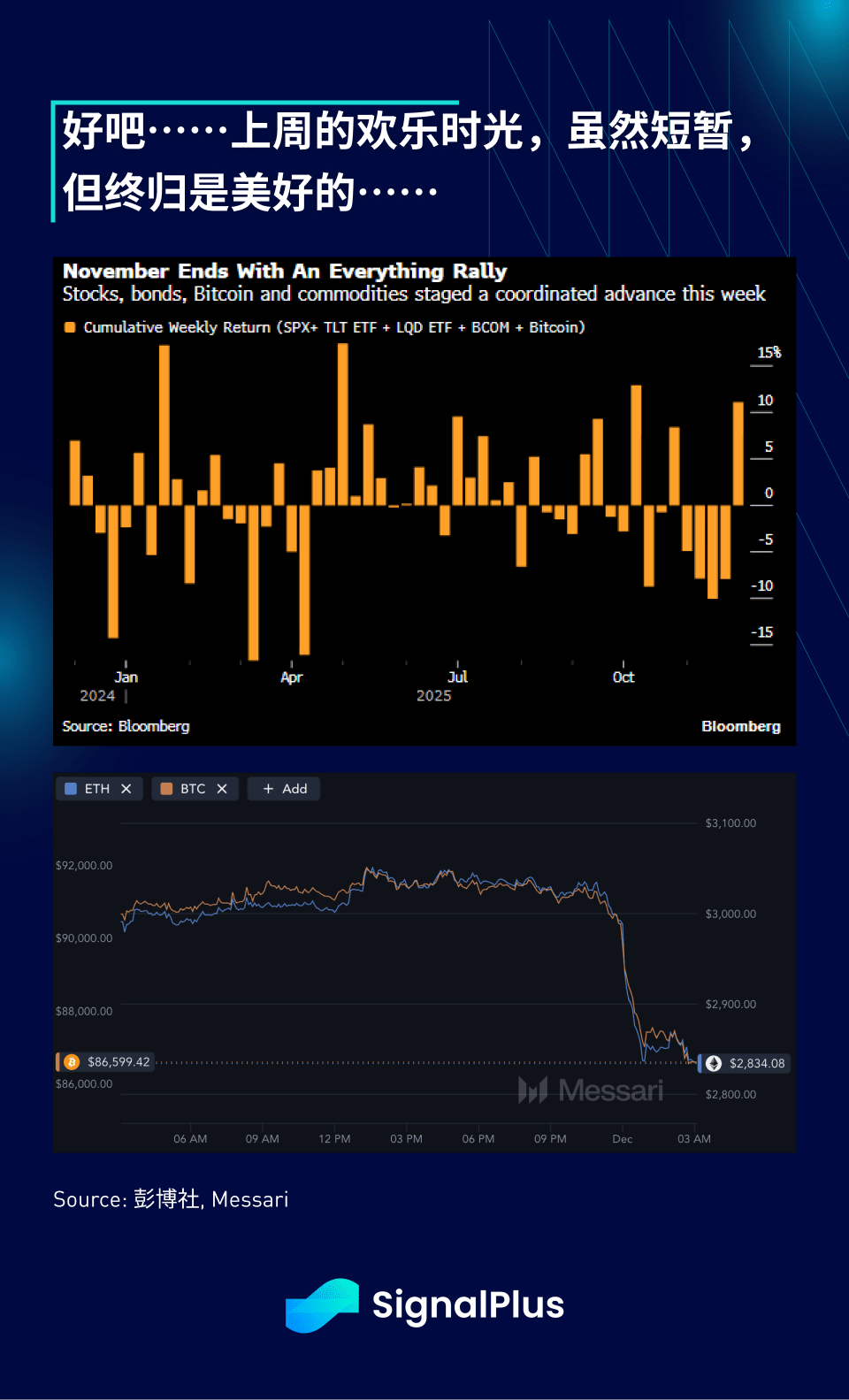

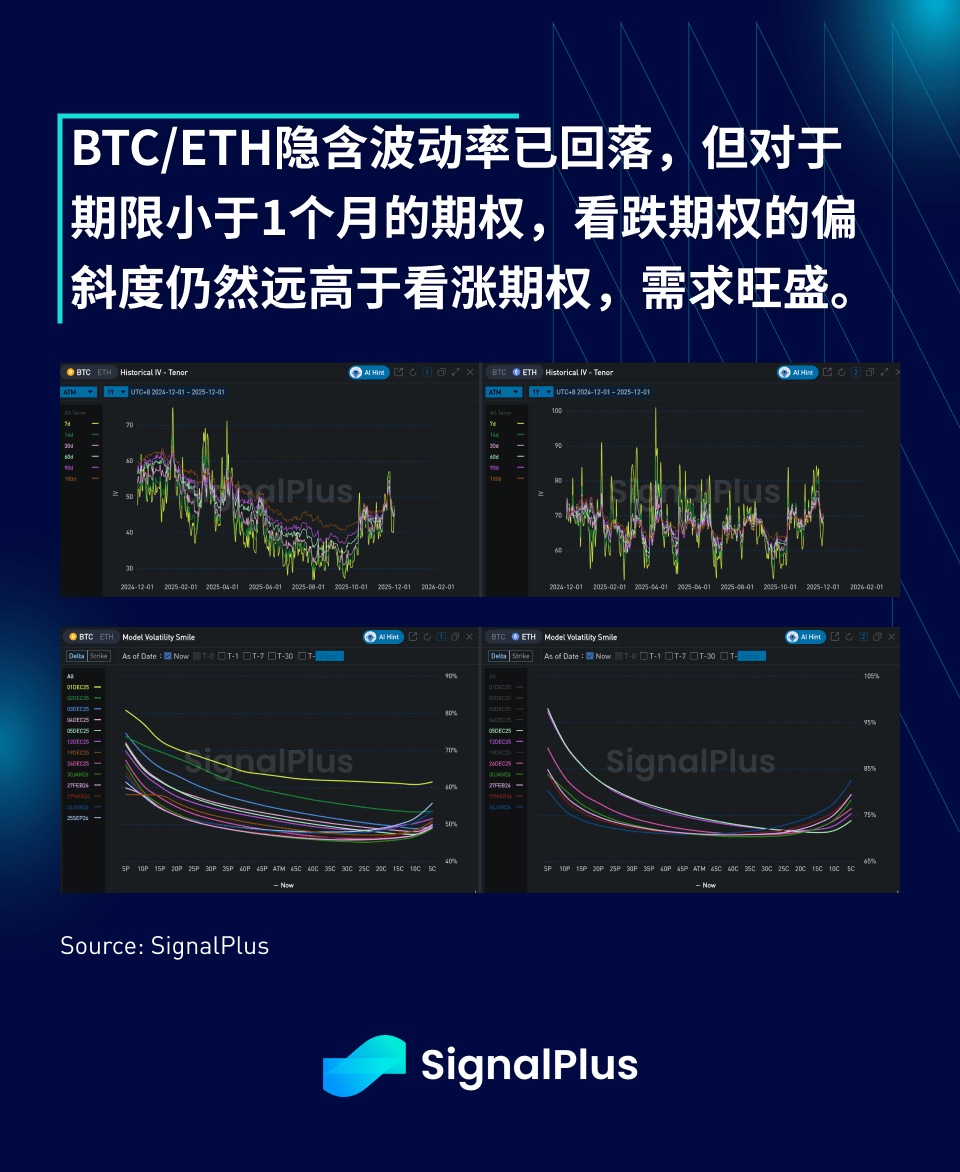

The market has taken a sharp downturn. Following a strong rebound in risk appetite on Friday, cryptocurrency prices suffered a significant drop as December began, with BTC falling below $87,000 again during the quiet trading period in Asia due to stop-loss selling.

