One thing I've realized over the last few years is that crypto doesn't really have a technology problem anymore. Faster chains, cheaper transactions, better smart contracts, AI-powered agents—we've made incredible progress on all of those fronts. Yet whenever serious money, institutions, or businesses enter the picture, everything suddenly becomes more cautious.

Not because the technology stops working, but because people stop asking, "Can this be automated?" and start asking, "Can we trust this to operate within the right boundaries?"

I think that's the question that matters most.

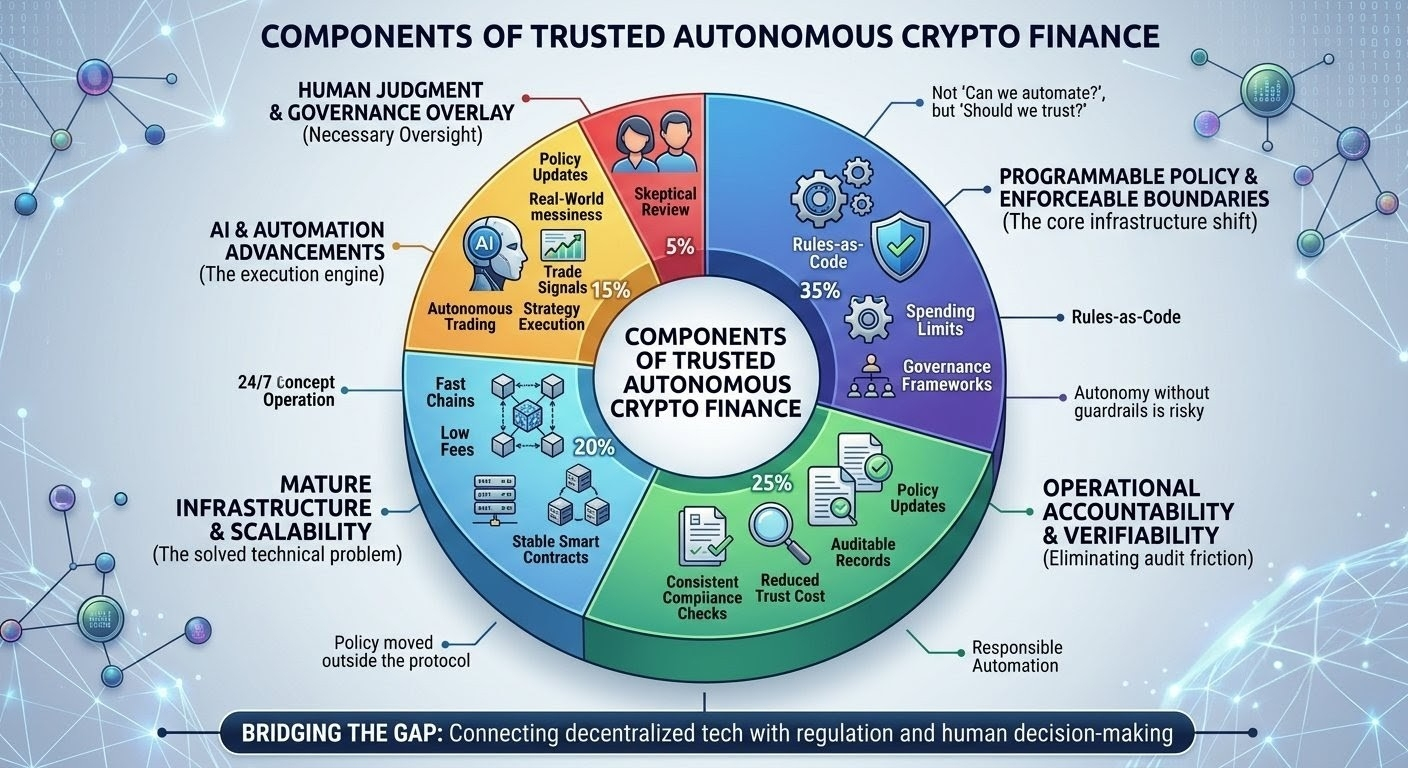

We spend a lot of time talking about autonomous finance, but autonomy alone isn't particularly valuable. An AI agent can execute trades, move assets between protocols, or manage strategies twenty-four hours a day. That's impressive, but it also raises a much more practical question: who decides what the AI is allowed to do in the first place?

In traditional finance, that answer is surprisingly straightforward. Every automated system operates inside a framework of rules. There are spending limits, approval processes, compliance checks, investment mandates, and audit requirements. These aren't there because someone enjoys bureaucracy. They're there because people have learned—sometimes the hard way—that automation without guardrails eventually creates problems.

