The crypto market staged a familiar drama again in December 2025: Bitcoin continued to decline after hitting a closing price of $90,360 in November, briefly falling below the $84,000 mark in mid-December. The global liquidation amount reached $591 million within 24 hours, with 193,000 investors being liquidated.

And this morning it fell to $85,000, breaking the $2,900 mark; this is not an isolated event—looking back at the history of cryptocurrency development, Bitcoin dropped from $6,000 to $3,815 before Christmas in 2018, the 2022 FTX collapse compounded by the Christmas cycle saw Bitcoin's price halve to $16,831, and in 2014 and 2015, there were also varying degrees of pre-holiday corrections. This 'Christmas curse' is not accidental, but an inevitable result of quarterly contract delivery, institutional capital recycling, and the resonance of human daily routines.

Part 01

Empirical Data: The Plunge Before Christmas is a High-Probability Event

The 'Christmas Effect' in the cryptocurrency market is not a subjective conjecture, but rather a seasonal pattern supported by clear data.

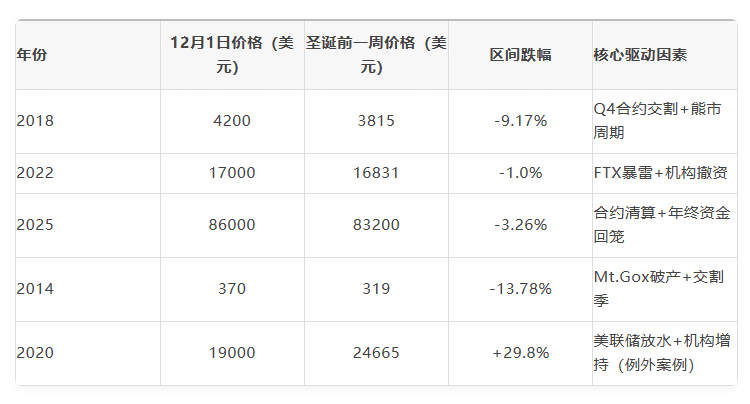

Taking Bitcoin as a sample (which accounts for over 58% of the total market value of cryptocurrencies and serves as a bellwether), in the 15 Christmas cycles from 2010 to 2024, there were 11 instances of declines in early to mid-December, followed by narrow fluctuations in late December, with a drop probability of 73.3%. Notably, the years 2021-2023 exhibited pre-holiday correction characteristics for three consecutive years. Only in 2024 did strong positive factors such as the Federal Reserve's interest rate cut and approval of Bitcoin ETFs break the pattern, further confirming the judgment that 'macro environment is the core variable.'

From the data, it can be seen that, except for special macro environments such as the Federal Reserve's unlimited QE in 2020, interest rate cuts in 2024, and ETF expectations, the downward trend before Christmas is the mainstream trend.

The plunge before Christmas in 2021 was particularly typical. On December 1, Bitcoin's price was still at a high of $59,000; within two weeks, due to the dual impact of the Omicron variant spread and tightening monetary policy expectations from the Federal Reserve, compounded by the December quarterly contract delivery, the price plummeted to $47,850, with a drop of 18.9%. During this period, the total liquidation amount across the network peaked at $2.23 billion. The most direct driver behind this regularity is the quarterly contract delivery mechanism in the cryptocurrency derivatives market.

Part 02

Core Driver: The 'Liquidity Black Hole' of Quarterly Contract Delivery

The proportion of leveraged trading in the cryptocurrency market has long remained above 60%, and quarterly contracts, as the most commonly used derivative tool by institutions, have overlapping delivery cycles with the Christmas node, forming the core engine of market volatility.

Currently, the quarterly contracts of major global exchanges follow the rule of 'expiring on the last Friday of the last month of each quarter'. For example, in 2024, BitMEX's BTCUSD_Z24 contract and Binance's ETHUSD_1224 contract are both set to expire on December 27, which is exactly the first working day after the Christmas holiday (December 25).

The 'Forced Liquidation Wave' Before Delivery

In the 1-2 weeks before the expiration of quarterly contracts, the market enters a 'position shifting' cycle. Due to bank transfers, capital clearing, and other services being suspended during the Christmas holiday, institutions typically complete position adjustments a week in advance to avoid holiday uncertainties. When many institutions simultaneously close old contracts, it triggers a phase of concentrated selling. From December 1 to December 20, 2025, CoinGlass data shows that the open interest of Bitcoin quarterly contracts plummeted from $20 billion to $15 billion, while the spot trading volume fell from $61 billion to $48 billion during the same period. This 'reducing positions without replenishing' behavior directly led to downward pressure on prices.