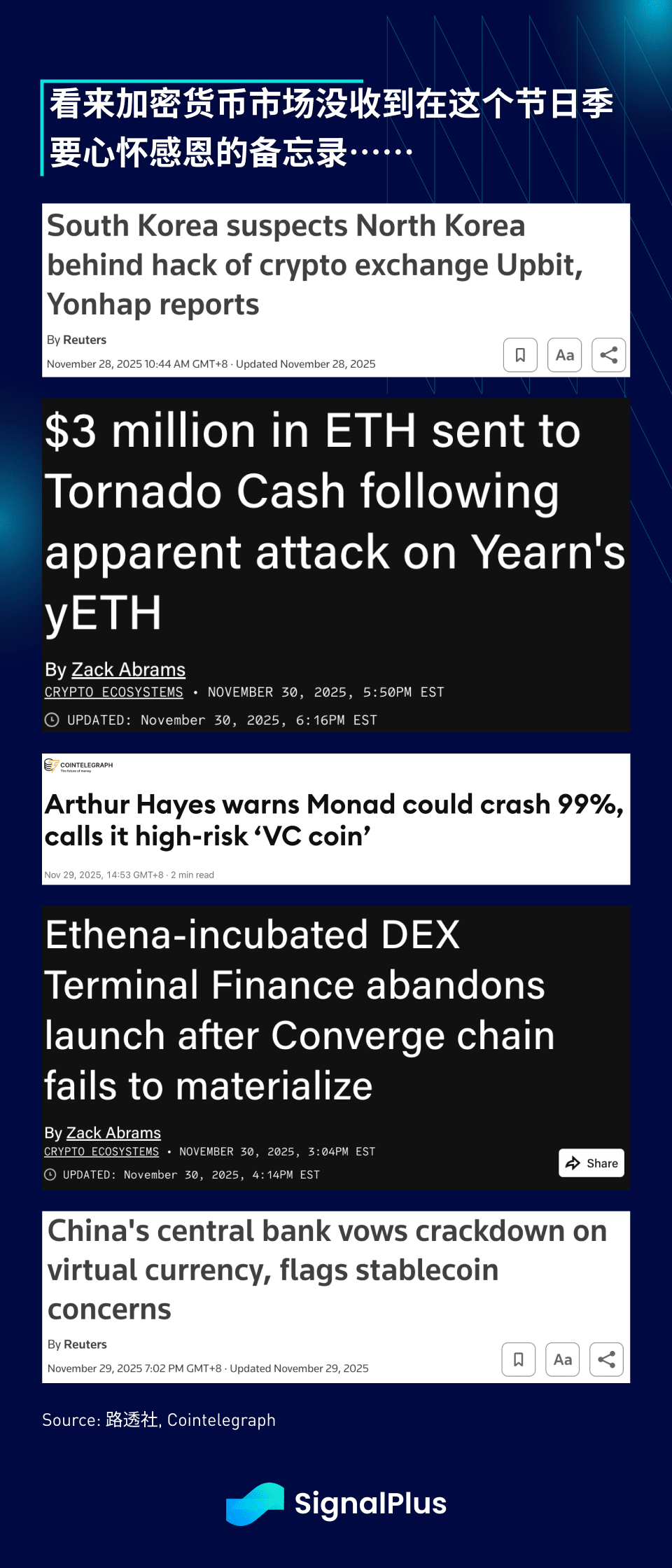

While it is difficult to attribute this to a single cause, overall risk appetite remains fragile after the market cleansing in October and November, and a series of negative headlines that have emerged in recent trading sessions exacerbated the decline. Another OG protocol's DeFi was hacked (Yearn staking), a DEX terminal abandoned its highly anticipated launch due to a challenging market environment (Terminal Finance), OG Arthur Hayes publicly expressed his pessimism about the recent Monad ICO (implying a 99% drop potential), S&P downgraded USDT's rating to 'weak' (insufficient information disclosure), and the People's Bank of China reiterated its cautious stance on cryptocurrency trading and stablecoins — Overall, we have reason to believe that we remain firmly in a bear market until further notice.

