I remember getting caught in one of those “infrastructure rotations” a while back. You know the type narratives around identity, data layers, middleware… everything sounds foundational, so you assume the market will eventually price it that way. I chased a couple of those plays purely on the idea that “this feels important.”

Most of them never translated into real usage. Just dashboards, partnerships, and vague promises.

That’s probably why SIGN confused me the first time I looked at it.

Because this one doesn’t feel like a story-first project. It feels… implemented. And that disconnect has been sitting in my head for a while now.

The more I dig into SIGN, the more I keep coming back to one simple thought:

Either this is undervalued infrastructure… or the market sees a structural issue that isn’t obvious at first glance.

I don’t think it’s somewhere in between. It’s one of those cases where the outcome will be very clear in hindsight.

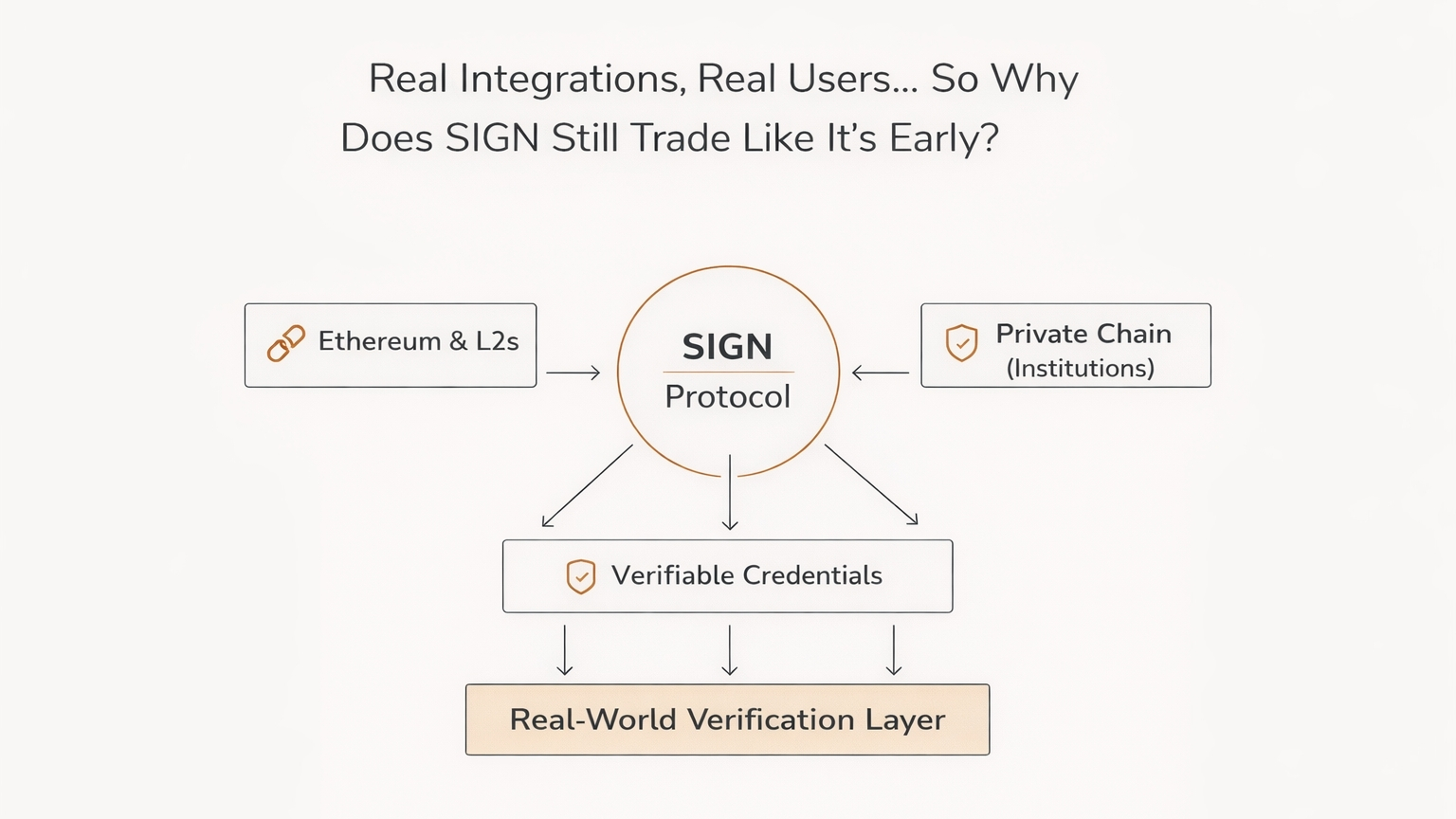

At a surface level, people call SIGN an identity or credential protocol. That’s technically correct, but it doesn’t really explain anything.

The way I understand it now is simpler:

SIGN is trying to become the verification layer for digital claims.

