1) Executive summary

Avalanche $AVAX is a Layer 1 blockchain ecosystem built around fast settlement, EVM-compatible smart contracts, and customizable Avalanche L1s. The network's Primary Network includes the C-Chain, where most EVM activity occurs, and its broader architecture lets applications and institutions launch dedicated blockchains with configurable validators, execution environments, gas tokens, and compliance controls.

Avalanche is associated with Ava Labs, a blockchain technology company founded in 2018 by Emin Gun Sirer, Kevin Sekniqi, and Maofan Yin. Emin Gun Sirer serves as CEO, and Ava Labs lists offices in New York City and Miami. Avalanche and its ecosystem have been supported by a mix of venture financing, AVAX token sales, and Foundation-led ecosystem funding, giving the project institutional backing while keeping the public report focused on the network's development, adoption, and operating metrics.

Q1 2026 was a mixed quarter for Avalanche. Ecosystem TVL, stablecoin supply, trading volume, active loans, fees, and FDV declined sequentially, while transaction count, transactions per second, and monthly active users increased. The strategic narrative was stronger than the market backdrop: Avalanche continued to position itself as infrastructure for purpose-built L1s and institutional tokenization, with Q1 developments spanning tokenized assets, gaming L1 infrastructure, and usage-based builder incentives.

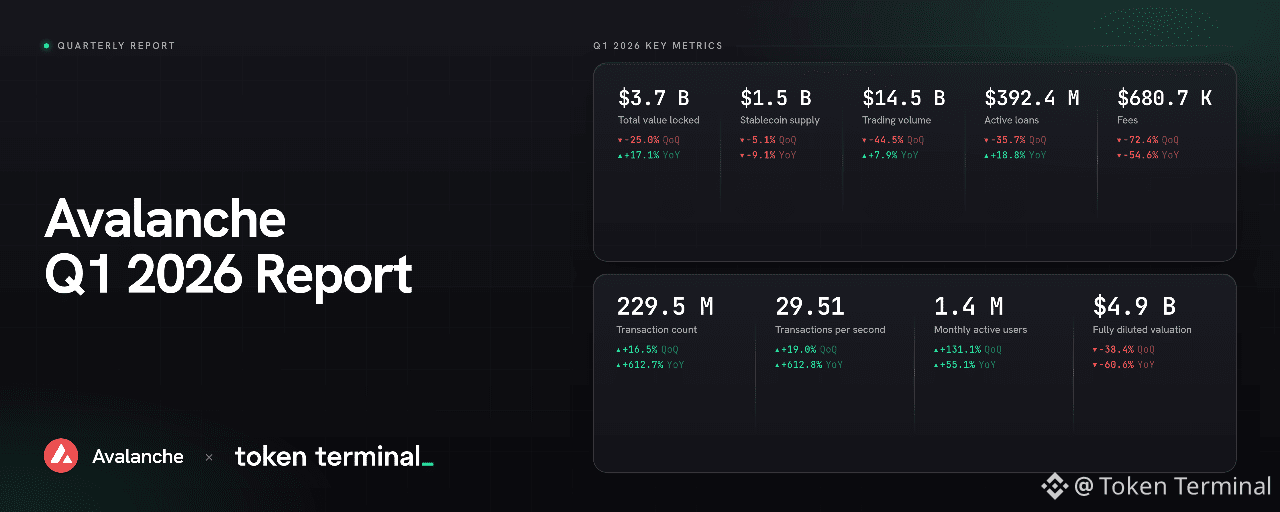

🔑 Key metrics (Q1 2026)

Ecosystem total value locked: $3.7 B (-25.0% QoQ, +17.1% YoY)

Ecosystem stablecoin supply: $1.5 B (-5.1% QoQ, -9.1% YoY)

Ecosystem trading volume: $14.5 B (-44.5% QoQ, +7.9% YoY)

Ecosystem active loans: $392.4 M (-35.7% QoQ, +18.8% YoY)

Fees: $680.7 K (-72.4% QoQ, -54.6% YoY)

Transaction count: 229.5 M (+16.5% QoQ, +612.7% YoY)

Transactions per second: 29.51 (+19.0% QoQ, +612.8% YoY)

Monthly active users: 1.4 M (+131.1% QoQ, +55.1% YoY)

Fully diluted valuation: $4.9 B (-38.4% QoQ, -60.6% YoY)

Metrics include only Avalanche's C-Chain and exclude activity on Avalanche Subnets.

👥 Ava Labs team commentary

"Q1 2026 was the quarter where Avalanche's institutional thesis moved from pipeline to production at scale. Network activity set new records across the board, with total network transactions hitting an all-time high, C-Chain transactions reaching their sixth consecutive quarter of growth, and $164.0 B in stablecoin transfer volume processed in the quarter alone. The story behind those numbers is technology built for business: blockchain rails for payments, lending, savings, and investing embedded behind the scenes into the fintechs, neobanks, brokerages, and asset managers that already have distribution, giving them new revenue streams while Avalanche runs quietly as the settlement layer.

The quarter's key developments reflect that thesis playing out in practice. In payments, Axiym settled $467.0 M on Avalanche through infrastructure running across 140 countries with stablecoins handling settlement in the background for major MSBs. In institutional finance, Progmat announced a $2.0 B migration of tokenized securities to an Avalanche L1, VanEck and Grayscale launched the first US-listed AVAX ETFs, and a growing private credit ecosystem including Valinor, Apollo, Janus Henderson, and OpenTrade pushed tokenized assets on-chain past $1.3 B, with OpenTrade surpassing $110.0 M powering savings products for retail users across Latin America and Asia with no blockchain interaction required from the end user. In consumer, FIFA Collect opened a new primitive for sports ticketing through right-to-buy ticket tokens, and Uptop brought on-chain fan loyalty rewards to the Cleveland Cavaliers, Detroit Pistons, and LSU Athletics, reaching 3,700 unique fan wallets in Q1, with its acquisition by Rain positioning stablecoin rails to come to those venues through the same infrastructure. Heading into Q2, Asia partnerships are moving into production, the private credit pipeline continues to scale, and the share of on-chain capital anchored by real cash flows rather than sentiment keeps growing."

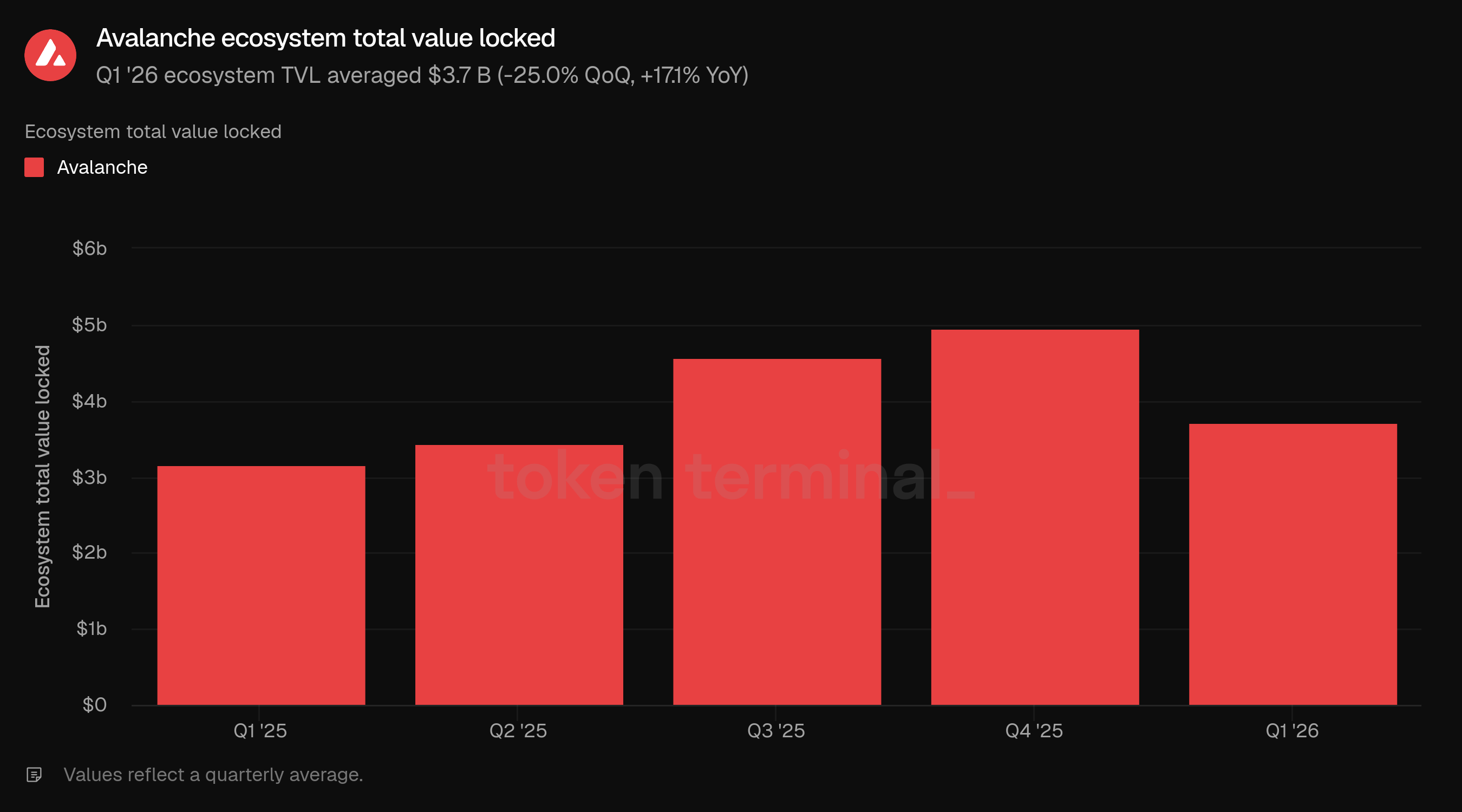

2) Ecosystem total value locked

Ecosystem total value locked (TVL) measures the total USD value of user deposits into applications on Avalanche. Q1 ecosystem TVL averaged $3.7 B, down 25.0% from $5.0 B in Q4 but up 17.1% from $3.2 B in Q1 2025.

