The most expensive duplicate in automated finance may be a perfectly valid authorization used one more time than intended.

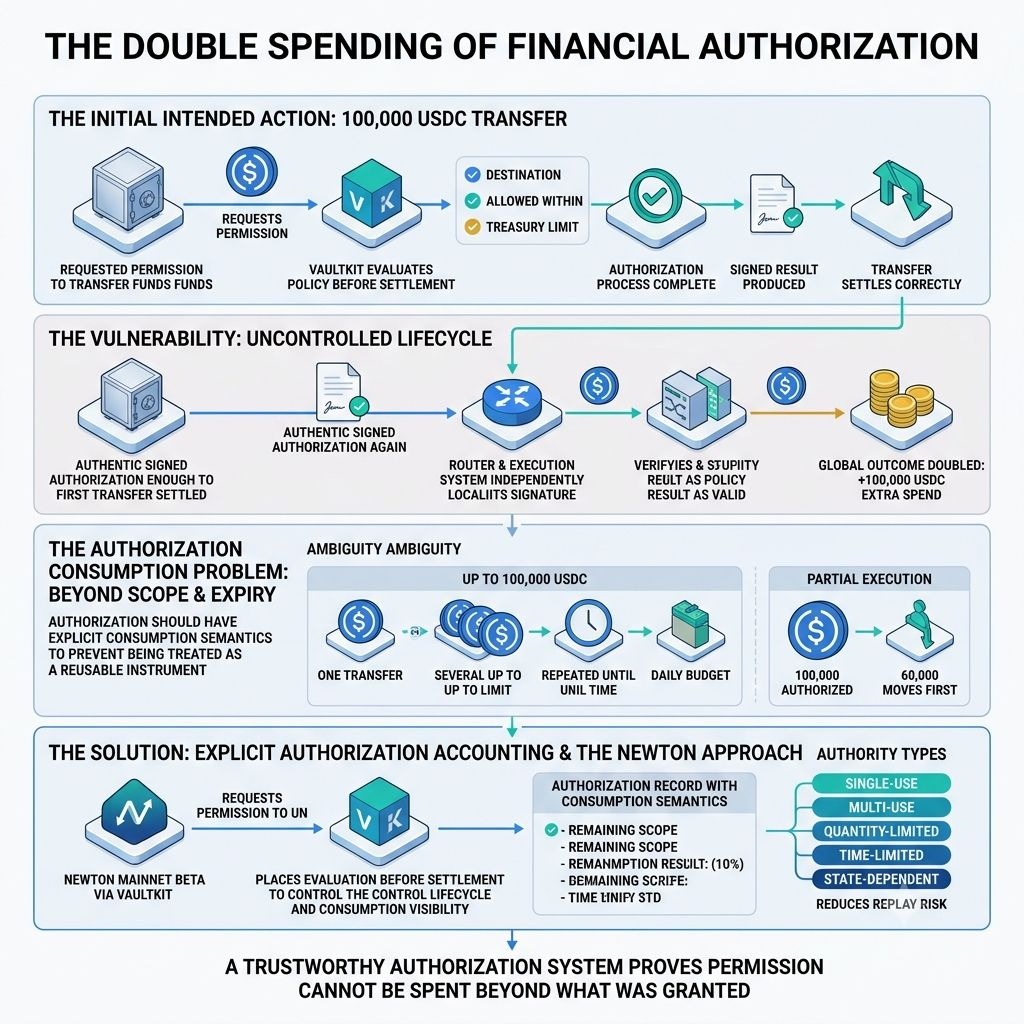

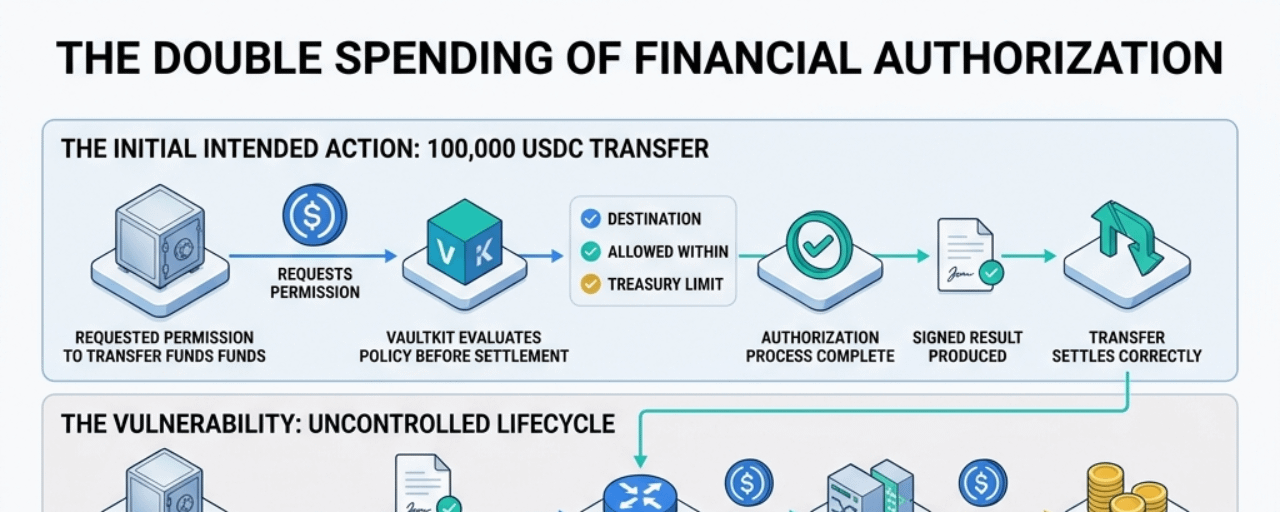

Imagine an institutional vault requests permission to transfer 100,000 USDC to an approved counterparty.