Not just “who you are,” but:

- What you’ve done

- What you’re eligible for

- What someone else can prove about you

And instead of storing that data directly, it allows entities (governments, platforms, protocols) to issue verifiable credentials that can be checked without exposing the raw data.

That’s where Sign Protocol comes in.

Think of it like this:

If Ethereum is where transactions are verified, Sign Protocol is where claims are verified.

Someone issues a credential → it’s recorded in a structured way → anyone with permission can verify it.

Now where it gets more interesting is how this connects to their other pieces.

TokenTable is not just some side product. It’s actually one of the clearest signals that SIGN isn’t purely theoretical.

It’s being used for:

- Token distributions

- Airdrop allocations

- Vesting and cap table management

That means real projects are already relying on SIGN’s infrastructure to manage who gets what, and why.

That’s not narrative. That’s operational.

And more importantly, it generates real revenue, which most “identity layer” projects never reach.

At first I didn’t fully get why SIGN needed both:

- A public L2

- A private network (for CBDCs / institutions)

It felt like overengineering.

But the more I thought about it, the more it started making sense.

Public chain → open verification, crypto-native use cases

Private chain → governments, regulated environments, sensitive data

And SIGN sits between them as a bridge of trust.

Not bridging assets bridging credibility.

That’s a very different positioning compared to most Web3 infra.

Now here’s where things get a bit uncomfortable.

Because when you look at the numbers, they don’t cleanly match the “infrastructure narrative.”

Without throwing random figures around, a few things stand out:

- Circulating supply is still relatively low compared to total supply

- There’s a meaningful gap between market cap vs FDV

- Unlock schedules aren’t negligible they will introduce pressure

- Revenue exists (TokenTable), but it’s not yet at a scale that forces revaluation

So you end up in this weird spot:

The product looks ahead of its valuation… but the token structure looks like it belongs to an earlier-stage project.

And I think the market is reacting more to the second part than the first.

The Core Tension

This is where my thinking keeps circling back.

SIGN feels like it’s already:

- Integrated into real workflows

- Used by actual projects

- Positioned toward institutional adoption

But it’s still priced like:

- Adoption is uncertain

- Revenue is speculative

- Token pressure is ahead

So what’s going on?

I don’t think this is just “market inefficiency.”

There are a few things that could justify the current pricing:

Even if the product is strong, supply expansion can suppress price for a long time.

If new tokens keep entering the market faster than demand grows, the price won’t reflect fundamentals immediately.

This is something people consistently underestimate.

A big part of SIGN’s long-term thesis relies on:

- Governments

- Large organizations

- Regulated environments

That’s powerful… but also slow.

Adoption cycles here don’t move like DeFi or memecoins.

They move in quarters, sometimes years.

The market might simply be discounting that timeline.

Yes, TokenTable generates revenue.

But the question is:

Is it enough to justify a re-rating today, or just proof of potential?

If it’s the latter, then current pricing starts to make more sense.

What Feels Off (My Personal Take)

This is the part I keep thinking about.

If SIGN were pure narrative, I’d understand the pricing.

If it were purely early-stage, same thing.

But it’s neither.

It’s already being used in ways most identity projects never reach.

And yet, the market still treats it cautiously.

That usually happens when:

- Either something is misunderstood

- Or something structural is limiting upside

Right now, I’m leaning slightly toward the first but not confidently.

My Working Thesis

I think the market is:

Overweighting token dynamics and underweighting real usage.

Not ignoring it completely just not giving it enough importance yet.

In other words:

SIGN might not be mispriced because it lacks fundamentals…

It might be mispriced because those fundamentals don’t immediately translate into token demand.

And that gap can persist longer than people expect.

What Would Change My Mind

I try to keep this part clear, otherwise it just becomes bias.

This thesis gets stronger if:

- TokenTable revenue shows consistent growth

- More projects depend on SIGN for critical flows

- Institutional integrations move from “announced” to “actively used”

- Circulating supply increases without crushing price

That last one is important. It would signal real demand absorbing supply.

This thesis breaks if:

- Unlock pressure keeps outweighing demand

- Usage stagnates or stays niche

- Institutional adoption remains slow or symbolic

- Revenue fails to scale beyond early traction

If those things happen, then the current pricing isn’t a mistake it’s accurate.

Where I Land (For Now)

I don’t think SIGN is a clear “easy bet.”

It’s one of those projects where:

- The product makes sense

- The use cases are real

- But the market translation is still unclear

And maybe that’s the whole point.

Most people wait for everything to align product, token, narrative.

By the time that happens, the repricing is usually already done.

SIGN feels like it’s sitting right before that moment… or stuck in a structure that prevents it from ever fully reaching it.

I haven’t fully decided which one it is yet.

But I keep coming back to the same thought:

If real-world verification becomes a core layer of Web3 and digital systems, something like SIGN probably has a place.

The only question is whether the token captures that value…

or just enables it quietly in the background.

@SignOfficial #SignDigitalSovereignInfra $SIGN