The sequential decline followed two quarters of expansion, with TVL rising from $3.4 B in Q2 to $4.6 B in Q3 and $5.0 B in Q4 before retracing in Q1. Despite the Q1 contraction, average ecosystem TVL remained above every quarter in the first half of 2025, indicating that the ecosystem retained a larger capital base than it had a year earlier.

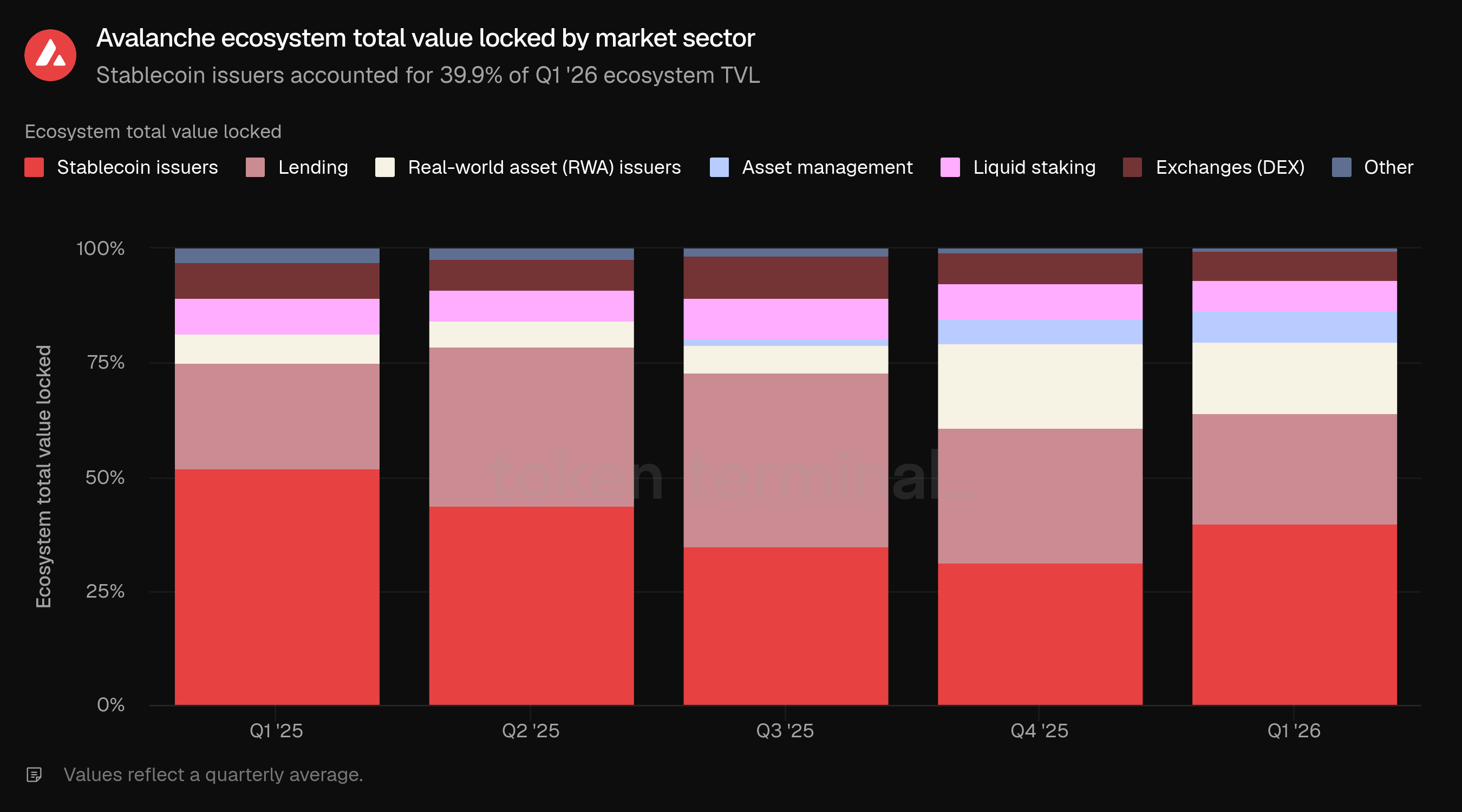

Stablecoin issuers accounted for 39.9% of Q1 ecosystem TVL, up from 31.1% in Q4 but below 52.1% in Q1 2025. Lending accounted for 24.3%, down from 29.8% in Q4. Real-world asset issuers accounted for 15.4%, down from 18.6% in Q4 but well above their 6.3% share a year earlier. Asset management increased to 6.9%, while liquid staking, exchanges, and other sectors accounted for 6.9%, 6.2%, and 0.4%, respectively.

The market-sector mix supports Avalanche's broader institutional narrative. RWA issuers and asset management together accounted for 22.3% of Q1 ecosystem TVL, compared with 6.3% in Q1 2025. That shift aligns with continued RWA-focused deployment activity on Avalanche.

👥 Ava Labs team commentary

"The sequential decline in Q1 TVL was driven by external market conditions rather than anything specific to Avalanche. As risk appetite softened broadly across crypto, leveraged positioning pulled back across DeFi, compressing lending TVL on Avalanche in line with what played out across every major chain globally. AVAX's 29.0% price decline over the quarter added a mechanical headwind, reducing the dollar value of AVAX-denominated positions; BENQI Liquid Staking's sequential decline was driven almost entirely by price rather than actual withdrawals, with staked supply roughly flat in token terms. Year over year the picture looks different, with the ecosystem TVL base larger and supported by institutional products that barely existed twelve months ago, including Avant Protocol's avUSD scaling from $13.0 M to $121.0 M and BlackRock's BUIDL growing from $53.0 M to $92.0 M.

The growing share of stablecoins and real-world assets in the mix reflects a meaningful shift in the kind of capital Avalanche is attracting, and the right frame for interpreting it is not just what is on-chain today but what is coming behind it. Avalanche ranks seventh among all chains by non-stablecoin distributed RWA value as of Q1 2026, and that share should grow meaningfully as fintechs, brokerages, and consumer platforms continue embedding on-chain products into their existing applications, bringing tokenized funds and yield-bearing instruments to users who will never interact directly with a blockchain. This is already playing out on Avalanche, with partners like OpenTrade providing retail users across Latin America and Asia access to tokenized US Treasury exposure through consumer fintech interfaces, $117.0 M in RWAs on-chain as proof. As lending protocol partners bring dedicated RWA markets to Avalanche in the coming quarters, those same institutional assets will begin functioning as productive, composable collateral across the ecosystem, and the TVL that comes with fintech-scale distribution is structurally more durable than anything sentiment-driven positioning produces."

