On November 20, 2025, a little-known medical AI startup made a 'counterintuitive' deal on the Kite network:

Its diagnostic agent had no collateral but obtained a GPU computing power credit of 100,000 USDC from a computing power lending protocol.

There was only one piece of collateral —

the 980 reputation points accumulated by that agent on the Kite chain.

At this moment, DeFi has transitioned from 'using assets as collateral' to a new stage of 'using credit for financing.'

And Kite is doing something that sounds crazy for billions of AI agents in the future:

Send an on-chain credit report to every 0x address.

Kite credit system: turns on-chain actions into 'loanable assets'

Kite builds this system using its own Proof of Chain architecture.

The distinction is simple:

Traditional e-commerce five-star reviews can be faked;

Kite's credit score can only be accumulated through unalterable on-chain actions (Proof of AI).

Every positive action will be recorded:

Agents complete a payment as agreed

Respond to an API request on time and accurately

Long-term compliance with SLA, no random shutdowns, no defaults

All of these have been written on-chain by oracles:

Turning off-chain response times, success rates, and dispute records into verifiable data points, attached to this agent's address.

Technical dimension:

Credit score = a complete, unalterable behavior timeline.

Economic dimension:

High credit scores are not just for show; they are tangible privileges:

Higher Spending Limit

Lower fee discounts

Obtain qualification for 'unsecured limits' in computing power/liquidity protocols

Regulatory dimension:

Every point addition or subtraction has an on-chain record to check,

This makes Kite's credibility system inherently compliant with 'explainable AI' requirements—

It is not a black box giving you 980 points, but a behavior ledger that anyone can review.

From the hell of cold starts to 'transferable credit': breakthrough in credit for AI agents

Before Kite, the biggest pain point for AI agents could be summed up in one sentence:

'You are a new account, why should I trust you?'

The newly deployed trading robot, due to lack of history, is treated as a high-risk user by all service providers

Either required to prepay a large deposit

Or directly blocked by risk control rules

The result is:

Only the 'favorite agents' of large companies can walk freely in their own ecosystem,

Excellent agents created by small and medium teams can only play in the corners.

Kite directly dismantled this threshold—

Credibility is transferable (Portable Reputation):

You have 1000 timely settlements and 0 disputes in the financial module

Then run to the legal module, data labeling module,

No need to brush 'good reviews' again, your high credibility directly follows the address

Trust has become an asset that can be reused across scenarios for the first time,

No longer isolated by individual app walls.

