Something weird happened last month that nobody in crypto seemed to notice. A major gaming publisher quietly shelved their blockchain integration project after spending two years and roughly $40 million on development. The official reason was “strategic realignment” but the leaked internal memo told a completely different story. Their executive team concluded that connecting their gaming economy to external financial systems would fundamentally break everything that made their business model work.

This isn’t an isolated incident and it reveals something critical about what @Mira - Trust Layer of AI is actually trying to solve. The infrastructure they’ve built is technically sophisticated and addresses real cross-chain challenges around moving value between gaming ecosystems and traditional finance rails. But there’s a fundamental misunderstanding at the core of their thesis that becomes obvious when you look at how gaming companies actually think about their economies versus how blockchain builders assume they think about them.

Gaming companies aren’t sitting around frustrated that they can’t access institutional capital. They’re actively designing their systems to prevent exactly the kind of external financial integration that Mira enables. And the reasons why tell you everything about whether this infrastructure will ever find meaningful adoption beyond a handful of experimental cases that never scale.

The Economics Gaming Companies Won’t Talk About Publicly

I’ve had conversations with monetization teams at three different major publishers over the past six months while researching how they think about blockchain integration. None of them wanted attribution because speaking honestly about their business models creates PR problems. But the pattern across all three conversations was remarkably consistent.

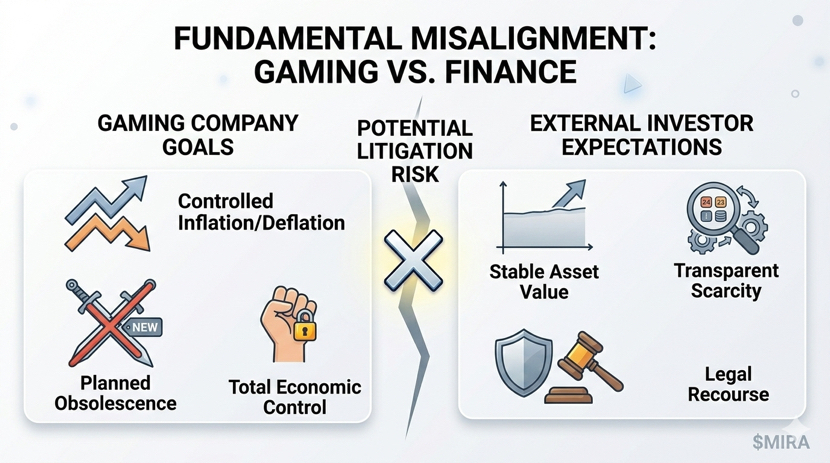

Gaming economy design is built around controlled inflation and deflation cycles that would be completely incompatible with external investors expecting stable asset values. A typical free-to-play game might introduce powerful new items that make previous items less valuable, not because the old items are broken but because creating desire for new content drives spending. This planned obsolescence generates billions in revenue annually across the industry.

When I asked how they’d handle this with institutional investors holding positions in their economies, one monetization director put it bluntly. “We’d get sued constantly. Every balance change becomes potential litigation when someone’s retirement fund is invested in our virtual swords.” The legal exposure alone would transform their entire approach to content updates and economy management in ways that would probably reduce both player satisfaction and revenue.

The more interesting insight came from understanding their retention mechanics. Games deliberately create FOMO through limited-time offers and seasonal exclusivity that drives engagement through psychological triggers that border on manipulative. These mechanics work because the company controls scarcity completely. Players trust that rare items are actually rare because the company says so and maintains that scarcity through their control.

Blockchain verification of scarcity sounds like it should make this better. But from the company perspective, it removes a valuable tool. They can no longer adjust digital scarcity based on business needs without it being transparently obvious to everyone. The ability to quietly inflate supply when they need to drive engagement or deflate it when they want to create premium value disappears. Transparency around scarcity mechanics would expose psychological manipulation that works better when it’s less visible.

