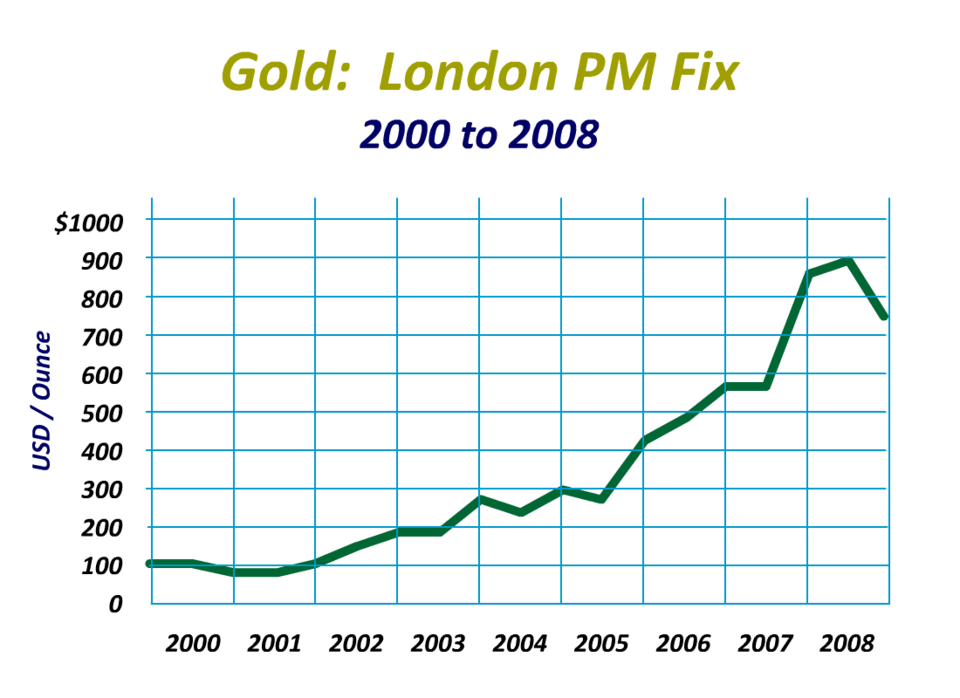

In 2025, the price of gold surged over 60%, breaking the $5000 per ounce mark, becoming one of the most dazzling assets in the global financial market. This rise is not only due to geopolitical uncertainties, inflationary pressures, and central banks' continued accumulation, but also reflects potential changes in the international monetary system. (As of yesterday, it has surpassed $5100 per ounce)

As an ordinary person, why should one hold gold?

First of all, gold is a classic safe-haven asset. In times of economic uncertainty, geopolitical conflicts, or market turmoil, investors often turn to gold to preserve value.

For example, in 2025, global trade tensions and geopolitical events drove gold prices up more than 55%, and central banks also view gold as a tool for reserve diversification, as it has no credit risk, does not rely on any issuer, and has high liquidity.

Secondly, gold is an effective means to combat inflation. Historically, gold prices tend to be positively correlated with inflation rates, as gold can maintain purchasing power when fiat currency depreciates. In the long term, gold's performance as a store of wealth surpasses many assets, especially in high-inflation environments.

Thirdly, gold provides diversification benefits. It has low correlation with stocks and bonds, offering a buffer during market downturns. Moreover, gold's scarcity and historical value make it a long-term investment choice that is not influenced by the policies of a single country.

Finally, from a central bank perspective, gold aids in reserve management. Reuters analysis shows that central banks buy gold to diversify risks and avoid dependence on a single currency.

Who is buying gold?

