Researching Plasma technology reveals two distinct but related concepts: the original Ethereum Plasma, introduced in 2017 as a scaling framework, and the modern Plasma Network (XPL), which has evolved into a specialized payment-focused blockchain for stablecoins. The contemporary Plasma Network is actively trading and gaining traction in the 2025–2026 market, and it is fundamentally different from other general-purpose Layer 2 solutions.

Its primary mission is to address the frictions and inefficiencies that businesses, traders, and individuals face when transferring stablecoins such as USD₮ on conventional blockchains. On networks like Ethereum, sending a stablecoin is not as simple as transferring money in a bank or via a messaging app. Users must first hold a separate native token, like ETH or MATIC, to pay for gas fees, which adds a layer of complexity and cost. Furthermore, high transaction fees make micro-transactions or frequent transfers impractical, and the limited scalability of general-purpose blockchains often leads to network congestion, slowing down urgent payments.

Plasma Network tackles these issues by providing a payment-first architecture that aims to make digital dollar transfers as seamless as sending a text message, eliminating the typical frictions associated with gas tokens, fees, and network congestion. Its focus on stablecoins allows it to optimize for speed, cost, and usability rather than trying to support all possible blockchain applications. This specialization makes it highly practical for real-world financial use cases, particularly cross-border payments and business settlements.

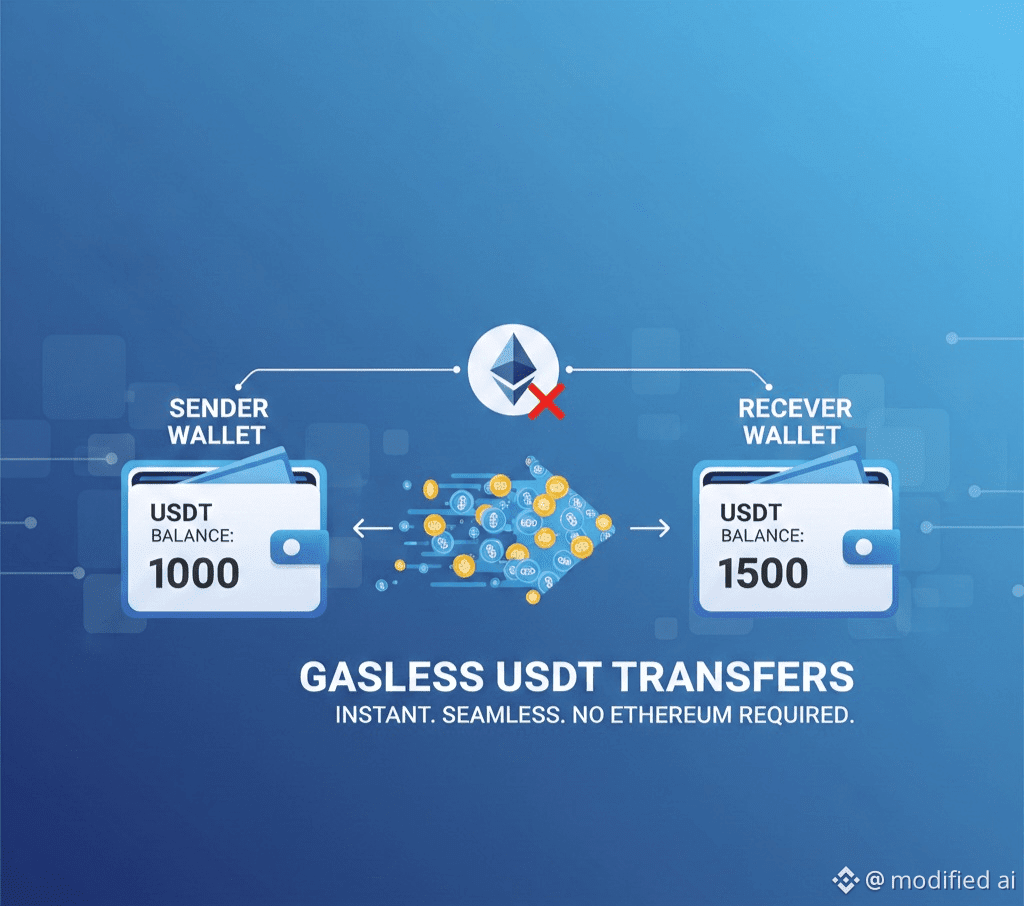

Technically, Plasma Network differentiates itself through a blend of security and speed, combining the robustness of Bitcoin with the programmability of Ethereum. Unlike traditional Layer 2 rollups, Plasma allows users to pay transaction fees directly in the stablecoin they are transferring, or even enjoy completely gasless transactions via “Protocol-Managed Paymasters.” This innovation removes the dependency on a separate gas token, which is often the largest hurdle for non-crypto-native users.