More dangerously, the chain reaction of high-leverage positions. When prices see a slight decline, long positions with leverage exceeding 5 times will trigger automatic liquidation, and the selling of liquidated positions can lead to a new round of declines. On December 15, 2025, Bitcoin fell only 2.3%, yet triggered $199 million in BTC liquidations and $135 million in ETH liquidations, as market leverage surged to an annual high of 8.2 times just before delivery.

Liquidity Contraction of Market Makers

Before the Christmas holiday, leading market makers such as Jump Crypto and Jane Street will significantly reduce liquidity supply. Market makers' core profits come from the bid-ask spread, and low trading volume during the holiday will lead to widened spreads and increased risk. The week before Christmas 2023 was particularly prominent, as Bitcoin experienced a sudden pullback after consolidating at the $44,700 resistance level, with Coinbase's Bitcoin bid-ask spread widening from 0.1% to 0.3%, and Ethereum's spread from 0.15% to 0.45%. Compounded by the high market leverage (open interest increased by 30% compared to November), this eventually triggered a price drop of 5.82%. The sudden withdrawal of liquidity diminished the market's ability to absorb sell-offs, causing small sell orders to result in significant declines.

This liquidity contraction was particularly extreme in 2022. At that time, the FTX collapse triggered a trust crisis, compounded by the Christmas delivery cycle, causing market makers to almost completely suspend cryptocurrency trading services. Bitcoin experienced a 'flash crash' on December 20, with the price dropping from $17,000 to $15,500, a single-day decline of 8.8%, while the trading volume that day was only 50% of the usual.

Part 03

Institutional Behavior: The 'Capital Recycling Curse' During Christmas Holidays

The 2025 a16z report shows that institutional funds have accounted for half of the crypto market, with spot ETF holdings reaching $175 billion, accounting for 12% of Bitcoin's circulating market value. The year-end financial cycles of these institutions highly overlap with the Christmas holiday, and their capital operation logic directly governs the pre-holiday market.

The 'Take Profit' Demand at Year-End Settlement

Western financial institutions generally use December 31 as the fiscal year-end, and the 2-3 weeks before Christmas is a critical period for year-end settlement. For high-risk investments like crypto assets, institutions prioritize reducing holdings to lock in annual profits. In December 2025, Bitcoin ETFs from Fidelity, BlackRock, and others saw an outflow of $226.56 million, while Ethereum ETFs had inflows, but the overall net outflow of crypto ETPs reached $102 million, directly suppressing market sentiment.

This behavior has clear regularity. After Bitcoin set a historical high of $69,000 in November 2021, it experienced concentrated selling by institutions in December, with prices falling back to $47,850 before Christmas, a drop of 18.9%. During the same period, Grayscale's GBTC redemption volume reached $1.5 billion, hitting an annual high, as many institutions chose to lock in yearly profits at the year-end. Although the drop in 2023 was relatively moderate, Fidelity's crypto fund also saw a net outflow of $12 million, confirming the fund withdrawal effect at year-end settlement.

Defensive Withdrawal of Funds for Holiday Risk Control

The Christmas holiday usually lasts for 10-14 days, during which the financial markets in Europe and the US are closed, and services such as bank transfers and compliance checks are suspended. To avoid being unable to respond to sudden risks during the holiday, institutions typically convert crypto assets into fiat or stablecoins in advance. In the week before Christmas 2024, the market capitalization of USDT increased from $90 billion to $93 billion, and USDC rose from $55 billion to $57 billion, highlighting a stark contrast between the substantial increase in stablecoins and the decline in Bitcoin, reflecting the shift of funds from risk assets to safe-haven assets.

This defensive withdrawal of funds creates a feedback effect between traditional finance and the crypto market. Wall Street strategists point out that the 'Christmas rally' in US stocks in 2025 was absent due to the impact of AI technology, with the S&P 500 index falling 3.5% in December, and the weakness of traditional risk assets further intensified the institutions' reduction in crypto holdings, creating 'double selling' pressure.