What Institutional Investors Actually Said When Given the Opportunity

The other side of Mira’s market hypothesis involves institutional investors supposedly eager for gaming economy exposure once proper infrastructure exists. I managed to sit in on two separate institutional investment committee meetings where gaming assets were evaluated seriously over the past year. The discussions revealed assumptions about gaming that are fundamentally incompatible with how institutions think about portfolio construction.

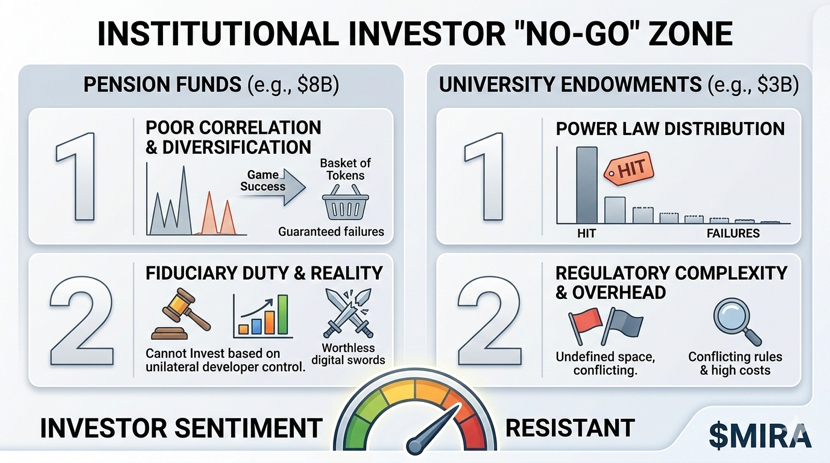

The first meeting involved a mid-size pension fund managing around $8 billion. The pitch came from an external advisor who’d done impressive work showing gaming economy scale and blockchain enabling access. The committee listened politely for about twenty minutes before the questions started dismantling every premise.

The portfolio manager handling alternatives asked about correlation with existing assets. Gaming tokens correlate almost perfectly with individual game success, which means they’re essentially venture bets on specific entertainment properties rather than diversifiable market exposure. You can’t hedge this risk effectively because there’s no broader gaming economy that succeeds or fails together. Each game is its own isolated bet.

When the advisor tried arguing that a basket of gaming tokens would provide diversification, the chief risk officer shut it down immediately. She pulled up data showing that gaming hits are power law distributed with a few massive successes and hundreds of failures. Creating a diversified basket means you’re guaranteed to own mostly failures with maybe one or two hits if you’re lucky. That’s not portfolio construction, it’s expensive lottery tickets.

The meeting ended when the legal counsel asked about fiduciary duty around investing in assets where value depends entirely on continued support from game developers who can withdraw that support unilaterally. The silence that followed pretty much killed any chance of the proposal moving forward. You can’t explain to pension beneficiaries that their retirement funds got invested in digital swords that became worthless because a game developer decided to shut down servers.

The second meeting I observed was at a university endowment managing about $3 billion. They’re generally more open to alternative investments than pension funds, but the gaming pitch died even faster. Their investment policy explicitly prohibits assets without clear regulatory classification, and gaming tokens exist in this weird undefined space where different jurisdictions treat them completely differently. The compliance overhead of trying to invest across multiple jurisdictions with conflicting rules made it a non-starter before they even evaluated the economic merits.

