When I first started exploring Newton Protocol I assumed it was another blockchain project focused on improving security. After spending more time understanding its architecture I realized the bigger idea is not simply about making transactions safer. It is about creating a system where artificial intelligence can participate in finance without receiving unlimited authority over assets.

That difference completely changed how I think about the project.

AI is becoming more capable every year. Modern AI agents can analyze markets compare lending opportunities monitor liquidity and identify profitable strategies within seconds. In many cases they can process information much faster than a human trader or portfolio manager. But speed alone does not solve the biggest challenge facing autonomous finance.

The real challenge is trust.

An AI model can make intelligent decisions but it can also misunderstand data respond to manipulated information or simply make an unexpected mistake. If that same AI has unrestricted control over a wallet then a single error could immediately become an irreversible blockchain transaction.

Newton approaches this problem from a different direction.

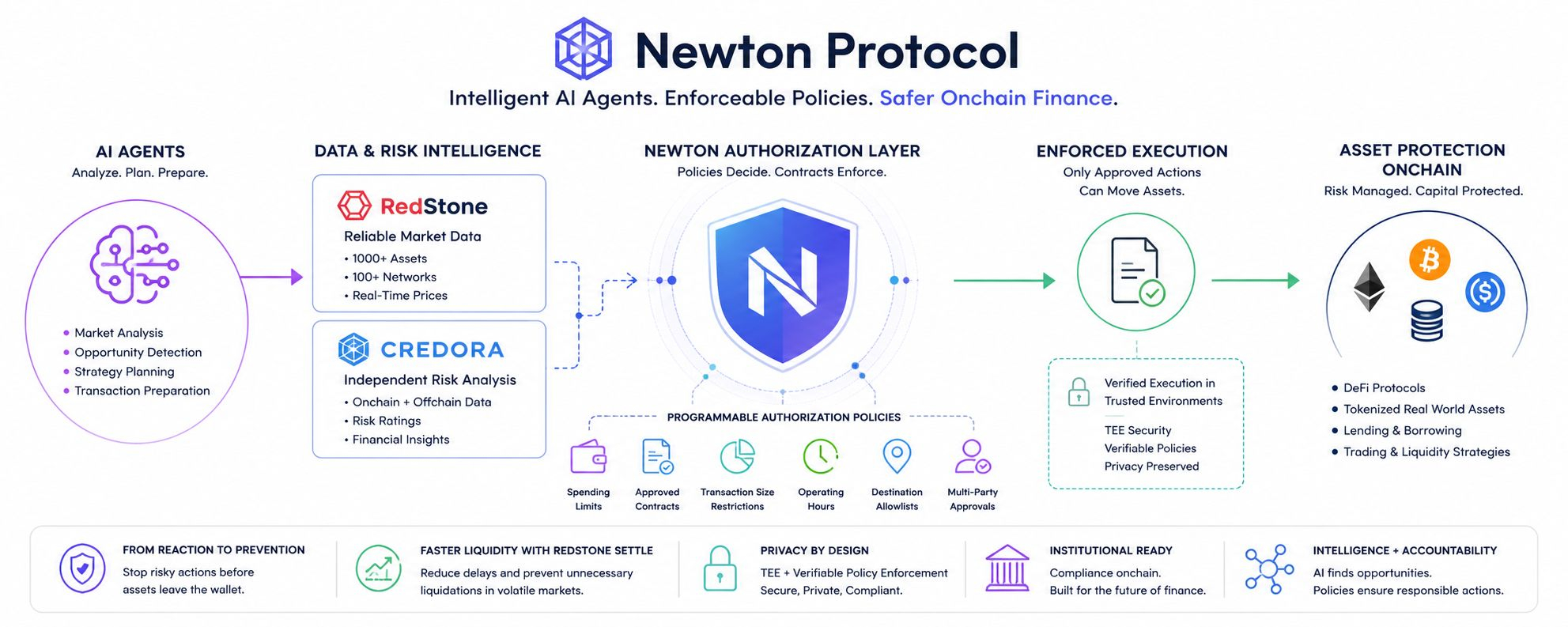

Instead of allowing intelligence and authority to exist together Newton separates them. AI agents remain responsible for research analysis and transaction preparation while execution is controlled by programmable authorization policies. Every action must satisfy predefined rules before assets can move.

To me this feels like a much more realistic approach to building autonomous financial systems.

