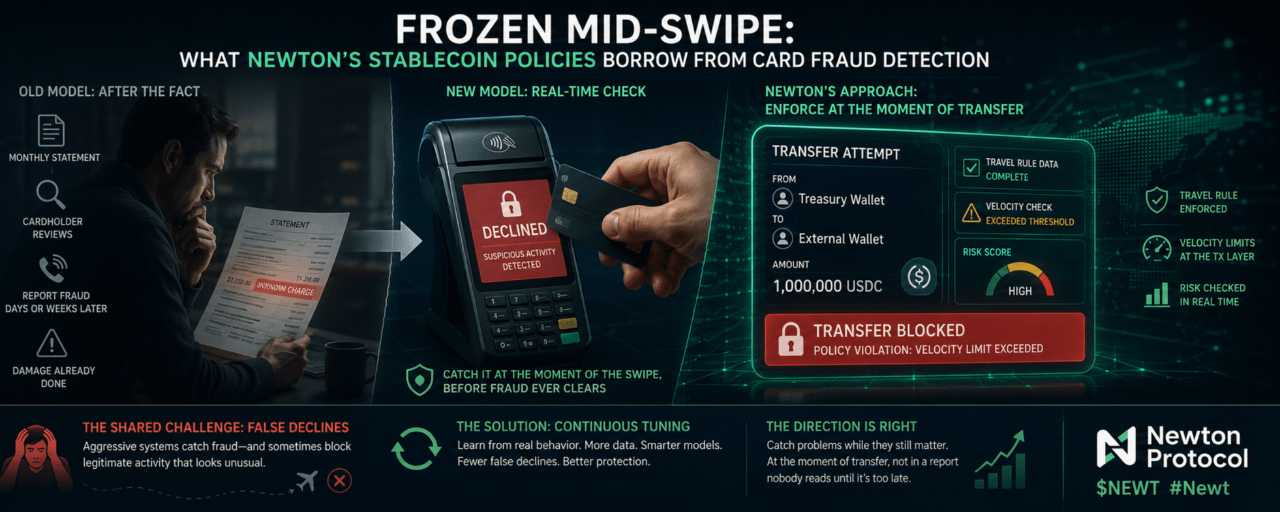

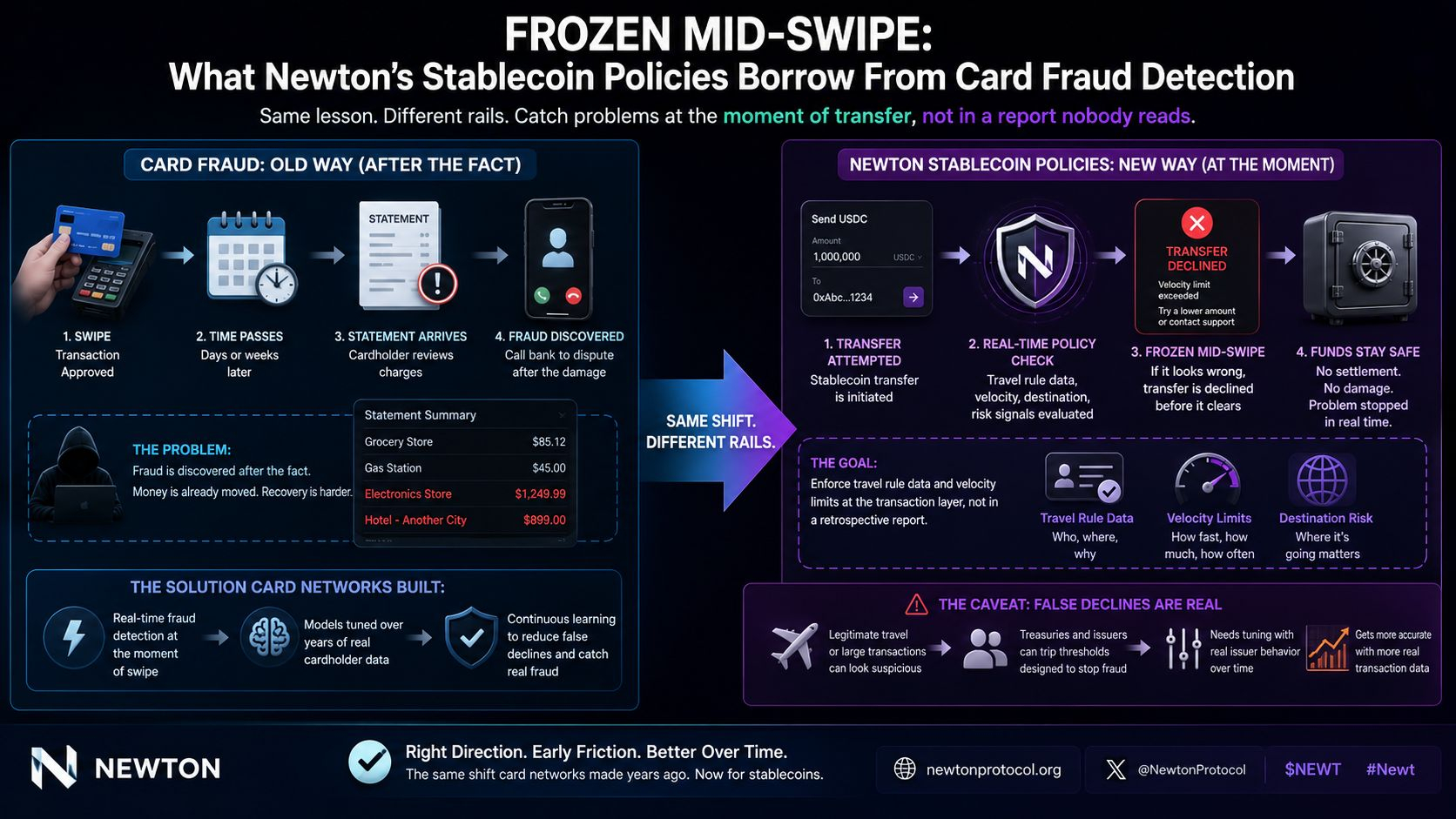

Credit card fraud detection used to work almost entirely after the fact. A statement would arrive at the end of the month, a cardholder would scan through it, notice a charge from a city they'd never visited, and call the bank to dispute it, days or weeks after the actual fraud happened. That model still exists in the background of some systems today, but the meaningful advance in fraud prevention over the last couple decades has been moving the check earlier, to the moment of the swipe itself, where a card can actually get declined in real time if the pattern looks wrong, before the fraudulent charge ever clears.

Newton's stablecoin policies are built on that same shift in timing, applied to a different kind of transfer. Instead of monitoring stablecoin movement after the fact and flagging suspicious patterns in a retrospective report, Newton enforces travel rule data requirements and velocity limits directly at the transaction layer, at the moment a transfer is attempted, the stablecoin equivalent of a card getting declined at the register instead of a fraudulent charge getting caught a month later on a statement nobody reads closely enough.

That's a meaningfully heavier lift than what most stablecoin compliance has looked like so far. Simple KYC at onboarding is the stablecoin equivalent of a bank verifying your identity once when you open an account and then trusting every transaction indefinitely afterward, regardless of pattern, regardless of destination, regardless of velocity. Enforcing travel rule data and velocity thresholds at the point of transfer means every movement gets evaluated against current risk signals, not just the identity established once at account opening. A wallet that behaved normally for months and suddenly starts moving funds at a velocity or to destinations that trip Newton's policy thresholds gets caught at that specific moment, the same way a card that's charged normally for years and then attempts an unusual pattern of transactions gets flagged by a fraud system in real time rather than waiting for a statement cycle.