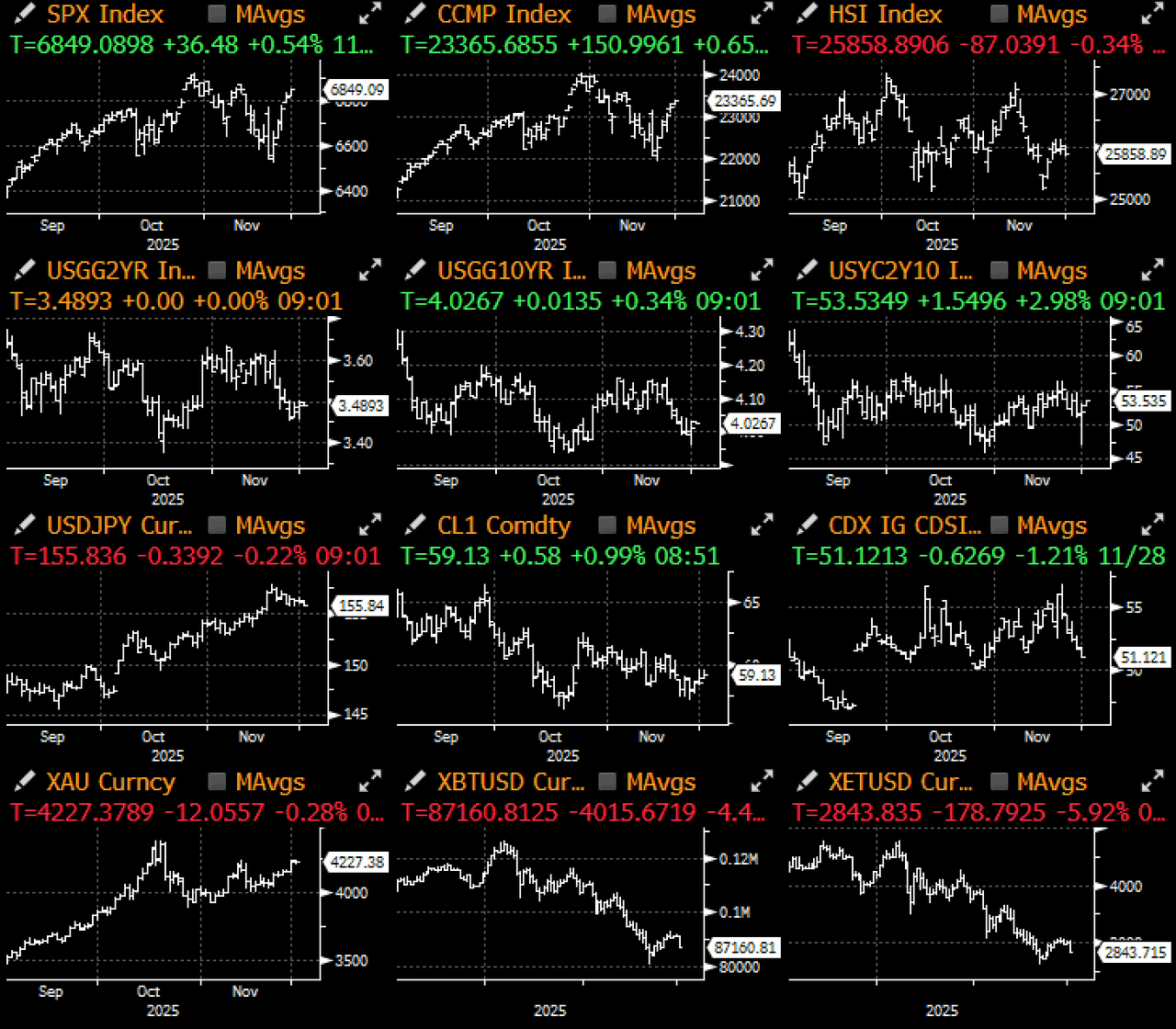

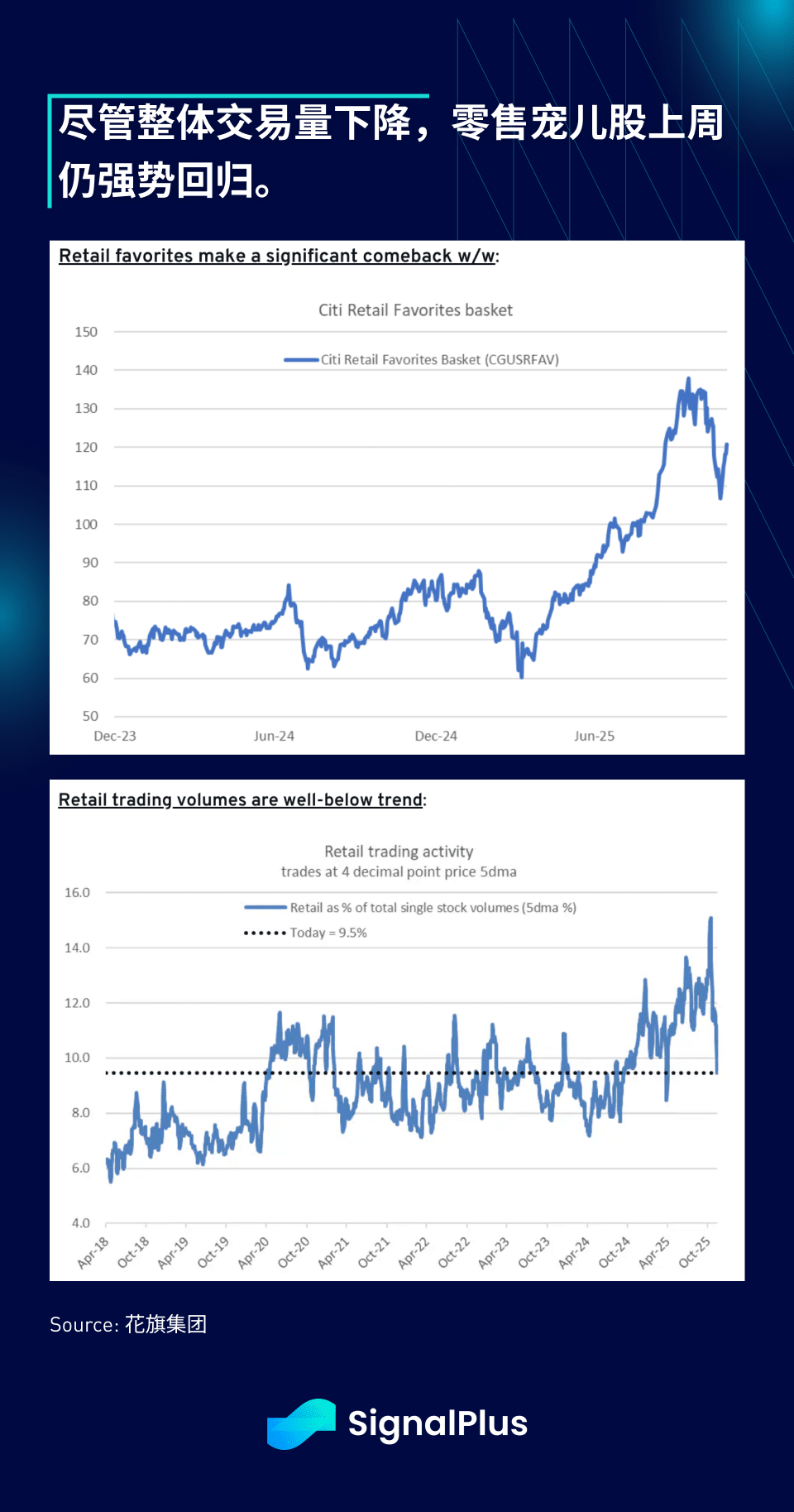

In the stock market, the S&P 500 index rose 3.7% last week, led by the semiconductor sector (+5.4%) and the retail sector (+4.7%). Despite an overall decline in retail trading volume, retail darling stocks still achieved a strong weekly rebound.