One feature that impressed me is the flexibility of those policies. Users or institutions can define spending limits approved contracts transaction size restrictions operating hours destination allowlists and additional approval requirements. The AI continues doing what it does best by finding opportunities and preparing strategies while the authorization layer decides whether those actions fall within acceptable risk limits.

That balance is important because intelligence creates possibilities but authorization determines which possibilities are actually allowed to become real transactions.

While learning more about Newton I also became interested in its growing ecosystem especially its collaboration with RedStone and Credora.

I think this partnership explains why Newton is trying to solve a much larger problem than transaction authorization alone.

Every decentralized financial application depends on reliable market data. Without accurate pricing protocols cannot value collateral manage liquidations or calculate risk correctly. RedStone supplies that foundation by delivering blockchain price data across a large number of digital assets and networks.

Raw market data however is only one part of the equation.

Understanding whether an asset or strategy carries acceptable risk requires another layer of analysis. That is where Credora contributes. Instead of simply presenting numbers it evaluates financial risk using both onchain and offchain information to create ratings that institutions and professional users can actually use when making decisions.

Newton then adds the final layer.

Rather than leaving those risk assessments inside dashboards documents or internal operating procedures Newton transforms them into programmable rules that smart contracts can automatically enforce. In simple terms data becomes intelligence and intelligence becomes action.

This changes the way risk management works.

Traditional financial systems often discover problems after losses have already happened. Investigations begin once damage has been done. Newton attempts to reverse that process by allowing policies to prevent risky transactions before they are completed. Instead of asking what went wrong afterward the system tries to stop dangerous actions before assets ever leave the wallet.

I believe this shift from reaction to prevention could become increasingly valuable as AI agents begin managing larger amounts of capital.

Another area that caught my attention is RedStone Settle.

One challenge facing tokenized real world assets is liquidity. Many assets cannot always be redeemed immediately which creates delays exactly when investors may need access to their capital. RedStone Settle is designed to reduce that friction by providing faster liquidity during situations that could otherwise trigger unnecessary liquidations or financial stress.

Although this technology continues to develop I think it highlights an important direction for decentralized finance. Better infrastructure is not only about increasing transaction speed. It is also about making markets more resilient when conditions become difficult.

Privacy is another aspect that makes Newton stand out.

Many compliance systems require users to trust centralized services that verify sensitive information behind closed doors. Newton takes a different approach by using Trusted Execution Environments together with verifiable policy enforcement. Sensitive information remains protected while users can still verify that policies were evaluated correctly.

I find this particularly interesting because financial institutions care about two things that often appear difficult to combine.

They need privacy to protect confidential information.

They also need transparency to satisfy regulators auditors and customers.

Newton attempts to deliver both without forcing organizations to choose one over the other.

As governments continue introducing stronger AML and KYC expectations around digital assets this type of infrastructure may become increasingly relevant. Instead of relying entirely on front end applications or centralized monitoring systems compliance rules can become part of the smart contract itself while maintaining user privacy.

That capability could make decentralized applications more attractive for institutions that require clear operational controls before deploying meaningful capital onchain.

Of course technology alone never guarantees adoption.

History shows that many excellent infrastructure projects arrive years before the market fully recognizes their value. Developers must integrate new tools businesses must adjust their workflows and users must gain confidence before any new standard becomes widely accepted.

Newton still faces those challenges.

However I think the project is solving a problem that will become increasingly important rather than simply following today's trends.

As AI agents continue evolving they will manage larger portfolios execute more transactions and participate in increasingly complex financial strategies. When that happens the industry will need systems capable of defining not only what AI can calculate but also what AI is permitted to do.

That distinction may ultimately become one of the foundations of autonomous finance.

After spending time researching Newton Protocol I no longer see it as only an authorization layer. I see it as infrastructure designed to connect intelligent automation reliable market data independent risk analysis privacy and enforceable onchain policies into one coordinated system.

Whether adoption happens quickly or gradually is impossible to predict.

What seems much clearer to me is that the future of AI powered finance will depend on more than faster algorithms or larger models. It will depend on building systems that can combine intelligence with accountability.#newt

In my opinion that is exactly the direction Newton Protocol is trying to take. If decentralized finance wants to welcome institutions support autonomous AI agents and manage billions of dollars responsibly then preventing unnecessary risk before it becomes a loss may prove far more valuable than simply responding after the damage has already been done.#Newt