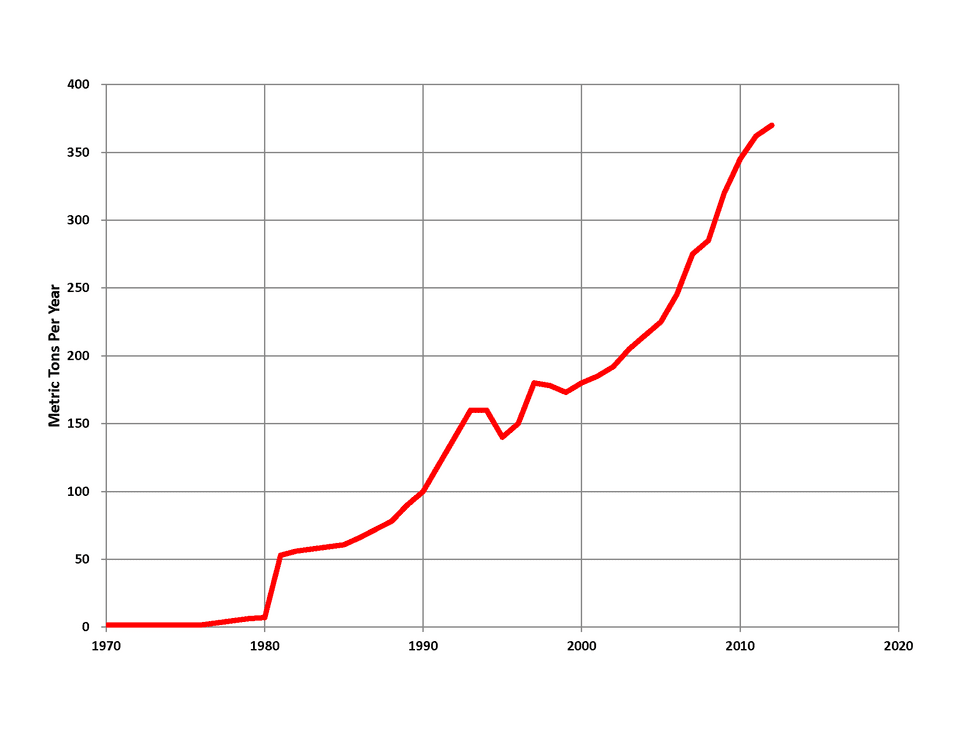

In 2025, the net gold purchases by global central banks are expected to be approximately 772 tons, lower than the thousand-ton levels of previous years, but still strong. Emerging markets dominate purchases, while developed countries remain relatively cautious.

Major buyers include: Poland, Kazakhstan, Brazil, China, Turkey.

Dollar hegemony

Since World War II, the dollar has dominated the global financial system, establishing its 'gold-like' status through the Bretton Woods Agreement. The dollar accounts for about 58% of global reserves, dominating trade settlements and commodity pricing (such as oil and gold). This hegemony grants the U.S. geopolitical influence, but it also faces challenges. The relationship between gold and the dollar is closely intertwined: historically, they have shown a negative correlation, with gold prices often falling when the dollar strengthens.

After Nixon ended the gold standard in 1971, the dollar shifted to a floating currency, but its hegemony did not decline. In recent years, calls for de-dollarization have risen: the dollar's share of reserves fell from 71% in 2000 to 57.8% in the second quarter of 2025. Gold has emerged as an alternative, with central bank gold reserves exceeding 25%, the highest in 25 years. Challenges include sanctions (such as against Russia), inflation, and geopolitical tensions. BRICS countries are promoting a gold standard or new currency to weaken the dollar.

However, the dollar is unlikely to be replaced in the short term: its liquidity, network effects, and the strength of the U.S. economy support its position. The rise of gold does not signify the end of dollar hegemony, but rather serves as a complement, marking a trend towards multipolarity.

The ambitions of East Asia

As the world's second-largest economy, East Asia is driving a strategic transformation through gold reserves. By 2025, East Asia's official gold reserves will reach 2,306 tons, accounting for about 6% of total reserves, doubling from a few years ago.

However, analysts estimate that actual reserves may be as high as 30,000 tons, through mine control and undisclosed accumulation.

The core of this 'ambition' is de-dollarization: reducing holdings of U.S. debt and shifting towards gold and the internationalization of the yuan. East Asia has been downgraded from the largest holder of U.S. debt while accelerating gold imports. Collaborating with Russia, it uses yuan and gold for settlements, reducing reliance on the dollar.

Motivations include financial sovereignty: the risk of sanctions encourages diversification. Within the BRICS framework, China is promoting a gold standard new currency to challenge the dollar. Furthermore, controlling global mines (for gold, copper, etc.) enhances resource influence. This is not only an economic strategy but also involves geopolitical ambitions: elevating the yuan's status and constructing an alternative financial system. China's gold reserve growth marks its transition from dollar dependence to a multipolar world.

How high can gold go?

The gold price forecast for 2026 is optimistic, influenced by central bank demand, geopolitical risks, and Federal Reserve policies.

JPMorgan: Maintains an optimistic outlook, expecting an average price of $5,055 in the fourth quarter of 2026, potentially rising to $5,400 or higher in the long term.

Goldman Sachs: Recently raised its price forecast for the end of 2026 to $5,400 (up $500 from the previous $4,900), driven by demand from private investors and emerging markets.

Bank of America has raised its recent gold price target to $6000 per ounce, the most aggressive forecast among all major institutions.

The future of gold depends on global changes, but its status as a strategic asset has already been established. Investors should allocate based on risk preferences.