The more time I spent dissecting Plasma, the clearer it became that most coverage misses the point by obsessing over raw throughput or headline finality numbers. Plasma is not trying to be the fastest chain in abstract benchmarks. It is trying to solve a much narrower and more difficult problem that institutions actually care about. When a bank, PSP, or treasury desk settles stablecoins, finality is not a UX feature. It is a legal, accounting, and risk boundary. Plasma’s architecture makes sense only when viewed through that lens, and once you do, many of its design choices stop looking conservative and start looking deliberate.

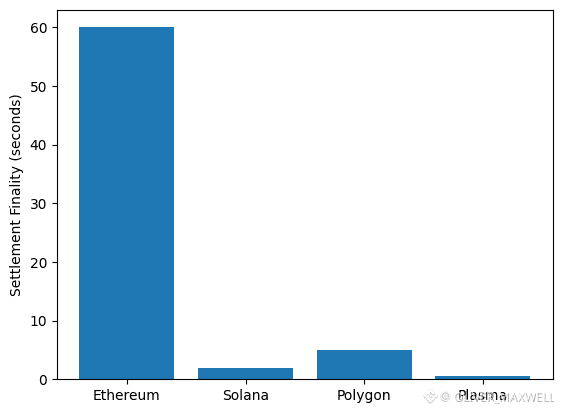

Plasma’s combination of full EVM compatibility and sub second finality creates a very specific competitive posture. Ethereum optimizes for decentralization and composability but accepts multi minute settlement latency as a tradeoff. Solana optimizes for speed but couples execution, consensus, and state so tightly that operational risk becomes part of the cost of performance. Polygon and similar chains sit in between, but still treat stablecoins as just another asset class. Plasma is different because stablecoin settlement is not an application on top of the chain. It is the organizing principle of the chain itself. EVM compatibility exists to reduce integration friction, not to attract maximal DeFi experimentation. That distinction matters because it shapes every downstream design decision.

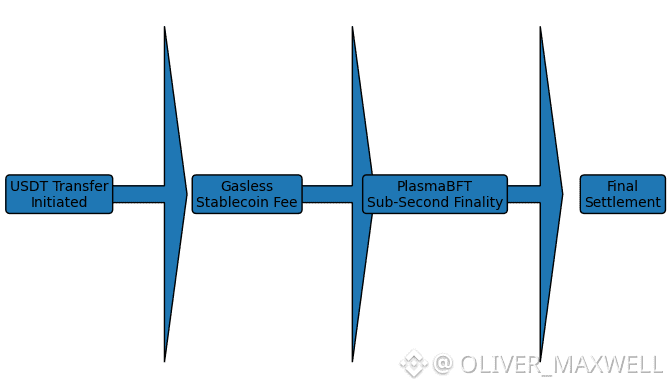

The PlasmaBFT consensus mechanism is where this philosophy becomes concrete. Sub second finality is not achieved by pushing validators to extreme hardware limits or by accepting probabilistic settlement. Instead, Plasma treats finality as a first class primitive. Transactions reach an irreversible state fast enough that they can be treated as completed obligations rather than pending intents. For institutions, that difference is critical. It enables atomic settlement flows where reconciliation, compliance checks, and balance sheet updates can happen immediately. Other high speed chains often conflate fast block production with final settlement. Plasma separates the two and optimizes explicitly for the latter. The tradeoff is that Plasma does not try to be everything to everyone. It sacrifices some generality to guarantee a settlement experience that other chains cannot consistently provide.

That design choice becomes even more visible in Plasma’s stablecoin first gas model. Gasless USDT transfers are not a marketing gimmick. They are an acknowledgment that requiring users or institutions to manage a volatile native token is one of the biggest blockers to real world payments. By anchoring transaction costs directly to stablecoins, Plasma makes costs predictable, auditable, and finance friendly. Treasury teams can model expenses without hedging gas exposure. Payment providers can abstract blockchain complexity away from end users entirely. The obvious limitation is that this architecture deprioritizes non stablecoin activity. Plasma is implicitly saying that if your use case is not centered on stable value transfer, this may not be your chain. That focus is not a weakness. It is what allows the rest of the system to stay coherent.

The Bitcoin anchored security model reinforces this coherence in a subtle but important way. Rather than competing on novel cryptoeconomic assumptions, Plasma borrows credibility from the most battle tested settlement layer in existence. Anchoring to Bitcoin is less about raw security metrics and more about neutrality. For regulated financial infrastructure, perceived neutrality is as important as cryptographic guarantees. Institutions want assurance that no single ecosystem actor can arbitrarily rewrite settlement history or exert governance capture. Bitcoin anchoring sends a signal that Plasma’s settlement layer is not easily politicized or forked for convenience. Compared to chains whose security rests entirely on their own token economics, Plasma positions itself as structurally harder to coerce, even if that comes at the cost of slower governance agility.

Institutional adoption barriers tend to cluster around a few recurring issues. Settlement speed that is fast but not final enough. Costs that are cheap but unpredictable. Integration paths that require deep crypto native expertise. Plasma’s architecture addresses these points directly rather than indirectly. EVM compatibility lowers integration costs. Sub second finality aligns with operational settlement windows. Stablecoin denominated fees simplify compliance and accounting. That does not mean adoption is guaranteed. Institutions are slow by nature, and Plasma still has to prove reliability at scale. But the way Plasma attacks these barriers is more aligned with how institutions actually think than most blockchain payment narratives.

Tokenomics and validator economics further reveal Plasma’s priorities. The token is not positioned as a speculative growth asset first. Its role is to secure the network, align validators, and support governance without forcing payment flows through a volatile unit of account. This reduces reflexive speculation but improves long term settlement credibility. Validator incentives appear designed to favor reliability and uptime over aggressive yield extraction. From a trader’s perspective, this may look less exciting. From a network health perspective, it creates a validator set that behaves more like infrastructure providers than mercenary capital.

Retail adoption in high stablecoin usage markets is often framed as a question of wallets and UX. Plasma reframes it as a question of trust and predictability. In regions where stablecoins already function as informal dollars, users care less about decentralization narratives and more about whether transfers clear instantly and fees remain stable. Plasma’s architecture aligns with those expectations. The challenge will be distribution and onramps, not protocol capability. Plasma is technically prepared for retail scale, but market access will determine whether that potential is realized.

Looking forward, Plasma occupies a defensible but narrow corridor in the blockchain landscape. It is not trying to replace Ethereum as a global settlement layer for all assets. It is not trying to outpace Solana on raw throughput. Its bet is that stablecoin settlement will continue to professionalize and that institutions will demand infrastructure built explicitly for that purpose. If stablecoins remain the dominant bridge between traditional finance and onchain systems, Plasma’s design choices look increasingly prescient. If the market shifts toward more generalized onchain finance without stablecoin dominance, Plasma’s focus could become a constraint.

What stands out after deep analysis is that Plasma feels less like a crypto project chasing narrative momentum and more like infrastructure built by people who have watched institutions struggle with blockchain adoption up close. Its architecture is opinionated, and that opinion is clear. Settlement should be fast, final, neutral, and boring in the best possible way. If Plasma succeeds, it will not be because it was the loudest chain in the market. It will be because it quietly became the one institutions trusted to move value without surprises.