Part 04

Social Psychology: The 'Resonance of Human Daily Routines' in Trading Behavior

Although the cryptocurrency market is known as '7x24 hours without rest', the human attributes of the participants determine that it cannot escape the influence of daily routines. As the most important traditional holiday in the West, the behavioral changes triggered by Christmas resonate through trading psychology into the market.

Seasonal Diversion of Trading Attention

Around Christmas, traders' attention shifts from the market to family life. According to Glassnode data, from December 20 to December 30, 2023, the number of active Bitcoin addresses on the chain dropped from 1.2 million to 800,000, a decrease of 33.3%; Ethereum's daily transaction volume fell from 1.2 million to 850,000, a decrease of 29.2%. The decrease in trading participation led to increased market volatility—when buying power weakens, a small amount of selling can trigger significant price fluctuations.

This attention diversion is more pronounced at the institutional level. After December 20, 2025, among the 10 leading crypto funds tracked by Cointelegraph, 8 paused releasing market analysis reports, and the frequency of trading decisions dropped from an average of 3 times a day to once every 3 days, significantly decreasing the activity level of 'smart money' in the market, further weakening market stability.

The 'Year-End Convergence' of Risk Appetite

From the perspective of behavioral finance, humans tend to exhibit 'risk aversion' psychological characteristics at year-end. Whether individual investors or institutional traders, there is a tendency to reduce risk exposure at year-end to avoid unexpected price movements impacting annual returns or performance assessments. The Fear and Greed Index for December 2025 remained in the 'extreme fear' range of 24, which is at the same level as 22 before Christmas 2022 and 20 in 2018, reflecting the seasonal convergence of market sentiment.

The behavior of individual investors further amplifies this sentiment. In the two weeks before Christmas 2024, CoinGecko's cryptocurrency search index fell by 45%, Binance's individual user trading volume dropped by 52%, and the ordinary investors' mindset of 'taking profits for Christmas' resonated with institutional behavior, jointly pushing prices down.

Part 05

Exceptions and Insights: Not an Inevitable 'Christmas Curse'

It should be noted that the plunge before Christmas is not an absolute rule, as significant changes in the macroeconomic environment can break this cycle. Before Christmas in 2020, the Federal Reserve launched an unlimited QE policy due to the pandemic, leading to excess market liquidity, with Bitcoin rising from $19,000 on December 1 to $24,665 before Christmas, an increase of 29.8%. The exception in 2024 is even more representative, as the Federal Reserve announced its third interest rate cut of the year to the range of 4.25%-4.50% in December, coupled with strong expectations for the approval of a spot Bitcoin ETF, causing Bitcoin to rise from $92,000 on December 1 to $98,200 before Christmas, an increase of 6.74%. Even facing quarterly contract delivery pressure, positive factors still dominated the market direction.

These exceptional cases reveal a core logic: when the positive force of macro liquidity exceeds the negative forces of contract delivery and capital recycling, the market tends to show an upward trend before Christmas. For investors, establishing a three-dimensional analytical framework of 'macro environment-contract cycle-market sentiment' is crucial.

Macroeconomic Level: Focus on the Federal Reserve's interest rate decisions, inflation data, and other core indicators; a liquidity easing cycle can weaken Christmas bearishness.

Contract Level: Use tools like CoinGlass to track quarterly contract delivery dates and changes in open interest to avoid moving contracts at month-end risks in advance.

Sentiment Level: When the Fear and Greed Index is below 30, one can buy quality assets at lows; when above 70, one should be wary of pre-holiday corrections.

Part 06

Conclusion: The Market Nature Behind the Cycle

The 'plunge before Christmas' in cryptocurrency is not a mysterious curse, but rather the result of the interplay of financial market regularities, institutional behavior logic, and human social attributes. Quarterly contract delivery provides a 'technical trigger point', the capital recycling by institutions constitutes a 'funding pressure source', and the attention diversion triggered by the Christmas holiday forms an 'emotional amplifier', creating this seasonal phenomenon.

As the crypto market matures (with the total market value surpassing $4 trillion in 2025 and institutional holdings exceeding 50%), this seasonal volatility may gradually weaken. However, as long as human daily routines and institutional financial cycles remain unchanged, market adjustments before Christmas will continue to exist in some form. For investors, understanding the underlying logic behind this cycle is more valuable than simply predicting price movements—it helps maintain rationality amid market noise and seize opportunities within the regular fluctuations.

Do you think Christmas will be a Christmas disaster? Feel free to leave comments for discussion!