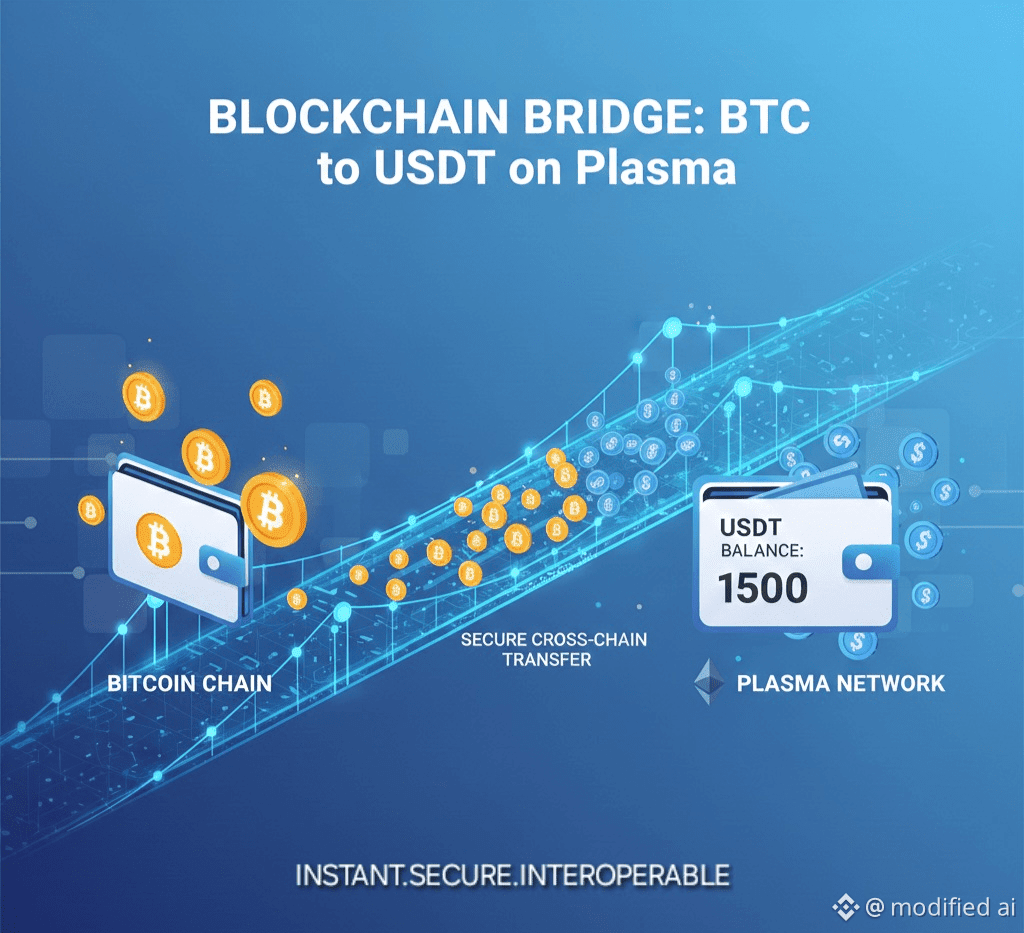

Plasma also uses a high-speed Byzantine Fault Tolerance consensus called PlasmaBFT, capable of processing over 1,000 transactions per second, offering both security and scalability. While most rollups rely on a single sequencer, which can become a point of centralization, Plasma’s architecture aims to distribute validation more robustly. Moreover, Plasma has integrated a native Bitcoin bridge called pBTC, enabling BTC holders to provide liquidity or use Bitcoin as collateral directly on the network. This level of interoperability, combined with full Ethereum Virtual Machine (EVM) compatibility, allows developers to easily migrate Ethereum-based applications onto Plasma without rewriting code.

The period from 2025 to 2026 has been significant for Plasma’s development and adoption. One of the most notable milestones was the activation of the Bitcoin bridge in early 2026, allowing users to leverage Bitcoin as collateral for stablecoin transactions, creating additional liquidity pathways and expanding the network’s utility. The Plasma One neobank, which is native to the stablecoin ecosystem, also underwent geographic expansion, entering markets in Southeast Asia and Latin America with the potential to serve over 150 million users.

By September 2025, the integration of Protocol-Managed Paymasters enabled the network to handle large volumes of zero-fee USD₮ transfers, demonstrating the practical feasibility of gasless payments at scale. Partnerships with popular wallets, such as Trust Wallet and CoinW, have further enhanced accessibility for retail traders, simplifying the onboarding process and allowing users to interact with the network more intuitively. These developments collectively indicate that Plasma is not just a technical experiment but an actively growing payments infrastructure with tangible real-world use cases.

Despite these strengths, Plasma Network faces certain limitations and risks. Its focus on stablecoin payments provides a clear competitive advantage for cross-border transfers and B2B settlements, but it also introduces specialization risk. Unlike general-purpose blockchains such as Solana or Base, which attract high-volume DeFi activity and NFT trading, Plasma may not capture speculative traffic or high-frequency trading communities, potentially limiting network effects and liquidity growth.

The validator set is also in transition from a core team to external participants, creating challenges associated with “progressive decentralization.” While decentralization is the long-term goal, the current stage introduces operational risks and governance complexities. Regulatory uncertainty is another critical factor. As a payment-centric network, Plasma is particularly exposed to stablecoin regulations such as Europe’s MiCA or potential U.S. legislation like the GENIUS Act. Changes to how stablecoins like USD₮ or USDC can be issued, held, or transferred could directly impact the network’s utility.

Additionally, the technical complexity of maintaining a custom BFT consensus alongside a Bitcoin bridge introduces security risks, as any flaw in the bridge or protocol code could lead to capital loss. Competing against established Ethereum Layer 2s also remains a challenge, as liquidity, developer adoption, and network effects are already concentrated on these larger ecosystems.

In summary, the modern Plasma Network represents a highly specialized approach to blockchain payments, focusing on speed, cost efficiency, and usability for stablecoins. Its innovations, particularly gasless USD₮ transfers and the Bitcoin bridge, create tangible advantages for businesses and users seeking a frictionless payment layer. However, its narrow focus, centralization transitions, regulatory exposure, and technical complexity highlight that adoption and long-term success are not guaranteed. Plasma’s future will depend on its ability to expand user and developer adoption while navigating legal and operational risks. If these elements align, Plasma could establish itself as a leading stablecoin payment solution in 2026, although uncertainties remain, and competition from broader Layer 2 networks will continue to be significant.