This article will overturn your understanding. Insurance and the big pancake, these two completely unrelated subjects, actually have many similarities.

In recent years, insurance in Hong Kong has become very popular. Many middle-class people choose insurance as a financial tool for their assets to maintain and appreciate value, achieving an annualized return of 6.5% on the basis of capital preservation.

What does the big pancake have to do with insurance? Because the big pancake can also achieve capital preservation.

Don't be deceived by the drastic price fluctuations of the big pancake. Let me tell you a cold fact that 99% of people don't know. On any given day, the price of the big pancake will always be higher than the price on the same day four years ago. If you don't believe it, you can check it out; if you find it, I'll admit defeat.

Since it can guarantee the principal, the essence of Bitcoin is similar to that of a savings insurance policy. Holding for 4 years is equivalent to a lock-in period, during which you may earn or lose money.

However, after 4 years, the probability of making a profit is almost 100%, and the returns are much higher than those of savings insurance. If you understand some timing methods, this 4-year period can be shortened further, and the returns can be even higher.

So if you are buying insurance with the purpose of financial management, it is indeed better to buy Bitcoin. Additionally, having a Hong Kong card to allocate cryptocurrency assets is very convenient. However, if you are buying for the functional attributes of insurance, that is another matter.

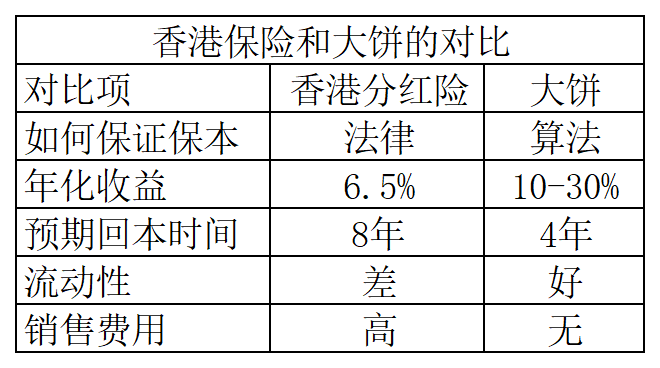

Below, I have created a comparison table that contrasts the differences between Hong Kong participating insurance and Bitcoin.

First point, both of these options guarantee the principal. The guarantee of the insurance is stipulated by law and regulations, and the cash value of the policy will be written in the insurance contract.

The specific principle is that the insurance company's asset allocation is mostly placed in bonds, with a small portion invested in stocks, and diversified globally. After an investment period of more than ten years, the probability of loss is very small, and naturally, the principal can be preserved.

The principal guarantee mechanism of Bitcoin is determined by algorithms; every 4 years, Bitcoin's production will be halved. This mechanism establishes a fixed bull-bear cycle, ensuring that holding for 4 years will not result in loss.

Second point, product returns. The annualized return of Hong Kong participating insurance is 6.5%, while Bitcoin's 4-year annualized return, at its lowest, is 9%. In the recent cycle, the average can reach 20%. If you understand some timing methods, the returns can be even higher.

Third point, expected break-even time. The average break-even time for Hong Kong participating insurance is around 7 years, while for Bitcoin, it is 4 years.

Fourth point, liquidity. The liquidity of Hong Kong participating insurance is very poor; after purchasing, you have to hold it for 7 years to break even. Bitcoin has very good liquidity, trading 7×24 hours, and can be bought and sold at any time.

Fifth point, sales costs. For Hong Kong participating insurance, the commission of sales personnel plus the operating costs of the insurance company account for about 10-15% of the principal. Bitcoin, on the other hand, is a publicly traded asset with no sales costs.

With this comparison, it becomes very clear: both are products that guarantee the principal, so why not buy the higher-yielding Bitcoin instead of Hong Kong insurance?

Bitcoin price at the time of writing: $86,000