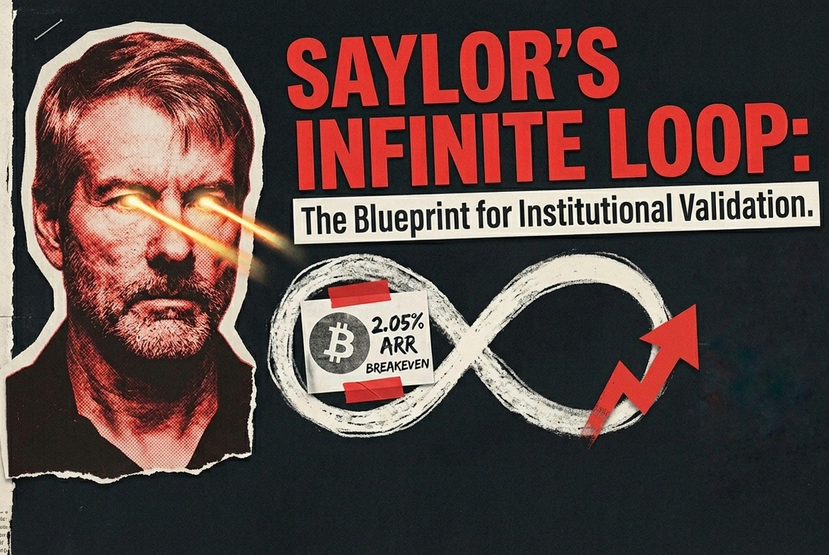

In the world of corporate finance, Michael Saylor just moved the goalposts again. For years, the bears argued that MicroStrategy $MSTR was a ticking time bomb of debt and dilution. Today, Saylor dismantled that narrative with a single number: 2.05%.

What is the "Breakeven ARR"?

Think of this as the "survival rate." Saylor is stating that as long as Bitcoin grows by a measly 2.05% per year, MicroStrategy generates enough value from its 760,000+ $BTC treasury to cover its interest and dividend payments ($STRC).

Why this is a pivot point:

• No More Dilution: They no longer need to issue new shares just to keep the lights on or pay dividends.

• Self-Sustaining Energy: MSTR has officially transitioned from a company "buying Bitcoin" to a "Bitcoin-powered machine" that pays for itself.

The $STRC Factor: Turning BTC into a Dividend Engine

By using $STRC (Stretch Preferred Stock), Saylor has created a way for investors to get a "yield" backed by Bitcoin’s growth. If BTC does what it has done historically (averaging way above 2% annually), MSTR sits on a mountain of "excess value" that they can use to buy even more BTC.

How This Hits the BTC Price

1. The Ultimate Diamond Hands: This confirms that the world’s largest corporate whale has zero operational reason to sell. The sell pressure from MSTR is effectively non-existent.

2. The Blueprint for the S&P 500: Saylor just gave every CFO a math equation to justify putting BTC on their balance sheet. If you can prove BTC "pays for your debt," why wouldn't you own it?

3. The Feedback Loop: If BTC grows at 20%, 40%, or 100%, MSTR uses the "extra" 18-98% growth to stack more sats. This creates a perpetual buy wall that never stops.

#