Various Fi types that people often hear about, such as CEFI, DEFI, GameFi, SocialFi, etc., today we will discuss the most useful PayFi for retail investors.

What is PayFi?

PayFi, short for Payment Finance, is an emerging blockchain finance concept officially proposed by Lily Liu, the chair of the Solana Foundation, at the EthCC conference in 2024. It means deeply integrating payment and financial services, utilizing blockchain technology to achieve real-time settlement, programmable money, and maximizing the time value of money (Time Value of Money, TVM). In simple terms:

PayFi is not just simple crypto payments, but a new financial market built around the 'time value of money'.

Core vision: Realizing the original ideal of the Bitcoin white paper for a 'peer-to-peer electronic cash system', allowing money to flow instantly, generate profits, and serve the purchase of real-world goods and services, rather than being limited to speculative trading.

Lily Liu's classic definition: 'PayFi is a new financial market created around the time value of money, enabling new product experiences on-chain that traditional finance cannot achieve.' By 2025, PayFi has become a hot topic in the crypto industry, with stablecoin circulation exceeding $230 billion, average monthly trading volume reaching trillions of dollars, and traditional giants like Visa, PayPal, and Stripe actively engaging.

In simple terms, it refers to the ecological application scenarios of blockchain technology and cryptocurrency in traditional financial settlements and payments. (Not as grand as DeFi decentralized finance, but not small either.)

The core logic and operational mechanism of PayFi is instant settlement + programmable finance, leveraging blockchain to combine payments with DeFi/RWA. Key mechanisms:

Time value of money (TVM): A dollar today is worth more than a dollar tomorrow because it can be invested immediately. PayFi ensures that funds are 'never idle' through real-time settlement.

Instant settlement: Traditional payments take days to clear, while PayFi completes in seconds.

Programmable payments: Smart contracts automate execution, such as releasing funds based on conditions.

Integration of stablecoins + RWA + DeFi: Settle with stablecoins like USDC/USDT, tokenize real assets (government bonds, accounts receivable), and earn interest through lending.

Classic innovation model:

Buy Now, Pay Never: Deposit principal into DeFi lending protocols and use the generated interest for purchases. The principal remains intact, while the interest 'freely' buys coffee/subscription services.

For example, you deposit $50 and earn interest, using that interest to buy $5 coffee, achieving 'free consumption'.