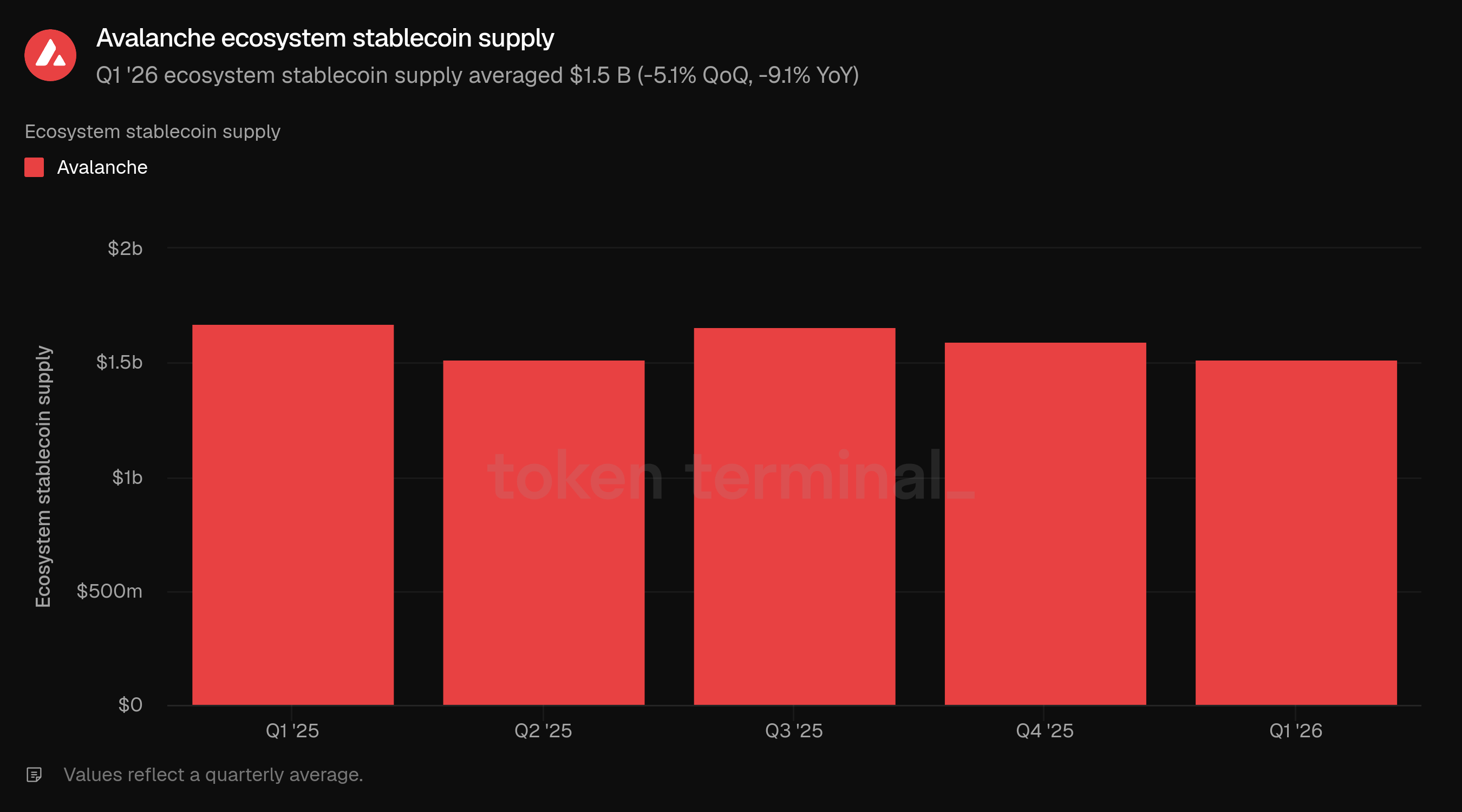

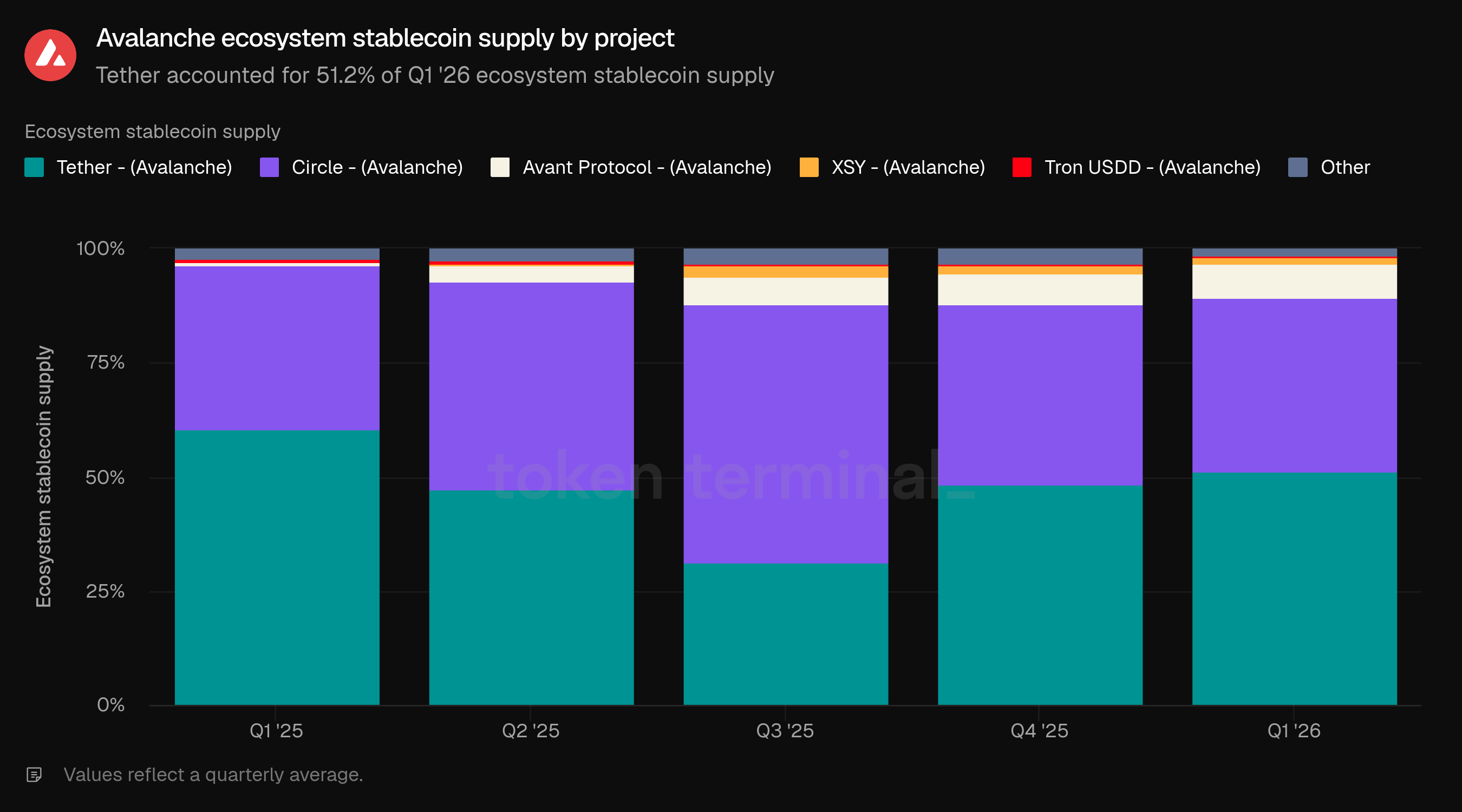

3) Ecosystem stablecoin supply

Ecosystem stablecoin supply measures the total USD value of outstanding stablecoins issued on Avalanche. Q1 ecosystem stablecoin supply averaged $1.5 B, down 5.1% from $1.6 B in Q4 and down 9.1% from $1.7 B in Q1 2025.

Stablecoin supply was relatively more resilient than ecosystem TVL and active loans during Q1. The metric was flat versus Q2 2025, below the Q3 and Q4 levels, and still below the year-ago quarter. This makes stablecoins a stabilizing but not yet accelerating part of the Avalanche ecosystem in the current dashboard data.

Tether accounted for 51.2% of Q1 ecosystem stablecoin supply, up from 48.3% in Q4. Circle accounted for 38.0%, down from 39.5%. Avant Protocol increased to 7.4%, up from 6.5% in Q4 and 0.6% in Q1 2025. XSY and Tron USDD accounted for 1.4% and 0.7%, respectively, while Other accounted for 1.4%.

The stablecoin mix became less Tether-dominated over the year, even though Tether regained share sequentially in Q1. The most notable year-over-year change was Avant Protocol's rise from 0.6% to 7.4% of supply. FUSD's Q1 launch adds another RWA-backed stablecoin angle to the ecosystem, though Q1's stablecoin supply remained concentrated in Tether and Circle.

👥 Ava Labs team commentary

"Tether and Circle's dominance on Avalanche reflects their position across crypto broadly, and the more interesting story is what is happening beneath them. Adjusted non-USD stablecoin transfer volume nearly doubled from Q4 2025 to Q1 2026, reaching over $1.0 B in the quarter, with EURC growing from $76.0 M in adjusted volume in September 2025 to $308.0 M by March and MXNB reaching $46.4 M as Nonco's FX settlement corridor scaled, average swap size growing from $40,500 in January to $92,200 by March as institutional flow picked up. More than 60 distinct stablecoins are now live on Avalanche, with Singapore dollar, Japanese yen, Turkish lira, and Brazilian real each reflecting real user demand in their respective markets. The stablecoin mix is diversifying organically, driven by use cases rather than design, and that is the healthier outcome.

The user segments driving stablecoin activity on Avalanche are broadening in ways that matter. The base of DEX trading, lending markets, and on-chain transactions remains, but what is being added on top is different in character. Avant Protocol's avUSD has scaled past $100.0 M as a DeFi-native yield-bearing primitive, BlackRock's BUIDL and OpenTrade's vaults serve the institutional and fintech-distributed end of the market, and Sky's native deployment of USDS and sUSDS via Skylink brings one of DeFi's most established stablecoin ecosystems on-chain through a burn-and-mint framework requiring no bridge liquidity. Wyoming's FRNT as the first US state-issued stablecoin and Fosun's RWA-backed stablecoin with Avalanche as its primary liquidity hub add further depth, and Axiym's payment infrastructure is settling cross-border MSB flows at scale through the same rails. The direction is toward a stablecoin ecosystem on Avalanche that serves institutional settlement, DeFi composability, and fintech-distributed retail simultaneously, with liquidity building around each use case on its own terms."