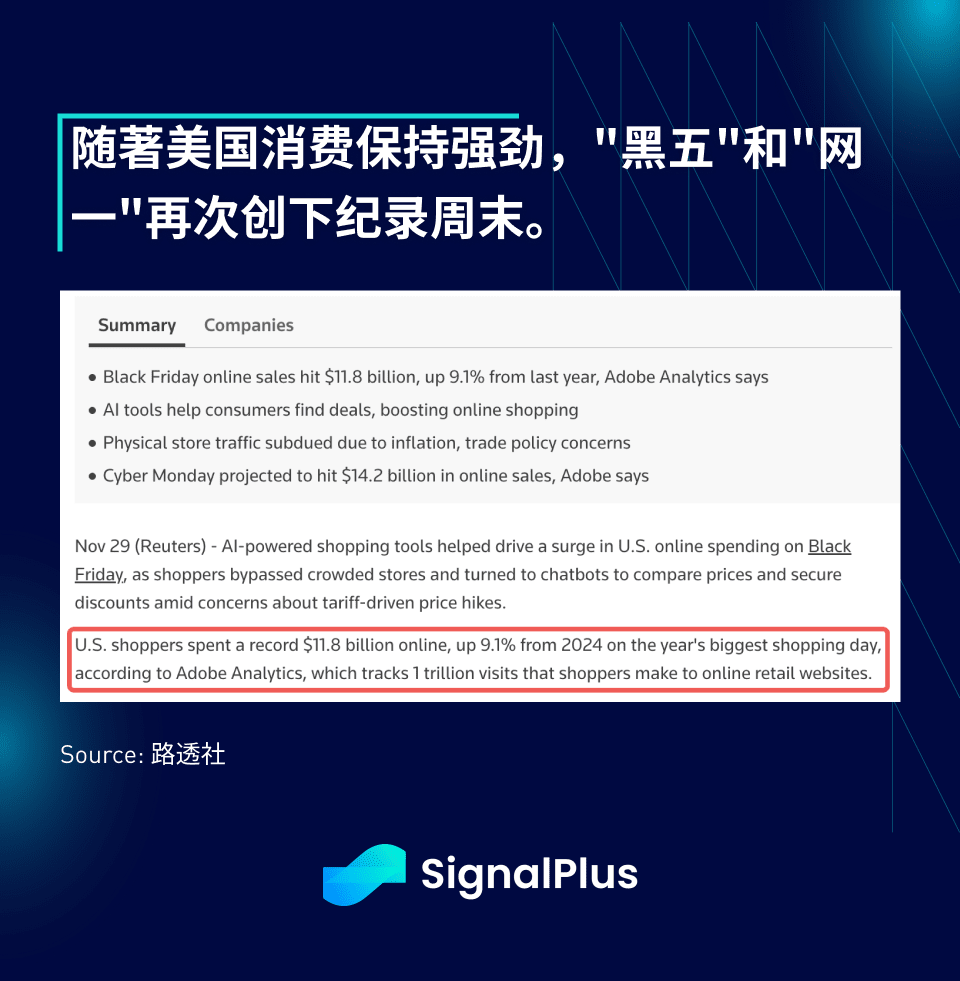

Moreover, early signs from Black Friday sales indicate that we have set another record, with online sales reaching nearly $12 billion (a 9% year-on-year increase), a historic high, while Cyber Monday is expected to bring in another $14 billion in revenue. So far, consumer spending in the U.S. seems to remain strong.