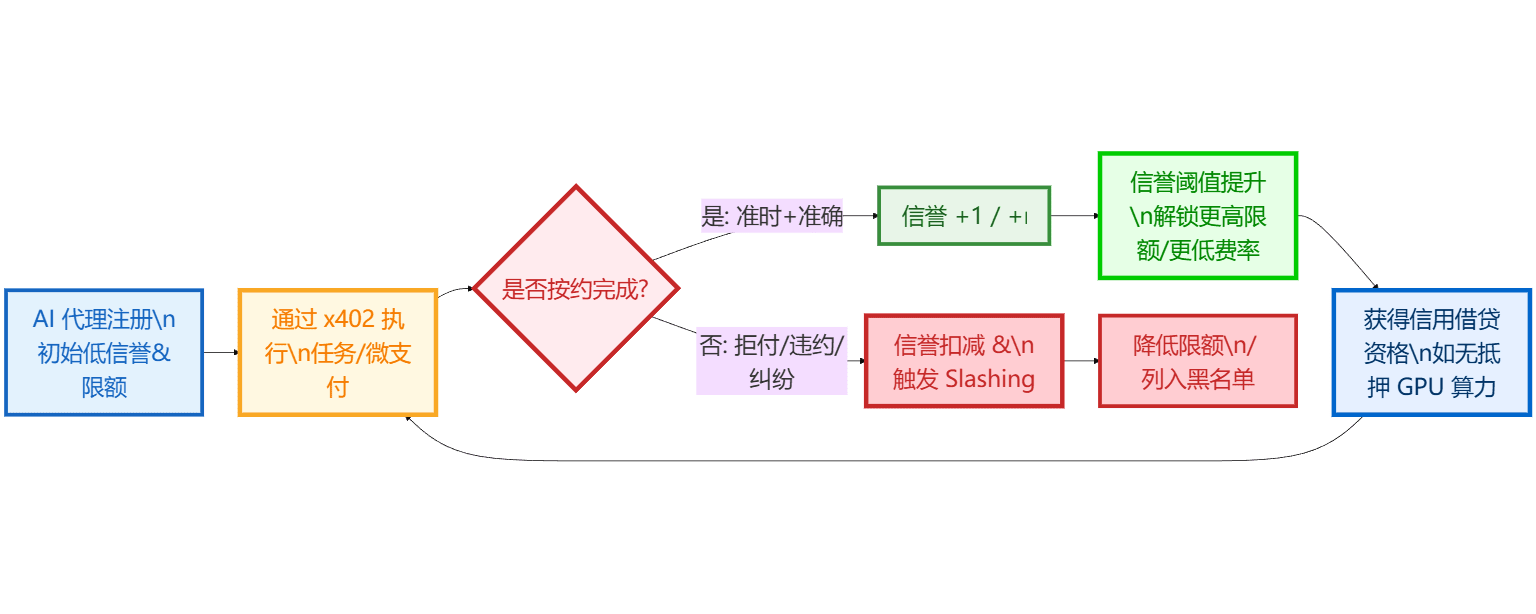

Accumulated point by point: how is Kite's credit score calculated?

From a practical perspective, Kite building credit for AI agents is actually a tight loop.

Initial state: blank account

New agent registers on-chain → gets a low credibility starting point + strict limits

For example: a maximum daily expenditure of $10, only able to run very small tasks

Daily behavior: use x402 to slowly 'build a resume'

Initiate micro-payments through the x402 protocol

Every payment is settled on time, with no disputes, and you gain a little credibility

Timeouts, refusals, repeated failures will incur points deduction

Violation costs: double whammy of credibility + assets

If an agent maliciously defaults, forges data, or repeatedly breaches contract:

Credit points will be significantly deducted

Trigger economic penalties (Slashing)

Severe cases will be directly blacklisted across the network, and subsequent modules will refuse service

Positive cycle: high score = higher authority

When an agent maintains a long-term contract, credit points rise to 900+

The system automatically raises its limits and lowers fees,

Even like the previous medical case, offering unsecured computing power credit

To view Kite's 'credit production line' in one picture:

What PayPal Ventures is interested in is the logic behind this production line:

Whoever seriously manages their on-chain resume will get cheaper funding;

Whoever wants to take advantage and run will be kicked out by the system.

This is the reverse reality version of 'good money drives out bad money.'

Data speaks: why is the funding cost for high-credit agents lower?

After running the testnet for half a year, the numbers have begun to provide direction:

The API call success rate of high-credit agents is about 40% higher than that of new accounts

Service providers are more willing to prioritize high-score agents' requests

Average transaction costs have decreased by about 25%

Discounts and multi-tiered rates are all reflected in the prices

Credit loan default rate based on credibility < 0.1%

Far below the level of traditional P2P lending.

Behind this is actually a very simple conclusion:

For AI agents planning to operate long-term,

Maintaining their on-chain credibility,

Is much more rewarding than just taking advantage and running.

Kite does not rely on moral education telling agents 'to be a good robot',

It simply writes all rewards and penalties into mathematics and contracts.

Rational agents will naturally choose the long-term side after completing arithmetic problems.

On-chain FICO: Kite turns 'trust' into programmable assets

Looking from a higher level, what Kite is doing is essentially moving FICO credit scores into the AI world:

In the human financial system,

Credit scores determine whether you can get a loan at a 3% interest rate for a house

In Kite's machine economy,

Credit scores determine whether your agent can obtain computing power/liquidity with zero collateral

The difference is:

Traditional FICO is controlled by black-box models + centralized institutions;

Kite's credibility layer is shaped by public contracts + verifiable behaviors;

Any change can be traced and questioned by the community on-chain.

The significance for the entire track is also very direct:

To AI developers: No longer just 'throwing an agent on-chain to take a gamble',

But can build a long-term cash flow business around a highly credible agent.To Kite ecosystem: The credibility layer combines payment layer, PoAI, Piggy Bank,

Making the network more willing to lend and better at pricing, the underlying economic effects will continue to amplify.To Investors and CreatorPad reviewers:

This is not just a 'chain with AI concepts',

But a set of forming machine-based credit infrastructure.

When the next wave of AI agent narratives truly erupts,

Agents without on-chain credibility can only knock on the door from outside;

And those addresses that scored high early in Kite,

Are already leveraging pure credit to access computing power, data, and liquidity.

I am searching for a sword by the boat,

On the curve of on-chain FICO, I see the credibility of each agent,

Is slowly growing into a real asset that can be pledged and financed.@KITE AI $KITE #KITE