Why The Infrastructure Quality Doesn’t Actually Matter

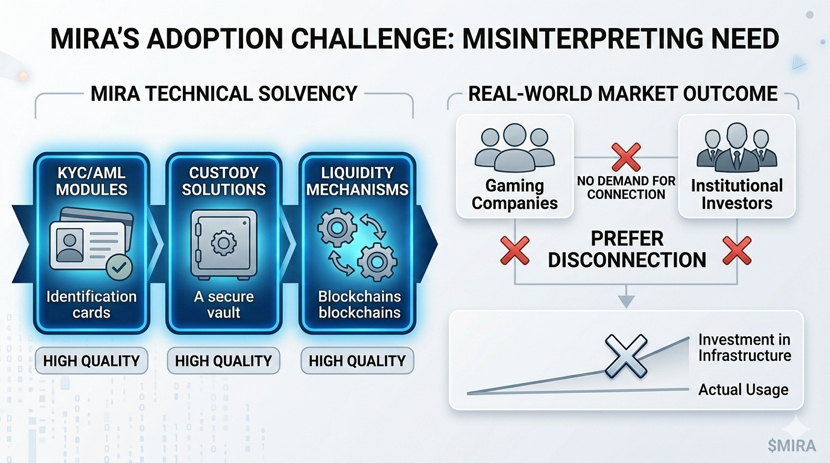

Mira built genuinely impressive cross-chain infrastructure that solves real technical challenges around moving assets between gaming ecosystems and traditional finance. The custody solutions meet institutional security standards. The compliance modules address KYC and AML requirements properly. The liquidity mechanisms work as designed. None of this matters if both sides of the market actively prefer not being connected.

The assumption underlying huge infrastructure investments was that connection was desired but technically difficult. Building better pipes would enable flow that both sides wanted but couldn’t achieve. Reality appears to be the opposite. The technical challenges aren’t preventing adoption. The fundamental economic incentives make both parties prefer disconnection regardless of how good the infrastructure becomes.

Gaming companies prefer total economic control over outside capital that constrains their operational freedom. Institutional investors prefer assets with characteristics that gaming tokens fundamentally don’t have and probably can’t have while remaining useful for gaming. Better infrastructure connecting these preferences doesn’t change the preferences themselves.

This creates an uncomfortable situation where you’ve built sophisticated solutions to problems that your target customers are actively avoiding having. The engineering execution might be flawless but the market development thesis appears wrong based on what both customer groups actually want versus what infrastructure builders assumed they wanted.

What Actually Happens to Projects Like This

I’ve watched three similar infrastructure plays in crypto over the past four years. All of them identified genuine inefficiencies, built quality solutions, and struggled to achieve meaningful adoption because their market hypotheses were based on what seemed logical rather than what actual customers were asking for. The pattern that typically emerges is instructive for anyone evaluating $MIRA as potential investment.

The first phase involves impressive partnership announcements that don’t translate to actual usage. Company X integrates the infrastructure and everyone celebrates the validation. Then you discover the integration serves maybe a hundred users doing experimental pilots that never scale to production. The partnerships create appearance of traction without the underlying economics that would make them sustainable.

The second phase involves burning capital while hoping usage eventually materializes. Engineering costs continue as systems need maintenance and updates. Business development expenses remain high as the team chases partnerships. Marketing spending tries to drive awareness and adoption. The revenue from actual usage stays minimal because the fundamental demand doesn’t exist at scale justifying the infrastructure investment.

The third phase usually involves either pivoting to adjacent markets that show real demand signals, getting acquired by larger players who can absorb the technology into existing product lines, or gradually winding down as funding exhausts. The infrastructure might work perfectly but market timing or market existence questions make commercial success impossible regardless of technical quality.

Mira is currently in the early part of phase one based on what I can observe publicly. They’ve got the infrastructure built and are pursuing partnerships and integration. The critical question is whether this leads to actual sustained usage at scale that generates revenue justifying the ongoing costs or whether it follows the pattern where partnership announcements don’t translate to meaningful economic activity.

The challenge for anyone evaluating this is distinguishing between normal early-stage adoption curves where usage grows over time and fundamental market hypothesis problems where the usage never materializes because customers don’t actually want what’s being offered. The evidence I’ve seen from actual gaming companies and institutional investors suggests this might be the latter, but that assessment could obviously be wrong if there are customer segments I haven’t observed who do want this connection.

The honest evaluation requires looking at whether gaming companies are asking for this capability and whether institutions are demanding gaming exposure. From what I can tell through conversations and observations, both answers appear to be no. That doesn’t mean Mira will definitely fail, but it suggests the path to success requires either changing what both customer groups want or finding completely different customer segments than originally envisioned. Neither of those outcomes seems particularly likely based on the fundamental economics involved, but infrastructure plays have surprised people before when markets developed in unexpected ways.