VaultKit evaluates the active policy before settlement.

The destination is allowed.

It is still within the treasury limit.

The required authorization process completes, and a signed result is produced.

The transfer settles correctly.

Then the same authorization is submitted again.

The signature is still genuine.

The policy result was valid when created.

The destination remains approved.

Yet the second transfer may never have been intended.

Nothing needs to be forged.

No operator needs to sign a dishonest result.

The system can lose another 100,000 USDC simply because it treated proof of one approval as reusable authority.

That is the authorization problem I think becomes critical once attestations begin moving between applications, agents, routers, and settlement systems.

A signed result can prove that a decision occurred.

It does not automatically prove that the decision has not already been consumed.

This distinction matters because financial authorization is not always a reusable statement.

Sometimes it is closer to a cheque.

The cheque may be authentic.

The signature may be valid.

The amount and recipient may be correct.

But once it has been paid, presenting the same instrument again should not create a second payment.

Automated systems need the same clarity.

An authorization should define not only what action is permitted, but also how many times that permission may be exercised.

This is where Newton Mainnet Beta becomes especially interesting to me.

Through VaultKit, applications can define policy conditions around what an agent, manager, or automated strategy is permitted to do. @NewtonProtocol can place that evaluation before settlement, creating a point where an action can still be stopped before value moves.

Signed authorization results can make the decision easier to verify and inspect.

But the stronger the system becomes at producing machine-readable approvals, the more important it becomes to control their lifecycle.

An agent does not naturally hesitate when it sees a valid signature.

A router may not know that another component already used the same result.

Two execution systems may receive the authorization at nearly the same time.

Each may independently conclude that the approval is valid.

Local verification succeeds.

The global outcome doubles the intended action.

This creates a different risk from ordinary transaction binding.

The authorization may be correctly tied to:

the intended destination,

the correct amount,

the right policy version,

and the permitted execution route.

The failure appears because the same valid authority remains usable after its intended effect has already occurred.

For me, a serious authorization record therefore needs more than scope and expiry.

It needs consumption semantics.

Was the approval valid for one execution?

Could it authorize several actions up to a cumulative limit?

Was it tied to a unique request identifier?

Did settlement mark it as used?

Could two chains or applications observe the same authorization state consistently?

What happens if two transactions attempt to consume it in the same period?

Those questions determine whether authorization remains a decision or becomes a reusable financial instrument.

Consider a policy that approves “up to 100,000 USDC.”

That phrase can have several meanings.

It may permit one transfer of no more than 100,000.

It may permit several transfers whose total remains below 100,000.

It may permit repeated transfers until a specific time.

It may describe a daily budget rather than a single action.

All four interpretations can use the same amount.

They create completely different authority.

If the policy does not express which meaning applies, every component may behave correctly according to its own interpretation while the treasury loses control of the total result.

This is why I think authorization consumption should be visible at the same level as authorization creation.

A signed approval should not only answer:

“Was this request allowed?”

It should also help answer:

“How much authority remains after this action settles?”

That becomes especially important for partial execution.

Suppose a vault receives authorization to move 100,000 USDC, but the first transaction moves only 60,000.

Is the remaining 40,000 still available?

Can the agent retry the complete 100,000 because the first transaction only partially succeeded?

Does the policy permit one attempt or one final outcome?

What happens when fees, slippage, or partial fills change the amount that actually settles?

These are not edge cases once autonomous strategies operate across real markets.

They are ordinary questions about how permission is consumed.

The same issue becomes harder across several applications.

One system may mark the authorization as used while another still sees it as available.

A cross-chain execution path may consume authority on one network before the updated state becomes visible elsewhere.

An agent may retry after a timeout without knowing whether the original transaction eventually settled.

The retry may look like responsible recovery.

It can become an unintended duplicate.

The obvious solution is to make every authorization single-use.

That would reduce replay risk.

It would also be too rigid for many legitimate workflows.

A trading strategy may need several fills.

A treasury may approve a bounded daily budget.

A debt-repayment process may require multiple transactions.

The better design is not universal one-time authorization.

It is explicit authorization accounting.

Applications should define whether authority is:

single-use,

multi-use,

quantity-limited,

time-limited,

or state-dependent.

The settlement process should reduce or close that authority according to the action that actually occurred.

And the resulting record should make the remaining scope understandable to the next system that receives it.

There is an operational trade-off.

Tracking consumption across applications can add state, coordination cost, and failure modes.

Strict synchronization may slow execution.

Loose synchronization may improve availability while allowing temporary double use.

A centralized counter can simplify accounting but create another dependency.

A distributed mechanism can reduce that dependency while making agreement harder during congestion or network disruption.

Newton does not escape these trade-offs merely because the authorization is signed.

The signature makes the decision verifiable.

The surrounding system still has to ensure that valid authority cannot be silently multiplied.

That is the standard I would use when judging Newton-powered applications.

Can an authorization be replayed after settlement?

Can several executors consume the same approval concurrently?

Can partial execution reduce the remaining authority correctly?

Can an agent distinguish a failed transaction from a delayed transaction before retrying?

Can the signed record show whether the approval is unused, partially consumed, or closed?

And can applications preserve this state without turning authorization into a bottleneck?

Danyaal’s strongest question is no longer only who signed or whether the approval can be challenged.

It is whether the authority created by that signature has a controlled ending.

A trustworthy authorization system should not merely prove that permission existed.

It should prove that permission could not be spent beyond what was granted.

Because in automated finance, one valid approval can become two unauthorized outcomes when the system forgets that authority, like capital, must be accounted for after it is used