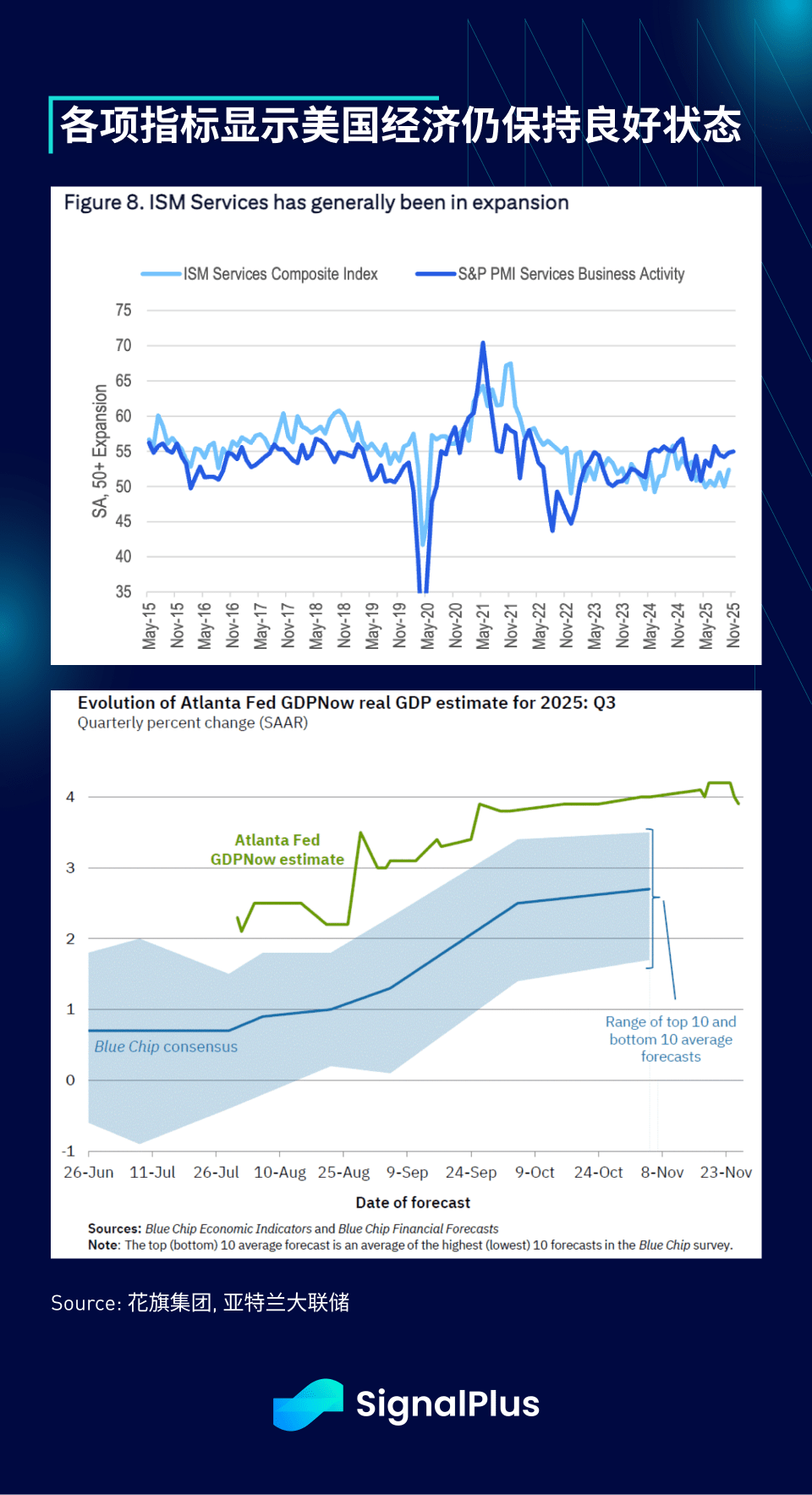

In addition to holiday sales, this week's economic calendar is quite busy, with data such as ISM, ADP, initial jobless claims, PMI, and the University of Michigan Consumer Confidence Index being released. Despite ongoing market noise, the PMI index has been slowly rising within a healthy expansion range of 50–55 since 2022, and the Atlanta Fed's GDPNow model continues to predict that the economic growth rate will be above Wall Street expectations, indicating that the economic fundamentals remain strong.

