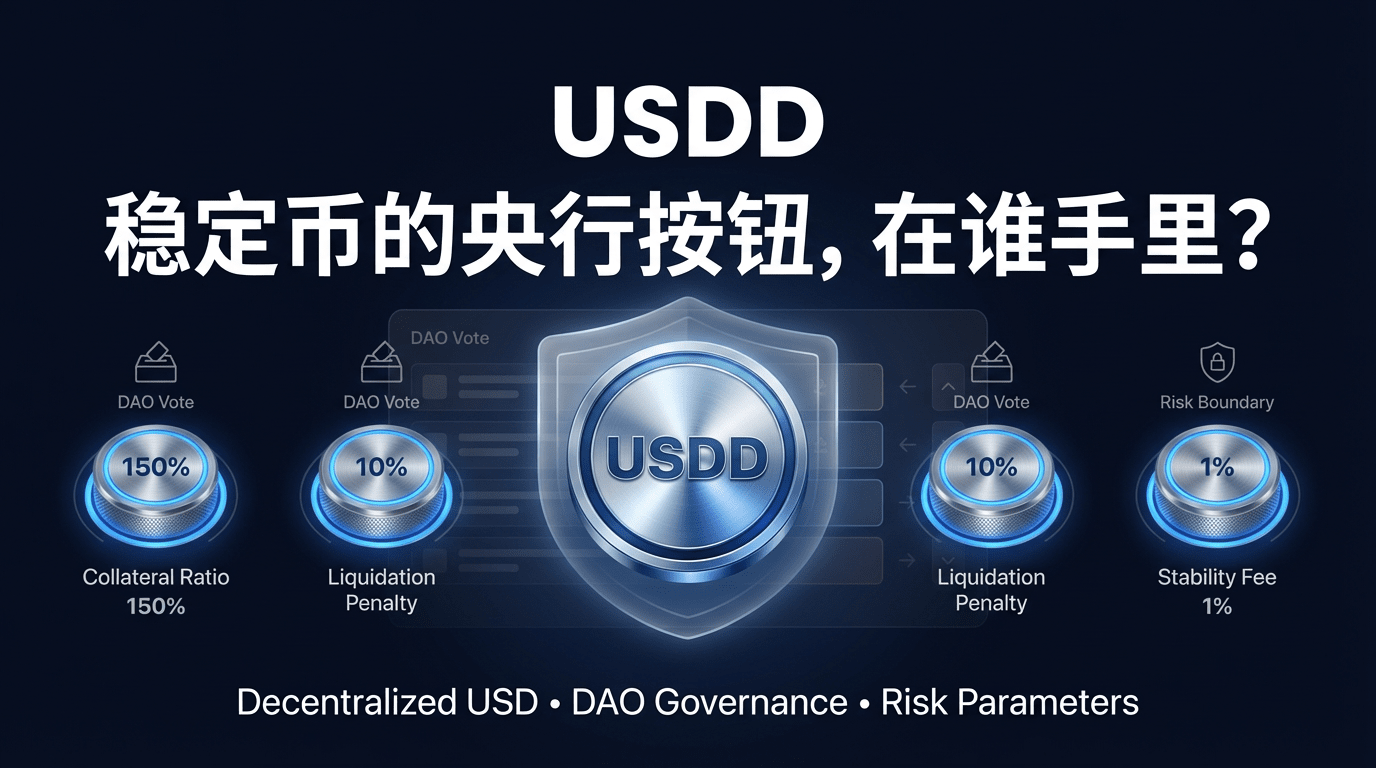

The real watershed is here: **USDD's monetary policy is not in some office, but in governance votes.** The knowledge base is written plainly—JST holders constitute the core governance layer of JustLend DAO, holding voting rights over key parameters of the USDD protocol. This means that USDD's 'central bank button' consists of at least three types of hard switches, each capable of directly altering the nature of the stablecoin as you understand it:

The first type of switch determines 'whether the system will collapse under pressure': the minimum collateral ratio threshold, liquidation penalty ratio, and stability fee rate. Once the collateral ratio threshold is lowered, it will be easier to expand supply in the short term, but the system's resistance to volatility will be weakened; raising the liquidation penalty can suppress high leverage behavior but may also amplify user losses in extreme market conditions; increasing the stability fee rate (which you can understand as the cost of borrowing USDD) will suppress minting expansion but may also raise the 'implicit threshold for holding USDD'. This is the typical trade-off in monetary policy: stabilizing risk boundaries vs expanding usage scale.

The second type of switch determines 'where the yield comes from and where the risk exposure is': the investment direction of the Smart Allocator. Governance can vote to decide whether to add a certain DeFi target to the protocol's reserve funds. This matter seems to be a yield issue, but at its core, it is a risk landscape issue: deploying idle reserves into a more blue-chip lending protocol may yield more moderate returns but with more controllable risks; if you push funds towards tail yields, the short-term APY may look better, but once protocol risks/liquidity exhaustion occurs, the entire trust foundation of the stablecoin is hurt. For a system like USDD that emphasizes 'over-collateralization + on-chain transparency', the Allocator's asset allocation is almost equivalent to the 'risk preference of the on-chain Treasury.'

The third type of switch determines 'who the value flows back to': the profit distribution ratio. The DAO decides how much of the protocol's profits are used to buy back and destroy JST and how much is distributed to sUSDD holders. This is not a minor adjustment, but rather the steering wheel of value capture: leaning towards JST means a stronger value anchor for the governance token; leaning towards sUSDD means that the 'yield stablecoin' attributes are more pronounced and better at attracting TVL. You will find that many people discussing stablecoins only focus on whether it can maintain a 1:1 peg, but for the DeFi ecosystem, 'who gets the yield' will also determine whether the funds will stay.

Widening the perspective—this is the subtle position of USDD 2.0 in the regulatory era: the narrative of the US GENIUS Act is pushing centralized stablecoins towards a path of '100% reserves + strict audits + regulatory interfaces', while USDD chooses to position itself in the differentiated space of 'decentralized commodities', responding to trust issues with on-chain transparency and emphasizing properties like non-freezable contracts. But the cost of this route is: you cannot outsource trust to regulation; you can only build trust on mechanisms and governance.

So when looking at USDD (Decentralized USD), I suggest you ask yourself a different question:

It's not 'Will USDD de-peg?', but rather—when the market environment changes, regulatory narratives shift, and on-chain interest rates fluctuate, which buttons will the governance layer of USDD twist in which direction?

Will they lean more towards 'conservative': raising collateral rate thresholds, tightening risk exposures, reducing tail yields?

Or will they lean more towards 'expansion': lowering thresholds, amplifying supply, attracting minting with stronger yields?

Both paths can tell a story, but they lead to completely different risk curves.

To summarize: the world of stablecoins is being forced to 'financialize', and the competitiveness of decentralized stablecoins increasingly resembles a governance capability competition. **USDD (Decentralized USD)**'s underlying structure (CDP over-collateralization, PSM mechanism, on-chain transparency) allows it to come closer to 'verifiable credit', but what truly determines how far it can go is how the governance layer continues to define risk boundaries, yield boundaries, and user boundaries. Understanding USDD is not just about how stable it is now, but whether its 'central bank button' will be turned in a direction you cannot bear.

Disclaimer: The above content is personal research and views of 'seeking a sword in a boat', intended for information sharing only and does not constitute any investment or trading advice.