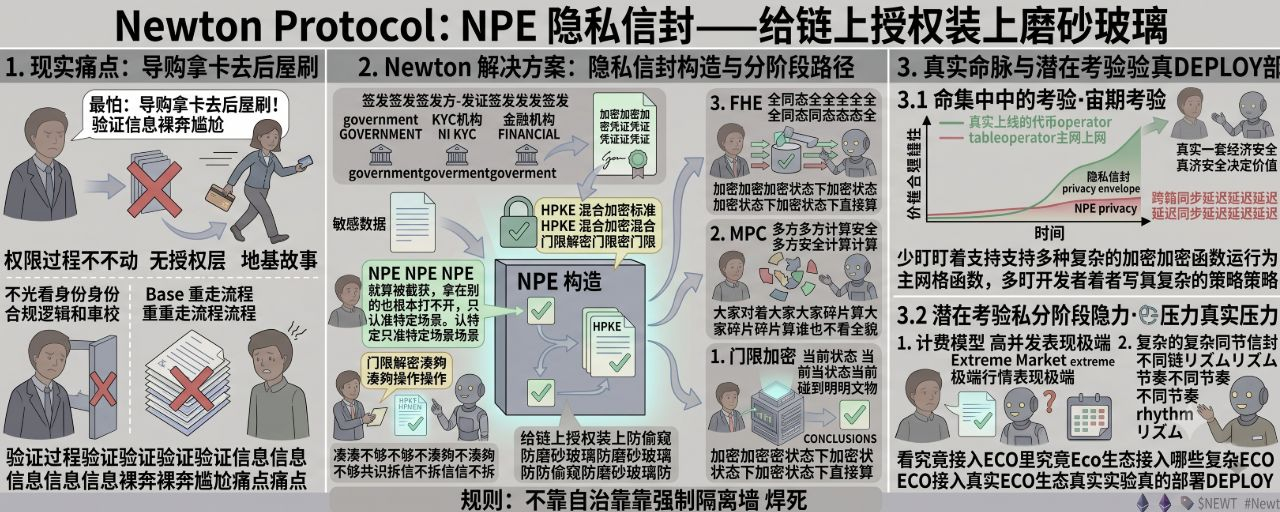

In the past, when buying valuable items at a mall counter, the one thing you feared most was the salesperson taking your credit card and going into a back room you can’t see to swipe it. Even though in the end they didn’t end up charging you extra, those few minutes left you feeling uneasy.

You don’t know whether he secretly wrote down your card number in there, or even made a copy of your ID. In this kind of verification process, the information is essentially exposed—actually one of the most awkward pain points in all financial authorizations.

After I read through the @NewtonProtocol white paper, about the design of the privacy layer NPE, I found that it took a lot of effort to solve this card-swiping “black box” problem. It created something called a Newton Privacy Envelope, and the logic is pretty interesting. It doesn’t simply encrypt the data and pass it along—it locks sensitive information inside an authorized envelope.

The strongest part of this envelope is that it tightly binds the data, the specific strategy logic, and your own authorization signature together. This means that even if this envelope is intercepted—or obtained on some other chain—it still cannot be opened, because it only recognizes that specific evaluation scenario.

Locking down the data context is far smarter than just using encryption.

I appreciate this kind of stubborn insistence on data sovereignty. It doesn’t expose the details directly to the operator. Instead, it gives users a locked parcel. In this NPE construction, it uses HPKE as the latest hybrid encryption standard, and on top of that it layers threshold decryption. In other words, it isn’t that any operator can just open it—the operators need to reach consensus in a sufficient number before, in their secure enclave, the envelope can be opened.

This design reduces the risk of that kind of middleman taking your card and swiping behind the back to the absolute minimum using mathematics and collaborative mechanisms. You don’t have to trust any one operator’s character—you trust the missing fragments and the locked, unopened envelope.

At a deeper level, it’s about planning the privacy path. The whitepaper is very honest: it lays out a three-step approach. What we see is step one—threshold encryption. It admits that in this step, when the operator is actually doing the work, they still come into contact with plaintext at that moment, even if it happens inside a secure environment, it’s still contact. Then it draws the second step’s MPC and the third step’s FHE. MPC has everyone compute on fragments without anyone seeing the full picture; FHE is even more of a magic trick—it computes directly on encrypted data.

I really like this honest, no-fluff attitude toward the current state of things. It doesn’t pull FHE from the lab and market it as a ready-made selling point. Instead, it tells you what we’ve achieved right now and how we plan to move forward next. That kind of pragmatism is pretty rare in today’s circles.

But the boundaries also need to be made clear. No matter how perfect the NPE-style envelope model is, it only protects against snooping in the transmission and storage processes—it protects against the data being repurposed for other uses.

But it can’t stop the issuer from the source. If the institution that issues your KYC credentials is itself a makeshift operation, or if the envelope it puts in front of you contains fake data, then no matter how refined Newton’s envelope is, the authorization result at the end will still be wrong. This is my inference based on this issuer-holding model—not that fake credentials have been issued right now. Also, complex encryption envelopes and threshold decryption will definitely have an impact on authorization speed.

The whitepaper doesn’t provide concrete millisecond-level figures, but in highly concurrent financial scenarios, whether institutions can accept the time cost paid for privacy depends on the real feedback that comes out when the mainnet Beta runs.

So how should we look at this? Newton’s privacy envelope aims to add a layer of frosted, privacy-preserving glass to on-chain authorization—so the verification result can come out, but the details don’t leak. This move is quite deep, and it really hits the bottom-line requirements that both institutions and individuals have for data security.

But its quality doesn’t lie in using fancier encryption algorithms—it lies in whether it can preserve privacy without making the authorization process as slow as a stubborn old ox pulling a cart. Don’t focus on the grand prospects it talks about for MPC and FHE; focus more on its current first-stage privacy envelope.

In real transactions, what is the processing latency—exactly what that number is is the key to whether it can move from the lab to the counter.