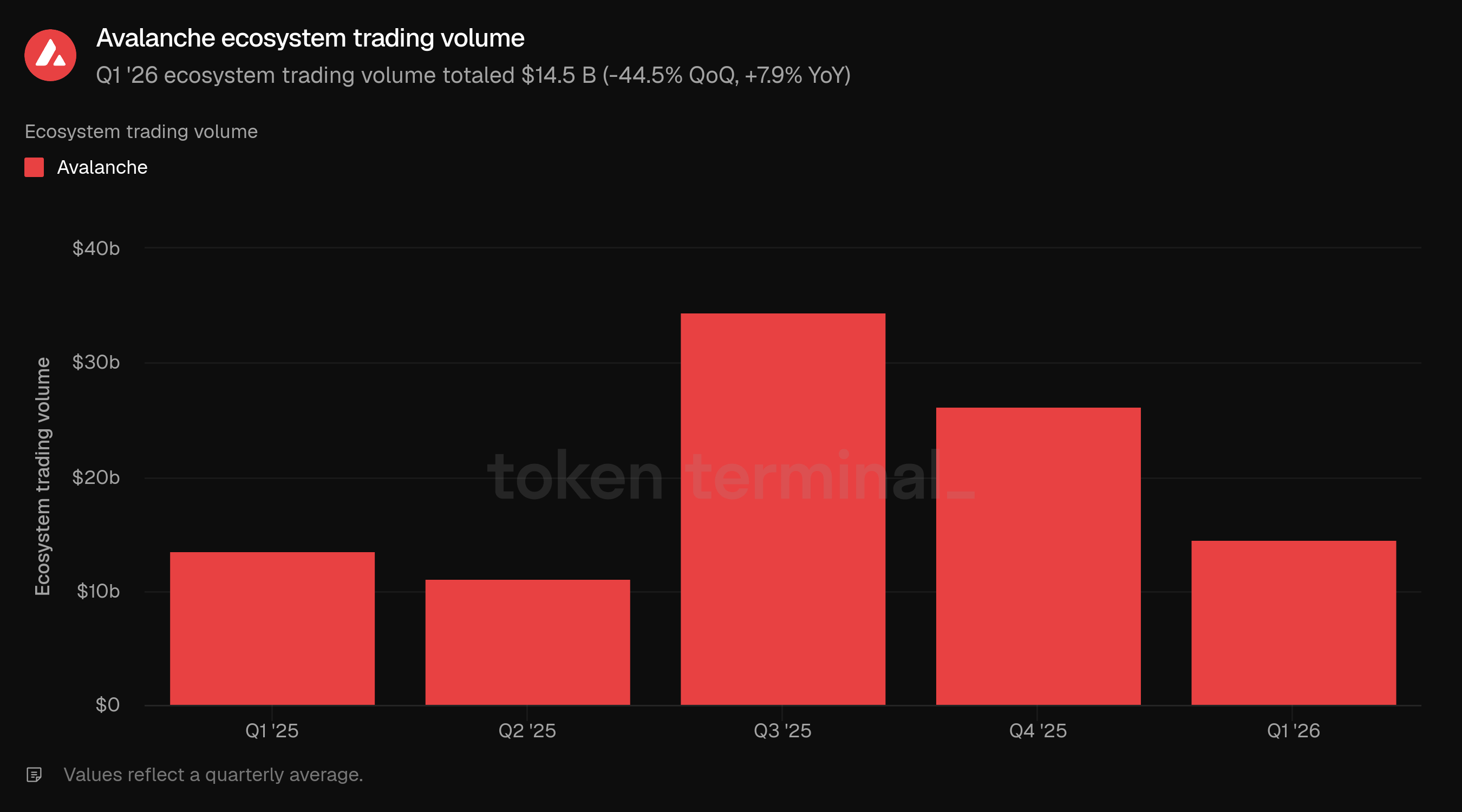

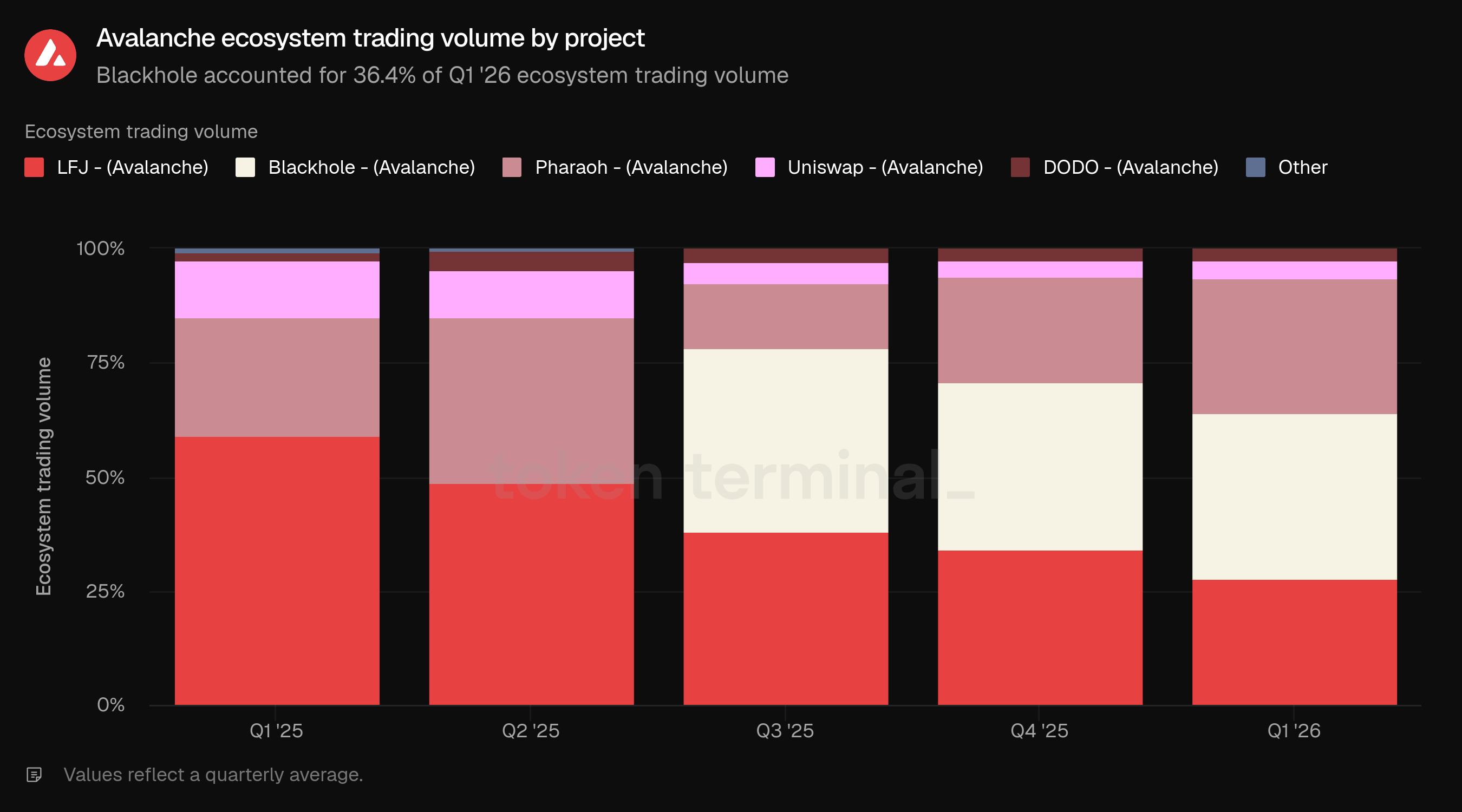

4) Ecosystem trading volume

Ecosystem trading volume measures the total USD value of DEX trades executed by applications on Avalanche. Q1 ecosystem trading volume totaled $14.5 B, down 44.5% from $26.2 B in Q4 but up 7.9% from $13.5 B in Q1 2025.

Trading volume fell sharply from the Q3 and Q4 2025 levels, when Avalanche DEX activity totaled $34.5 B and $26.2 B, respectively. Even after the sequential contraction, Q1 trading volume remained above the year-ago period and above Q2 2025, indicating that DEX throughput was lower than the late-2025 peak but not back to early-2025 levels.

Blackhole accounted for 36.4% of Q1 ecosystem trading volume, roughly flat from 36.5% in Q4. Pharaoh accounted for 29.6%, up from 23.0%, while LFJ accounted for 27.7%, down from 34.3%. Uniswap and DODO accounted for 4.0% and 2.3%, respectively, while Other accounted for 0.1%.

The trading-volume mix remained concentrated among three venues: Blackhole, Pharaoh, and LFJ together accounted for 93.7% of Q1 volume. The year-over-year change was more pronounced: LFJ accounted for 59.1% of trading volume in Q1 2025, while Blackhole was not present in the Q1 2025 tooltip breakdown and became the largest contributor by Q1 2026.

👥 Ava Labs team commentary

"Q1 was a quieter quarter across crypto broadly, and Avalanche DEX volume reflected that. The broader DEX market was down roughly 33.0% quarter over quarter in the same period, so Avalanche at -44.5% underperformed somewhat, though Q4 was an unusually high baseline. Blackhole launched in July 2025 and Pharaoh V3 in September, both pulling in a wave of exploratory volume that normalized once the new venue launches settled and volatility came down. Year over year, volume was up 7.9% versus Q1 2025, with a more competitive DEX landscape than existed then.

The 93.7% volume share looks like concentration until you consider how recently two of those three venues showed up. A couple years ago LFJ was carrying the vast majority of Avalanche DEX volume by itself. Now that share is split across three venues genuinely competing, with Blackhole and Pharaoh not existing in their current form 18 months ago. Pharaoh grew from $281.0 M in Q1 2024 to $4.3 B in Q1 2026 built natively on Avalanche with a ve(3,3) model, declining only 16.6% quarter over quarter against a broader ecosystem down 44.5%. Blackhole launched in July 2025 and by Q1 2026 was the highest volume venue on the chain at $5.3 B."