Here's where the comparison needs an honest caveat, because card-swipe fraud detection has a well documented failure mode that stablecoin issuers should expect to inherit too, false declines. Anyone who's had a legitimate purchase rejected while traveling, or making an unusually large but entirely legal transaction, knows the frustration of a fraud system that's tuned aggressively enough to catch real fraud also catching perfectly legitimate activity that happens to look statistically unusual. Newton's velocity limits carry the exact same risk. A legitimate high frequency treasury operation, an institutional issuer moving stablecoins at genuine business velocity, can trip the same thresholds designed to catch an actual attack pattern, because from a pure pattern matching standpoint, unusually fast, high volume movement looks similar whether it's malicious or just a normal business day for a large treasury desk.

Card networks solved this, imperfectly but meaningfully, by continuously tuning fraud models against real cardholder behavior over years of data, learning the difference between a legitimate frequent traveler and an actual stolen card being tested at speed. Newton's stablecoin policies are going to need the same kind of tuning against real issuer behavior before velocity limits stop being a blunt instrument and start reliably distinguishing normal high frequency activity from an actual attack. That tuning takes real transaction history to build, the same way card fraud models took years of real purchase data before they stopped declining as many legitimate transactions as they were catching fraudulent ones.

I think the direction is right regardless. Catching a problem while it still matters, at the moment of transfer rather than in a report nobody reads until the damage is already done, is the correct shift for stablecoin compliance to make, the same shift card networks already proved out at massive scale. The honest expectation for Newton isn't that the first version of these velocity limits will get the tuning right immediately. It's that, like fraud detection before it, the system gets more accurate the more real transaction data it has to learn from, and the early friction is the cost of building a system that can eventually tell the difference reliably.