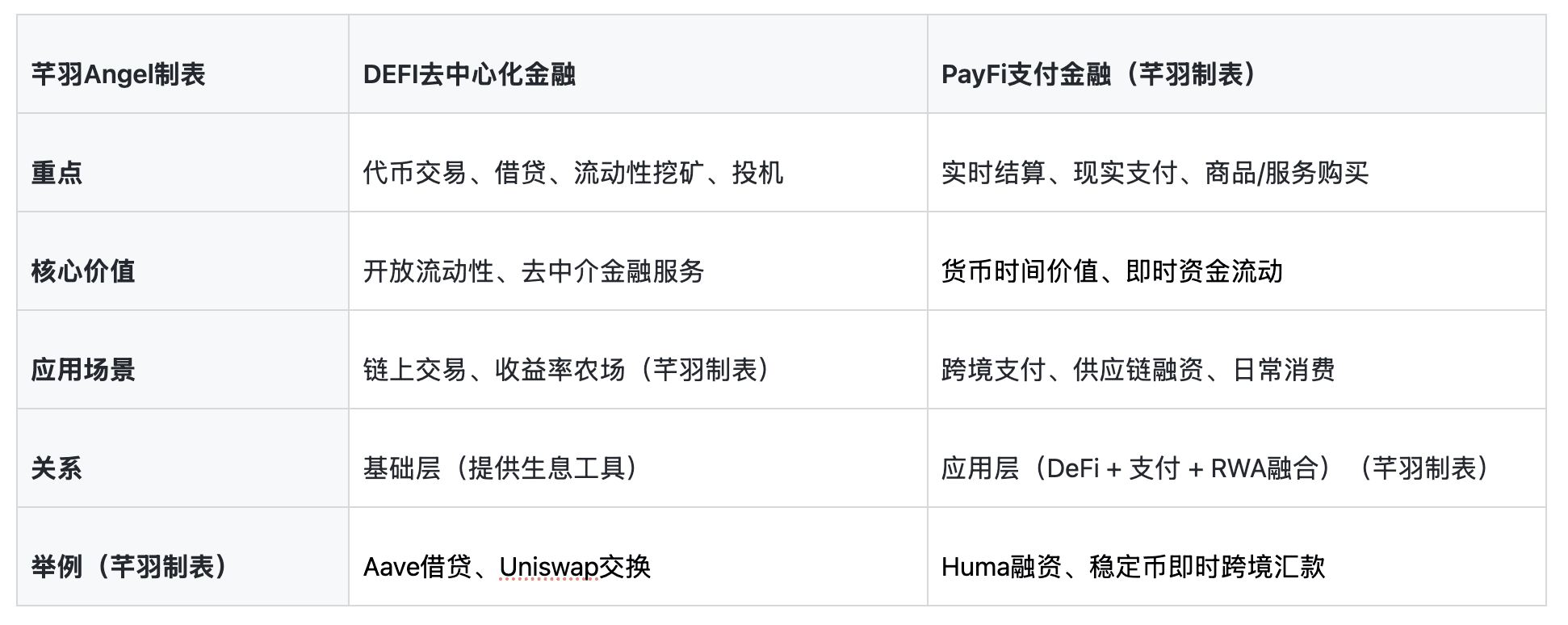

PayFi vs DeFi

Key distinction: PayFi is often seen as an extension of DeFi, but the two have essential differences:

PayFi is not a competitor to DeFi but rather a complementary evolution—DeFi provides 'money-making tools', while PayFi optimizes 'spending efficiency' using them.

What can PayFi do in reality?

PayFi has transitioned from concept to practical application, main scenarios:

Cross-border payments and remittances: Seconds-level low-cost settlement, replacing SWIFT (which traditionally takes 3-5 days with high fees).

Supply chain/trade financing: Tokenizing accounts receivable for immediate realization of future cash flow.

Daily consumption: Crypto cards/stablecoin payments combined with earning interest.

Creator economy: Real-time monetization based on progress.

Corporate credit/bill financing: Global private credit pool, allowing SMEs to obtain loans quickly.

RWA applications: Tokenizing government bonds/money market funds, earning interest while holding, used for payments.

2025 data: Stablecoin trading volume exceeds Visa's annualized volume, PayFi is serving unbanked populations, promoting financial inclusion.

Advantages and benefits of PayFi

Efficiency: Settlement in seconds, low fees (<$0.01 per transaction).

Inclusivity: All you need is a mobile phone + internet, no bank account required.

Innovative earnings: Spend 'for free' using interest, unlocking TVM.

Transparent and secure: Blockchain is tamper-proof, reducing fraud.

Global: 24/7 without borders, suitable for cross-border/emerging markets.

Compared to traditional payments: time-saving, cost-saving, and more flexible.

Risks and challenges of PayFi

Despite its immense potential, issues still remain:

Regulatory uncertainty: Different countries have varying legislation on stablecoins/crypto payments (such as the EU's MiCA and the US's GENIUS Act in progress, but many gray areas exist).

Volatility risk: Although stablecoins are used, there are risks of hacking related to underlying assets/protocols.

Scalability: Fees increase during network congestion (Solana and others are optimizing).

Adoption thresholds: User education and compliance KYC need to balance privacy.

Systemic risk: Smart contract vulnerabilities, insufficient liquidity.

PayFi is moving from the crypto circle to the mainstream, achieving 'free flow of money'. It is not only a technological upgrade but also a democratization of finance—allowing everyone to use future earnings to pay for today's living.