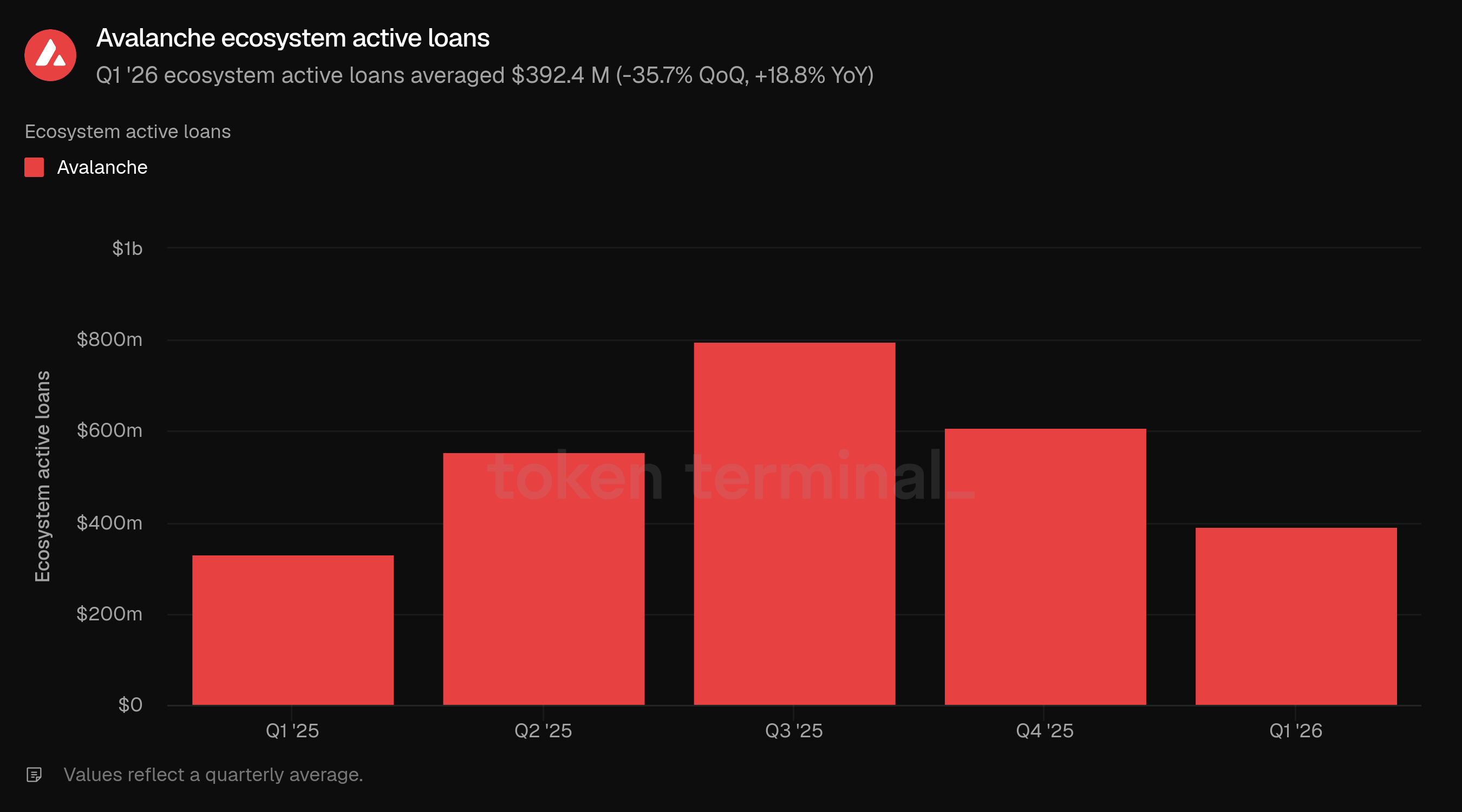

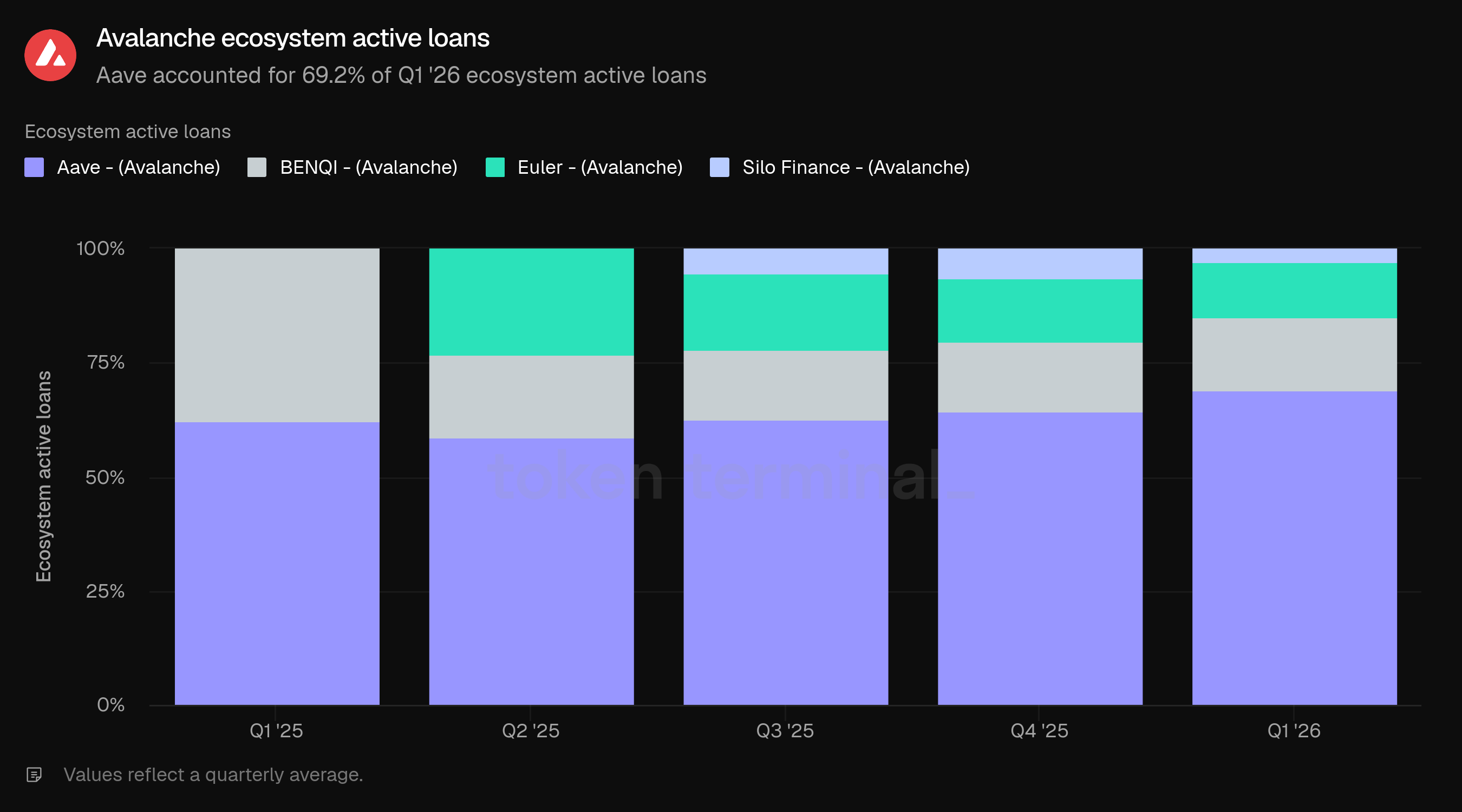

5) Ecosystem active loans

Ecosystem active loans measures the total USD value of outstanding loans issued by lending applications on Avalanche. Q1 ecosystem active loans averaged $392.4 M, down 35.7% from $609.9 M in Q4 but up 18.8% from $330.2 M in Q1 2025.

Active loans declined more sharply than ecosystem TVL, indicating that borrowing demand weakened during Q1 relative to deposited capital. The metric remained above the year-ago period, but the sequential decline brought active loans below Q2, Q3, and Q4 2025 levels.

Aave accounted for 69.2% of Q1 ecosystem active loans, up from 64.3% in Q4 and 62.4% in Q1 2025. BENQI accounted for 15.9%, Euler accounted for 12.2%, and Silo Finance accounted for 2.8%. Aave gained share sequentially as Euler and Silo Finance lost share, while BENQI was broadly stable.

The active-loan mix shows that Avalanche lending remained concentrated in Aave during the quarter. This concentration can be constructive for liquidity depth, but it also means ecosystem borrowing trends are highly sensitive to Aave market conditions, risk parameters, and borrower demand.

👥 Ava Labs team commentary

"The decline in active loans in Q1 reflects the same dynamic that compressed DeFi TVL broadly: as crypto markets softened and speculative positioning pulled back, demand for leveraged exposure fell across every major chain simultaneously. The year-over-year growth of 18.8% is the more meaningful number, reflecting a lending base that is larger and more diversified than it was twelve months ago even after the sequential contraction. Aave's 69.2% share reflects a pattern that plays out across DeFi broadly: in the absence of significant emissions-driven incentives elsewhere, users gravitate toward the most battle-tested protocols with the deepest liquidity, and that is a market outcome rather than a structural concern specific to Avalanche.

Lending markets on C-Chain fit into Avalanche's institutional strategy in a direct way: as tokenized real-world assets become a larger share of what sits on-chain, the lending layer is what makes those assets productive rather than passive. An institution holding a tokenized treasury fund, CLO tranche, or private credit position can borrow stablecoins against it while the underlying continues earning, which changes the economics of being on-chain entirely. That is the direction lending on Avalanche is heading, and the private credit ecosystem already building here reflects the same logic: partners including OatFi, Valinor, Fence, BlackOpal, Bright Funding, and Droplinked are financing B2B receivables, credit-card receivable flows, and other real-world credit instruments on-chain, representing a category of short-duration credit that stablecoin-native settlement makes financeable for the first time."