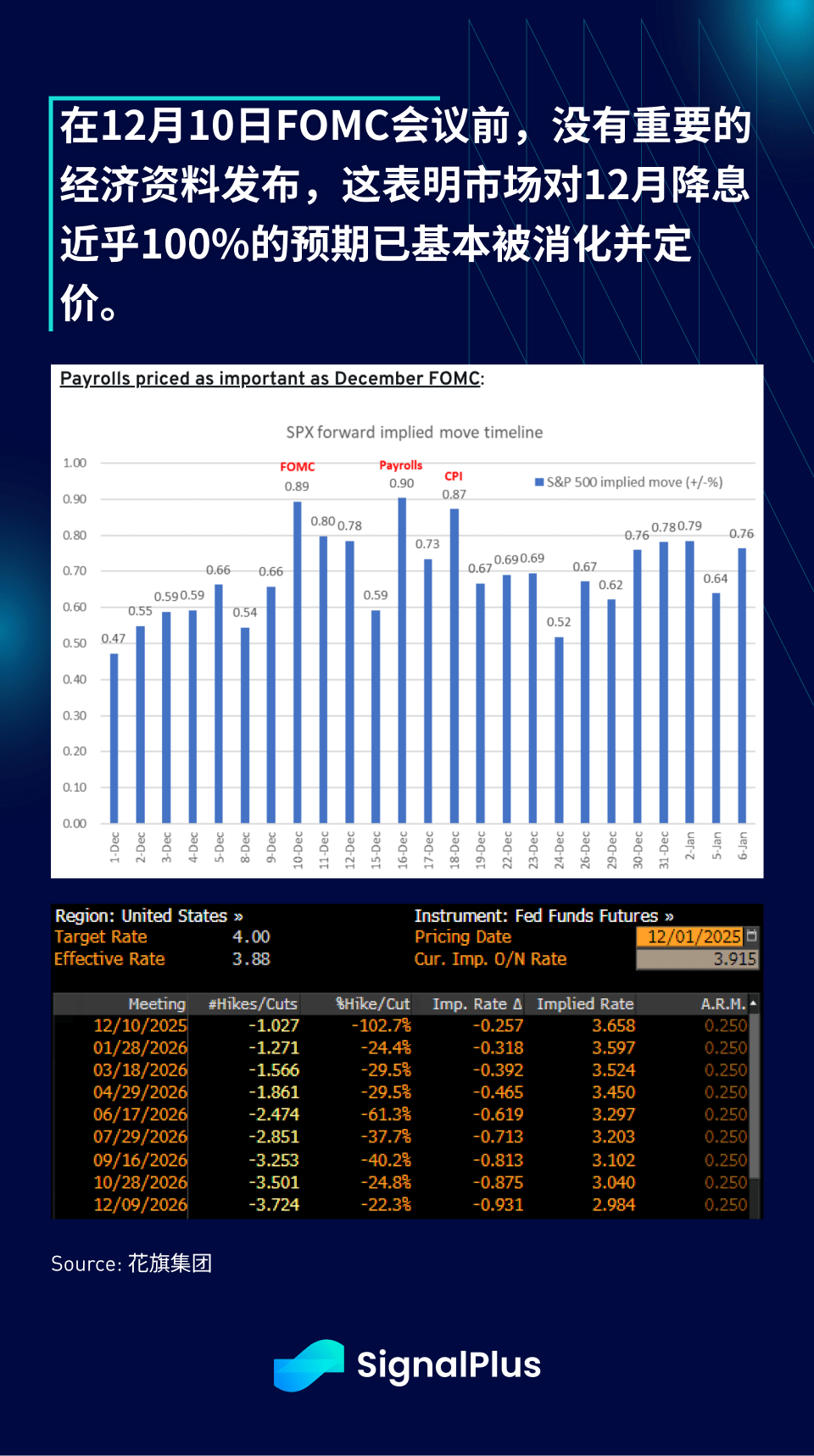

The most important economic data dates for the remainder of this year will be in the next two weeks: the FOMC meeting on December 10, followed by the non-farm payroll data delayed until December 16, and the CPI data on December 18. Additionally, it is worth noting that there will be virtually no first-tier economic data released between now and the FOMC meeting date, so the market's nearly 100% expectation for the Fed to cut interest rates has been largely priced in (as the Fed typically does not tend to let market expectations fall short unexpectedly). The focus will be on the guidance language regarding the policy path for 2026, rather than the interest rate decision itself.

Specifically, we will focus on how the Fed comments on its increased confidence in the waning inflation pressures, in relation to the weak labor market and tightening market conditions, to justify a 'dovish rate cut', and vice versa. The minutes will also scrutinize how many participants leaned towards maintaining interest rates unchanged as a dissent, especially in the context of the yet-to-be-released NFP and CPI reports. Additionally, how Powell responds during the Q&A session regarding the inflation gap and unemployment gap will also be noteworthy. As the meeting approaches, we will provide a more detailed interpretation of the Fed meeting.

Good luck and happy trading!