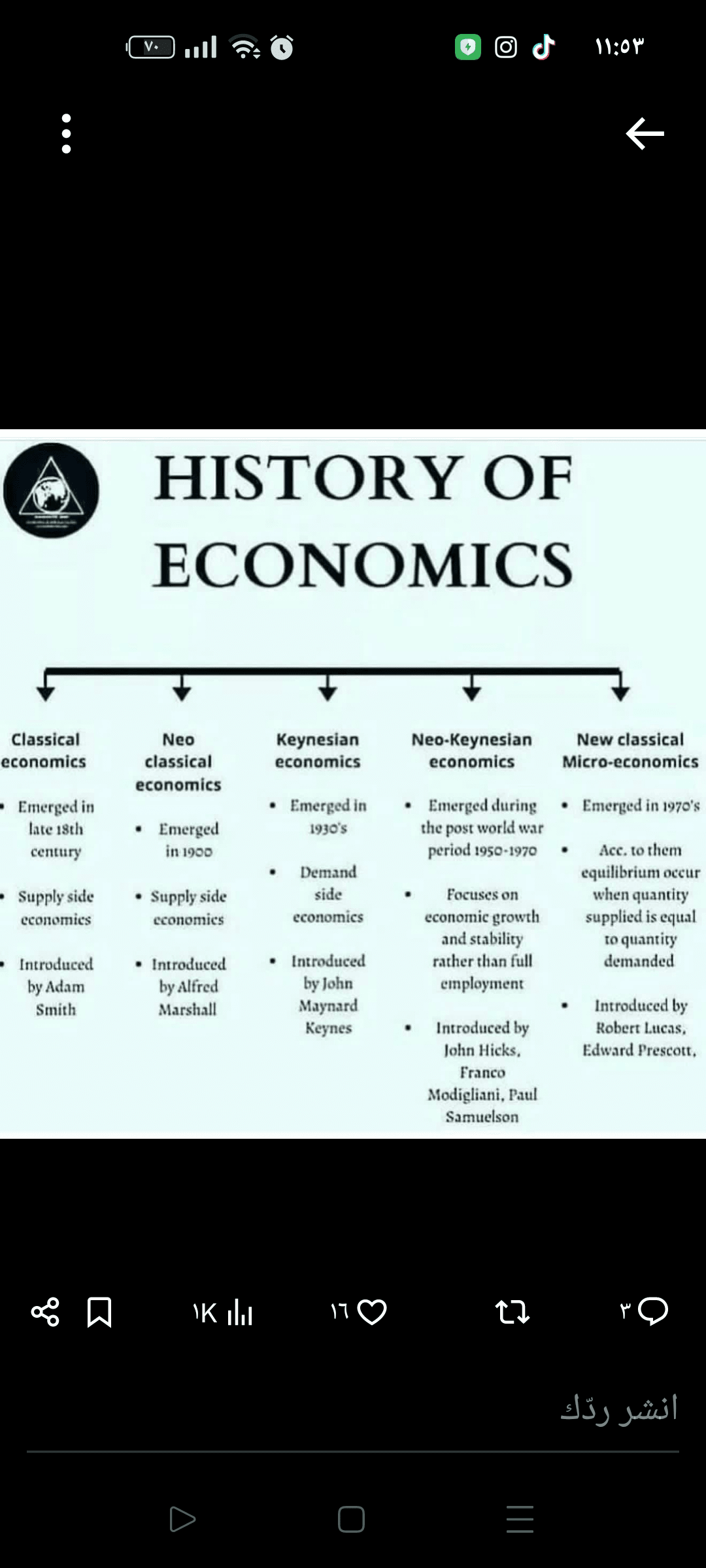

The displayed image summarizes more than two centuries of economic thought development in a trajectory that appears linear, but in reality is a dialectical cumulative path, where no school has abolished its predecessor, but rather reinterpreted or rebelled against it in response to economic reality shifts.

First: Classical Economics – Free Market Economics

It emerged in the late eighteenth century with Adam Smith, in the context of the Industrial Revolution. He assumed that the market is capable of self-correcting through price mechanisms, and that supply creates demand (Say's Law). This thought was suitable for emerging economies with limited government intervention, where the fundamental problem is increasing production rather than managing crises.

Second: Neoclassical economics – market rationalization

With Alfred Marshall at the turn of the twentieth century, analysis shifted from philosophical macro-level to mathematical micro-level analysis. The focus here is on maximizing utility and partial equilibrium, and assuming complete rationality. This school did not change the spirit of the classics, but it provided more precise analytical tools.

Third: Keynesianism – the return of the state to the stage

Keynesianism emerged in the 1930s as a direct reaction to the Great Depression. John Maynard Keynes turned the classical hypothesis upside down: the problem is not in supply but in demand. Unemployment may be equilibrium, and the state is required to intervene through fiscal policy. Here, economics shifted from “the science of markets” to “the science of managing cycles.”

Fourth: New Keynesianism – reconciliation, not rupture

After World War II, economists like John Hicks and Paul Samuelson tried to reconcile Keynesianism and Neoclassical economics. The goal was no longer just full employment, but stability and growth. This school is the theoretical basis for post-war policies, but later struggled against stagflation in the 1970s.

Fifth: New Classical School – the counter-revolution

In the 1970s, with Robert Lucas and Edward Prescott, the focus returned to rational expectations, and the effectiveness of discretionary policies was questioned. Economics here is built on dynamic models, markets are assumed to be efficient, and government intervention is of limited effect.

The important conclusion:

This map is not a “history of corrected mistakes,” but a record of attempts to understand an ever-changing economy. Each school was correct in its context, and wrong if generalized outside its conditions. The common mistake today is to treat one school as an “absolute truth,” while the smart policymaker is one who possesses a diverse toolbox and knows when to use each tool.

Economics is not a doctrine… but a tool