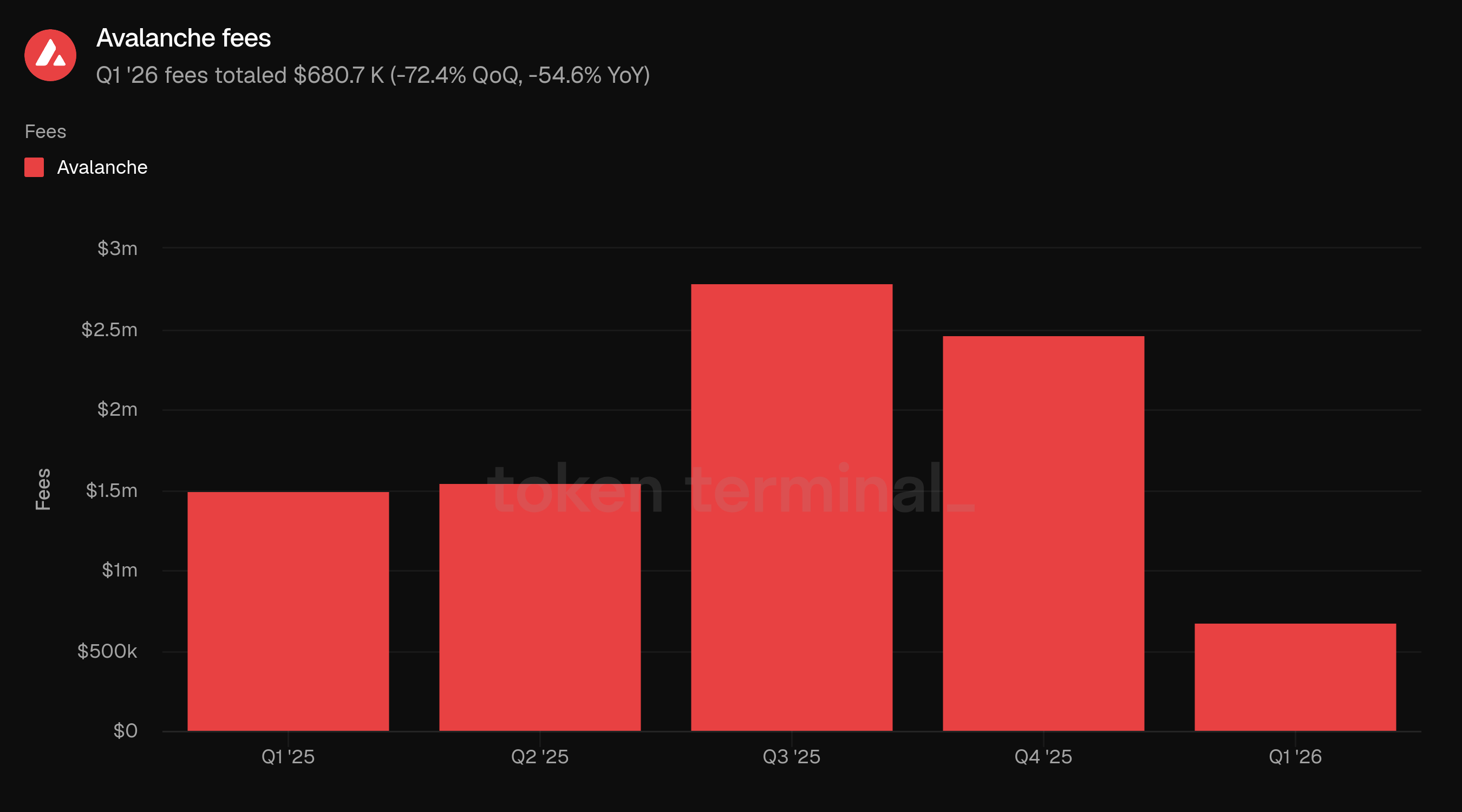

6) Fees

Fees measure the total USD value paid by users to transact on Avalanche. Q1 fees totaled $680.7 K, down 72.4% from $2.5 M in Q4 and down 54.6% from $1.5 M in Q1 2025.

The fee decline was the sharpest contraction among the core operating metrics in the dashboard. It also diverged from transaction count and transactions per second, both of which increased sequentially and year-over-year. This indicates that higher transaction throughput did not translate into higher fee generation during Q1, likely reflecting lower fee intensity per transaction.

This divergence matters for Avalanche's blockchain-business profile. Q1 showed that the network can process meaningfully more activity while users pay materially less in aggregate fees. That can be positive for user experience and application growth, but it weakens near-term fee capture unless activity density or fee-generating use cases increase.

👥 Ava Labs team commentary

"The fee decline is intentional. Token Terminal ranked Avalanche the lowest-fee major chain in March, with median C-Chain transaction fees down 99.6% year over year to $0.0000137. The goal is for individual user fees to go down while total fee revenue grows, and the path there is expanding block space supply and continuously fine-tuning the fee mechanism. The Octane upgrade gave validators the ability to dynamically signal network capacity without requiring hard forks, and the results showed up quickly in the numbers.

Cheaper fees did surface one issue worth noting. With prices near zero during quiet periods, certain protocols found it profitable to run low-value activity on-chain at scale, consuming network resources without contributing meaningfully to the ecosystem. The team is addressing this through a proposed upgrade that would give validators the ability to collectively set a price floor during low-activity windows, without affecting costs for normal users. The broader philosophy holds: fees should be low enough to unlock real-world use cases, resilient against abuse, and structured to grow aggregate network revenue as activity scales."

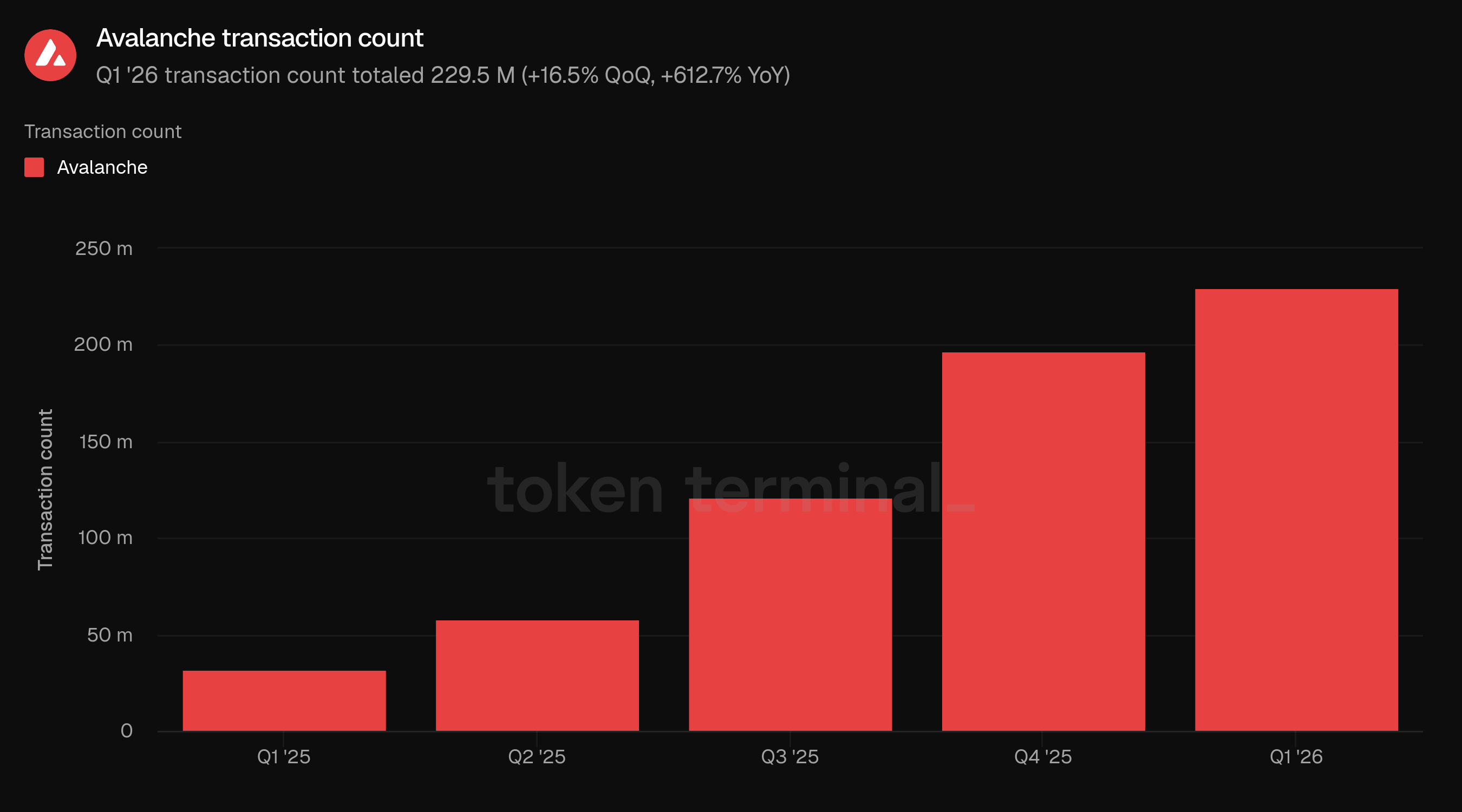

7) Transaction count

Transaction count measures the total number of confirmed transactions on Avalanche. Q1 transaction count totaled 229.5 M, up 16.5% from 197.0 M in Q4 and up 612.7% from 32.2 M in Q1 2025.

Transaction count increased for the fourth consecutive quarter in the dashboard period. The year-over-year comparison is especially large, with Q1 activity more than seven times the year-ago level. This makes transaction throughput the strongest growth metric in the report.

The increase coincided with Avalanche's broader push toward measurable usage. Retro9000 C-Chain Round 1, which went live in March, rewards projects based on AVAX burned by real C-Chain activity. Separately, Avalanche Builder Hub's spam-prevention work highlights the need to interpret transaction growth alongside network-quality controls, because low-fee environments can create both legitimate usage growth and operational spam-management requirements.

👥 Ava Labs team commentary

"The 229.5 M transactions in Q1 came from a broad set of sources. Native USDC was present across a meaningful share of activity, moving through DEX swaps, lending markets, payments, and transfers, a reflection of how deeply it has embedded itself as the primary asset across C-Chain. MyPrize generated 44.7 M transactions from 1.2 M monthly active users, accounting for nearly 20.0% of total throughput, while the remainder came from 1.3 M unique contracts spanning Blackhole, Pharaoh, LFJ, cross-chain bridging, and MapleStory Universe's NXPC token economy with nearly 40,000 in-game burn transactions. Bot share was 0.1% and median fees stayed at fractions of a cent.

