The American stock market continues to reach new highs despite weak consumer sentiment and the gap between stock dynamics and the state of the economy. Analysts at Bravos Research note that in the past, such periods of growth have always ended under the same macro conditions.

What is happening in the U.S. stock market?

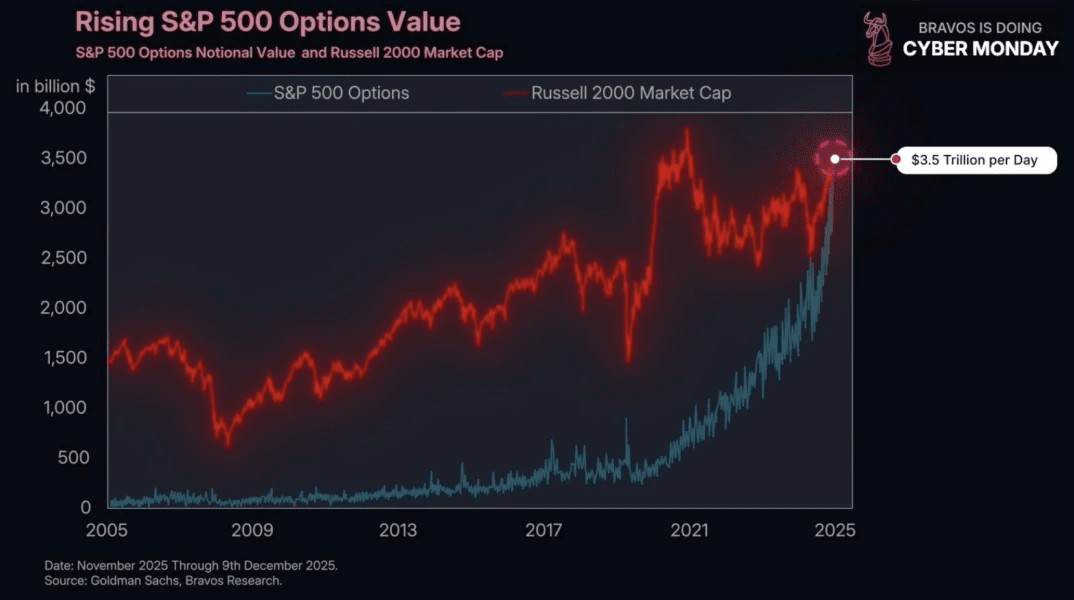

In their analysis, Bravos Research draws attention to the sharp increase in speculative activity. Daily trading volume in options on the American market reached $3.5 trillion. Such a volume is comparable to the total capitalization of all companies in the Russell 2000 index and indicates extensive use of short-term and high-risk strategies.

At the same time, margin debt on the New York Stock Exchange is rising. Its volume reached $1.2 trillion, increasing by approximately 45% over the past year. Similar growth rates were previously recorded only in 2008 and 2021, shortly before periods of serious market turbulence.