Retro9000's C-Chain Round 1 ties rewards to AVAX burned through actual usage, and the early rankings show it working as intended. Blackhole, Pharaoh, and LFJ came in first, second, and third, the three dominant DEXes on the chain. Beyond them, AvaxPixel crossed 400,000 transactions from a growing global community, PumpSpace, The Arena, and Festify each drove real activity, and the program is giving emerging builders a path to visibility based on usage rather than fundraising."

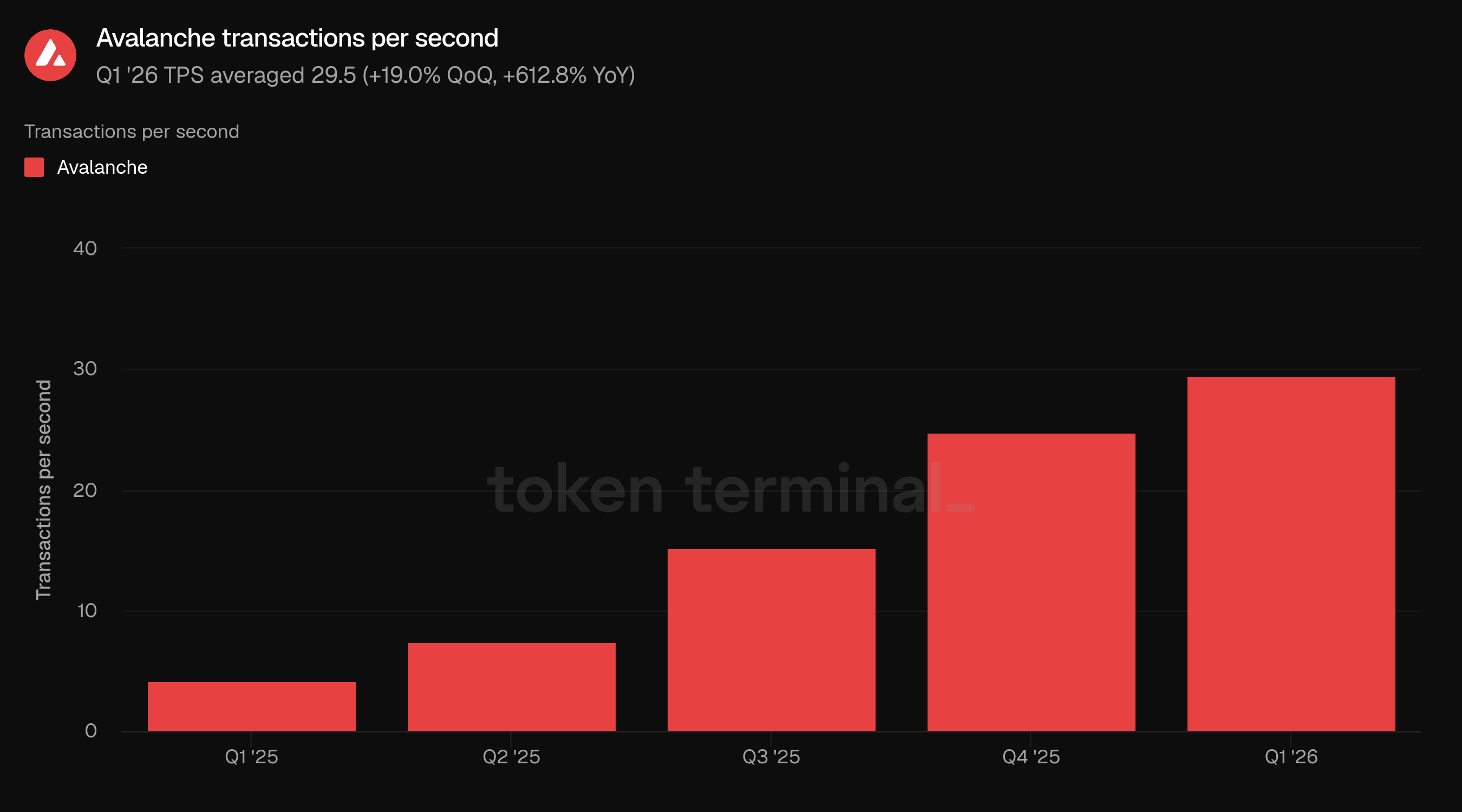

8) Transactions per second

Transactions per second (TPS) measures Avalanche's average transaction throughput during the period. Q1 TPS averaged 29.5, up 19.0% from 24.8 in Q4 and up 612.8% from 4.1 in Q1 2025.

TPS followed the same directional pattern as transaction count, increasing sequentially and sharply year-over-year. This confirms that the transaction-count increase was not only a quarterly total effect, but also reflected a higher average rate of network activity.

The TPS increase reinforces Avalanche's positioning around scalable execution. However, the simultaneous fee decline means Q1 throughput growth should be interpreted as a network-usage and capacity story rather than a fee-growth story.

👥 Ava Labs team commentary

"TPS growth in Q1 was driven by a combination of infrastructure improvements and application-level activity. The Granite upgrade, which activated in November 2025, introduced dynamic minimum block times through ACP-226, allowing validators to push toward sub-second confirmations and enabling more transactions to settle in a given period. On the application side, MyPrize's 44.7 M transactions, sustained DEX activity across Blackhole and Pharaoh, and growing cross-chain activity all contributed to the higher baseline throughput across the quarter.

TPS on its own tells you how much the network is processing but not what it is processing. The metrics worth watching alongside it are gas utilization relative to the 4.0 M gas per second target, which shows how much of the available capacity is being used, stablecoin transfer volume as a proxy for real economic activity moving through the chain, and unique contracts called as a signal of application diversity."

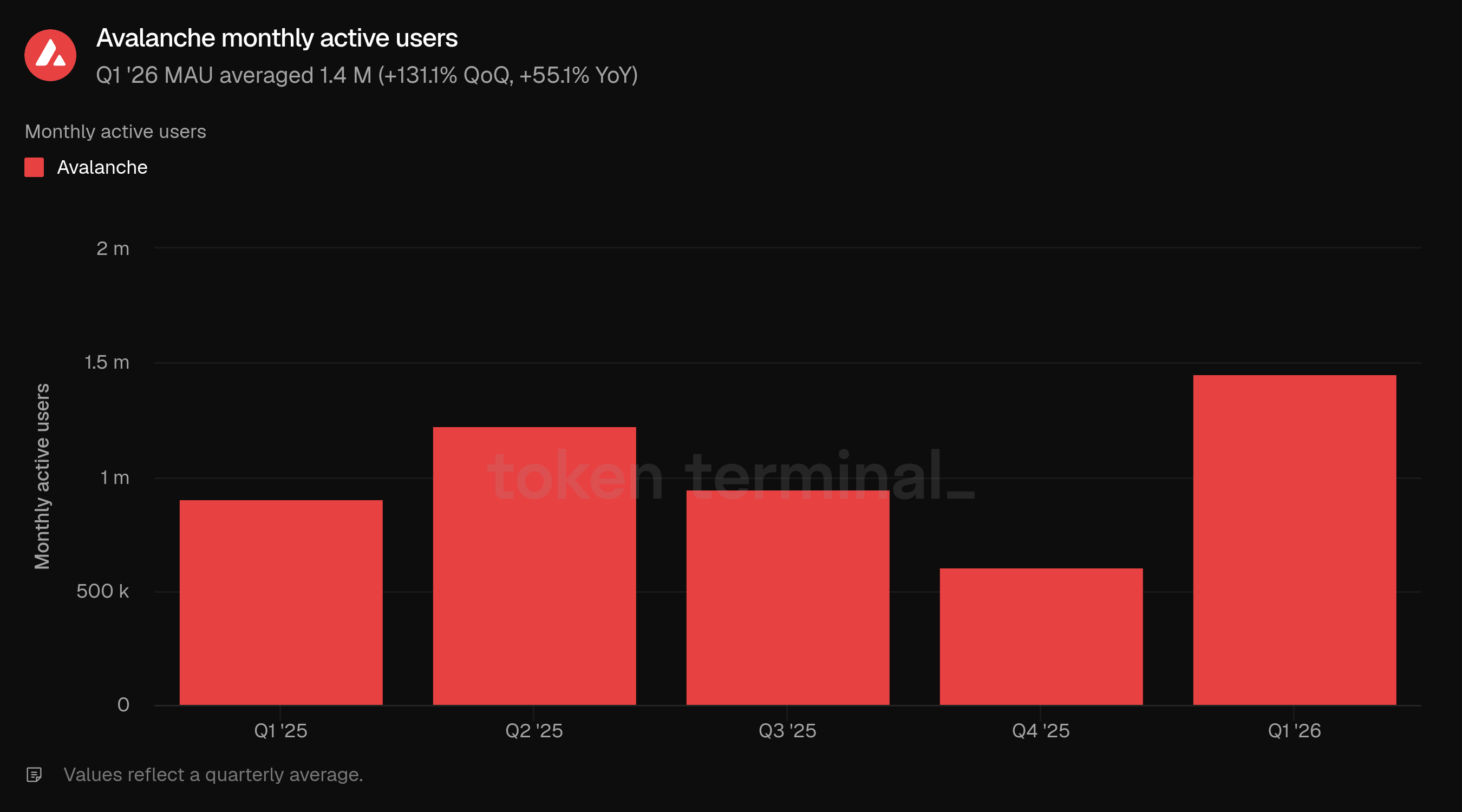

9) Monthly active users

Monthly active users (MAU) measures the number of unique addresses that sent at least one transaction on Avalanche within a rolling 30-day window. Q1 MAU averaged 1.4 M, up 131.1% from 605.9 K in Q4 and up 55.1% from 902.6 K in Q1 2025.

MAU was the strongest user-side metric in Q1. The increase reversed declines from Q2 through Q4 2025 and brought active users above every prior quarter in the dashboard period. The divergence between rising MAU and declining fees suggests that the quarter's user growth was broad but relatively low in fee intensity.

Q1 product and ecosystem activity gives several possible sources of user growth, including builder incentives, C-Chain activity programs, gaming-related launches, and stablecoin/RWA distribution. The metric should still be interpreted carefully because wallet-count growth does not necessarily map one-to-one to economic activity, particularly during incentive-driven periods.

👥 Ava Labs team commentary

"MAU more than doubled QoQ to 1.4 M, with MyPrize as the standout contributor, generating 1.2 M monthly active users across all three months of Q1 alongside its 44.7 M transactions. Gaming and consumer applications on both C-Chain and dedicated L1s added further depth, while the continued growth of DeFi and payment activity brought in users through entirely different channels.

Distinguishing durable user acquisition from short-term participation comes down to behavior over time. The industry learned that token emissions and yield incentives attract capital and users that leave the moment a better opportunity appears elsewhere. What matters is where the user is being onboarded, through which distribution partner, and whether they continue to engage after the initial interaction. Returning addresses, sustained transaction activity, and asset retention are the signals that separate structural adoption from a spike, and around 90.0% of active addresses on Avalanche in Q1 were returning addresses.

As for which segments are most important going forward, the lines between them are blurring. We have been building institutional infrastructure since before RWAs were a narrative, and that focus on tokenization, private credit, stablecoins, and payments continues. But Avalanche is a general purpose chain and gaming, consumer applications, and app-specific L1s remain a core part of the strategy. DeFi, institutional finance, payments, and fintech distribution are all converging into the same on-chain stack, and the through line across all of it is the same: providing the technology for businesses to do better business."

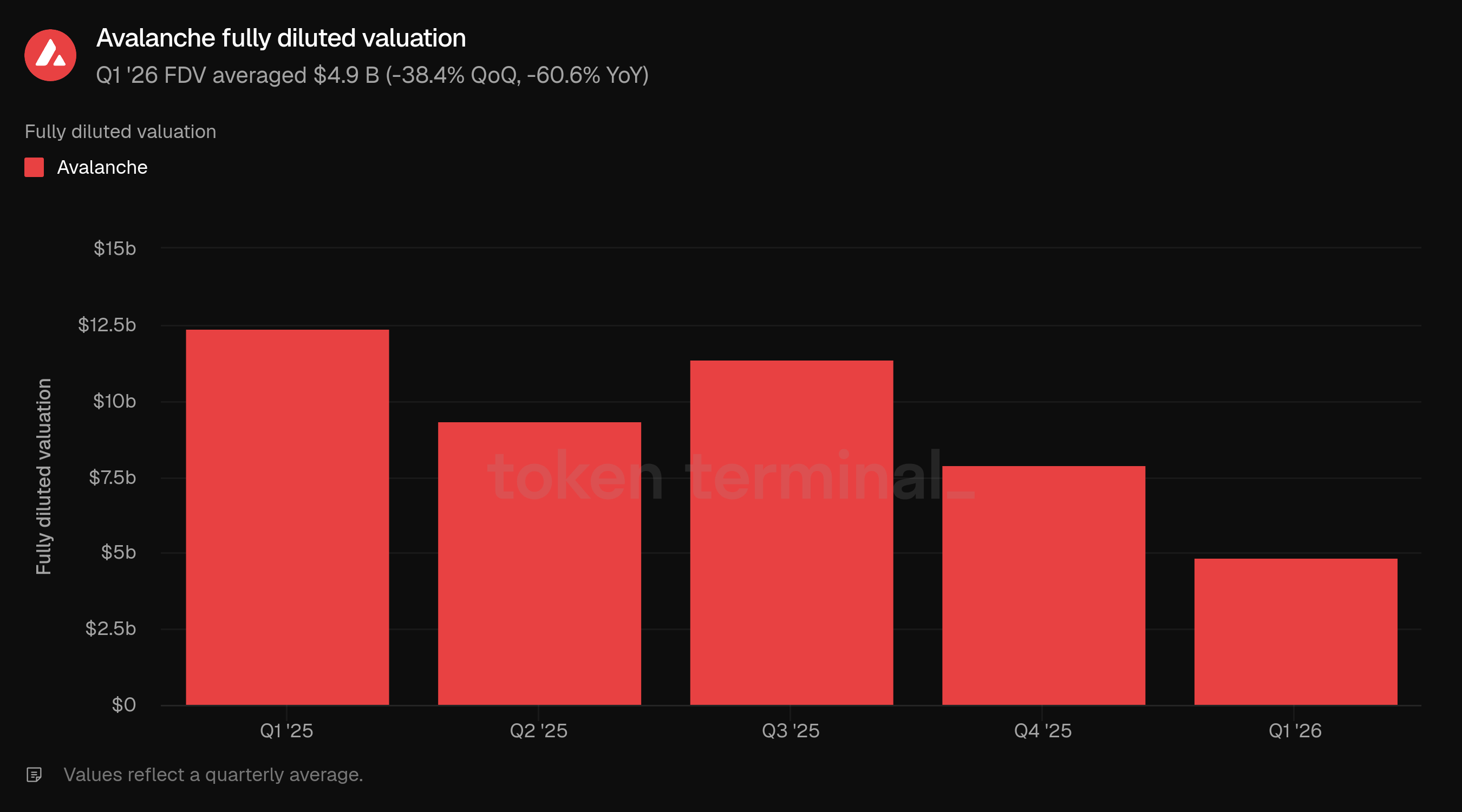

10) Fully diluted valuation

Fully diluted valuation (FDV) measures Avalanche's token valuation assuming full dilution, calculated as AVAX price multiplied by total supply. Q1 FDV averaged $4.9 B, down 38.4% from $7.9 B in Q4 and down 60.6% from $12.4 B in Q1 2025.

FDV declined despite higher transaction count, TPS, MAU, and year-over-year ecosystem TVL and active-loan growth. This reflects the broader Q1 crypto market drawdown and the gap between network-usage indicators and token-market performance during the quarter.

The FDV decline was directionally consistent with weaker market conditions across crypto. For Avalanche specifically, the key analytical question is whether continued institutional deployment, L1 adoption, and C-Chain usage can translate into more durable economic activity over time.

👥 Ava Labs team commentary

"Recent token price softness across the digital asset market is best understood as a sector-wide dynamic rather than a signal about Avalanche's underlying trajectory. Bitcoin, the largest and most liquid digital asset in the world, ended 2025 down roughly 30.0% from its peak, and the broader rotation out of risk assets affected the entire crypto market. The market is also working through a rethink of how digital assets should be valued, with the rise of high-revenue app-chains and fee-generating ecosystems pushing investors toward a sharper cash flow and protocol revenue lens, creating near-term headwinds for infrastructure-layer tokens where value capture plays out over a longer time horizon.

The metrics that tell a more complete story are tied to real on-chain GDP signals: consistent application revenue, fee generation as a measure of productive infrastructure use, stickiness of returning users, and capital flows across the ecosystem. Application-level fees reached roughly $20.0 M in Q1, gas used grew 200.0% year-over-year, and 507,000 ICM messages were exchanged across 45 actively interoperating L1s, showing capital moving across DeFi, payments, and tokenization rails. Value accrual to AVAX compounds across multiple layers as the network grows: C-Chain fees are burned in full, and every L1 in the ecosystem contributes ongoing burn streams through continuous P-Chain validator fees under the pay-as-you-go model. These are not settled questions, and we are investing in the rigor to work through them, with an independent research program and committee drawing on leading academics in economics and decentralized network design to inform how value accrual and validator incentives evolve on Avalanche over time."

11) Outlook

Avalanche's next phase will likely be judged by how effectively its L1 and C-Chain infrastructure converts production deployments into durable usage. The Q1 commentary points to a strategy centered on embedded financial rails: payments, stablecoins, tokenized credit, and fintech distribution where Avalanche operates in the background as settlement infrastructure.

Institutional finance remains the clearest near-term opportunity. Progmat, OpenTrade, BlackRock BUIDL, Avant Protocol, FUSD, and private-credit partners all point to demand for tokenized assets that can move beyond passive on-chain holdings and become productive collateral, settlement assets, or consumer-facing financial products.

Usage growth should be evaluated with more nuance going forward. Higher transaction count, TPS, and MAU are encouraging, but the key questions are whether users return, whether activity reflects real economic flows, and whether low fees can remain resilient against spam while still supporting broad application growth.

For AVAX, the important question is whether this activity translates into clearer value accrual over time. C-Chain fee burns, P-Chain validator fees from Avalanche L1s, application-level revenue, stablecoin transfer volume, and cross-L1 activity are likely to be more useful signals than FDV alone.

12) Definitions

Metrics:

Ecosystem total value locked: measures the total USD value of user deposits into applications on Avalanche.

Ecosystem stablecoin supply: measures the total USD value of outstanding stablecoins issued on Avalanche.

Ecosystem active loans: measures the total USD value of outstanding loans issued by lending applications on Avalanche.

Ecosystem trading volume: measures the total USD value of DEX trades executed by applications on Avalanche.

Fees: measures the total USD value paid by users to transact on Avalanche.

Transaction count: measures the total number of confirmed transactions on Avalanche.

Transactions per second: measures the average transaction throughput on Avalanche during the period.

Monthly active users: measures the number of unique addresses that sent at least one transaction on Avalanche within a rolling 30-day window.

Fully diluted valuation: measures Avalanche's token valuation assuming full dilution, calculated as AVAX price multiplied by total supply.

13) About this report

This report is published quarterly and produced leveraging Token Terminal's end-to-end onchain data infrastructure. All metrics are sourced directly from blockchain data. Charts and datasets referenced in this report can be viewed on the corresponding Avalanche Q1 2026 Report dashboard on Token Terminal.