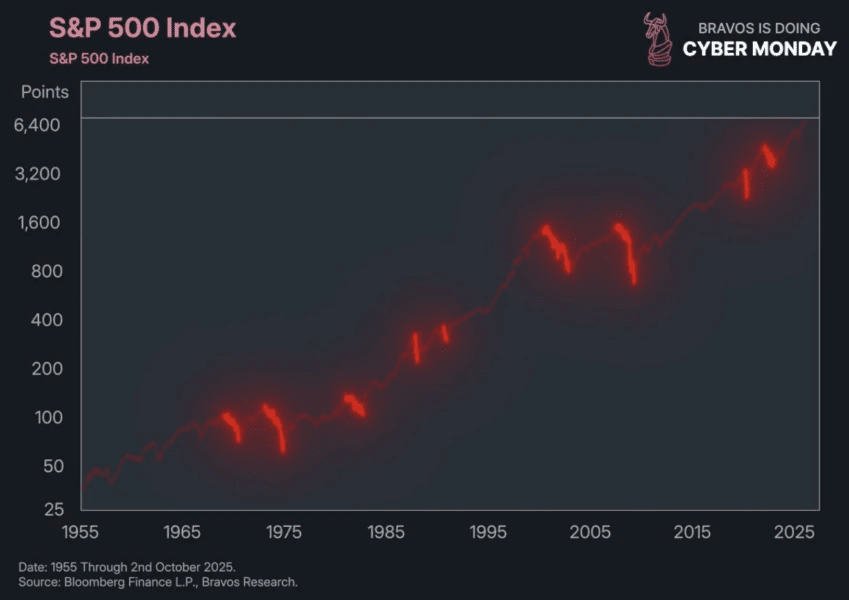

Against this backdrop, the S&P 500 index has increased by 235% over the past ten years. Historically, such returns are extremely rare and were previously observed at the end of the 1920s, early 1960s, and during the dot-com bubble in the late 1990s.

Why is the market growing despite consumer sentiment?

Bravos Research notes a significant divergence between market behavior and the real economy. Data from the University of Michigan shows that consumer sentiment in the U.S. remains one of the weakest in the past 70 years. The rising cost of living continues to put pressure on households, despite the strong dynamics of the stock market.

In previous periods of high ten-year returns, stocks rose amid consumer confidence in the future of the economy. The current situation deviates from this pattern. With weak sentiment, the market continues to move upward, and investors are increasing risk in an attempt to maintain participation in the rally.

The role of expectations.

According to analysts, the market's resilience is largely explained by expectations of corporate profits. Wall Street is pricing in about 18% average annual profit growth for S&P 500 companies over the next five years. This figure is almost double the long-term average.

The main contribution to such forecasts comes from a limited number of the largest tech companies. The revenue growth of Nvidia, Microsoft, Amazon, Google, and Meta is linked to the development of AI, cloud services, semiconductors, and digital advertising. This dynamic poorly reflects the state of consumer demand in the U.S. economy.

Investors take this imbalance into account, which is why the largest tech companies receive the greatest weight in the index and the highest valuations. Bravos Research emphasizes that such a market structure may persist as long as profit expectations are justified.

The market is becoming vulnerable.

High profit growth expectations lead to rising valuations. The forward P/E ratio for S&P 500 approached levels last seen during the dot-com bubble.

Such a situation makes the market sensitive to any changes in forecasts. A decrease in profit expectations can quickly intensify pressure on stocks. Analysts at Bravos Research emphasize that a high valuation by itself is not a trigger for the end of a bull market.

The main macro factor that would end bull markets.

The key conclusion of Bravos Research is that all major bear markets over the past 70 years occurred under inflation conditions above 3.5%. In several cases, including 1987, 1999, and 2022, it was the rise in inflation that became the point of ending years of stock growth.

An exception was the crash of 2020 caused by the pandemic, when inflation remained below this level.

Inflation directly affects interest rates and liquidity. Rising prices force central banks to tighten monetary policy. Financial conditions become stricter, and capital inflow into risk assets decreases.

According to Bravos Research, the current bull market in stocks is unlikely to end until inflation turns upward.

What does crypto have to do with it?

The same logic applies to the crypto market, as it largely mirrors the stock market. Bitcoin and altcoins are sensitive to global liquidity and interest rate expectations. As long as inflation remains under control, the conditions for growth in risk assets, including cryptocurrencies, persist.

Historically, phases of active risk in the stock market were accompanied by capital inflow into crypto. Investors willing to take on increased risk in stocks and derivatives often expand their exposure to digital assets.

The scenario of an inflation reversal carries key risks for the crypto market as well. Rising prices can force regulators to tighten policy again, leading to synchronized pressure on stocks and cryptocurrencies. In this case, Bitcoin is highly likely to continue behaving as a risk asset rather than a safe haven.

The dynamics of inflation remain the main macro indicator for participants in the crypto market. As long as the indicator does not exceed critical levels, the scenario of continued growth described by Bravos Research formally remains.