Crypto has often approached things differently. The goal has been to remove friction, eliminate intermediaries, and let code execute exactly as written. That's a powerful idea, but as the industry has matured, something interesting has happened. Many projects have quietly started rebuilding the same controls they originally tried to remove. Multi-signature wallets, governance approvals, emergency pause mechanisms, permission systems, and manual reviews have become increasingly common.

To me, that's a sign that the need for policy never disappeared. It simply moved outside the protocol.

That's why Newton Protocol feels different from many other AI-focused projects. What caught my attention isn't the promise of smarter automation. It's the idea that the rules surrounding automation can become part of the infrastructure itself instead of being handled separately through documents, internal procedures, or human intervention.

That may not sound revolutionary at first, but I think it's a meaningful shift.

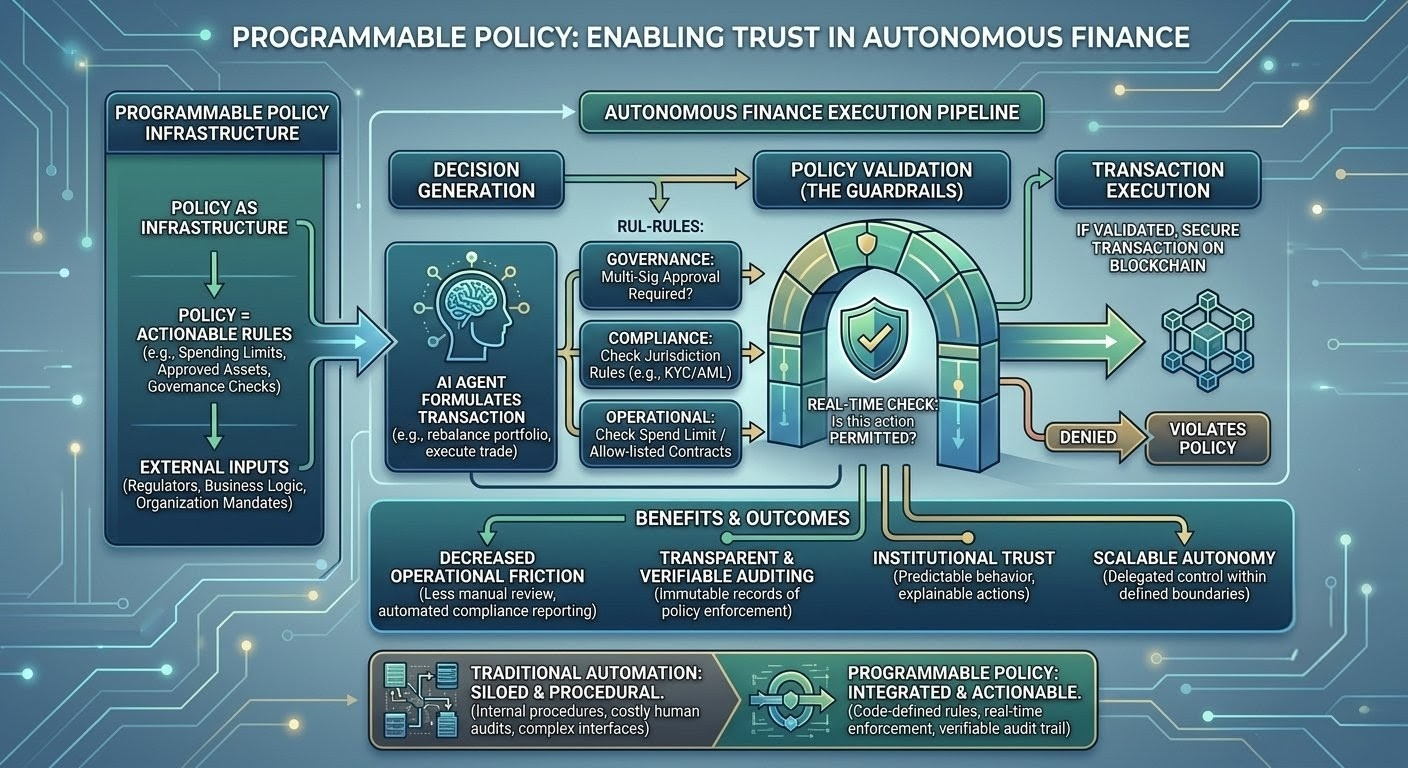

If an AI is managing capital, it shouldn't just know how to execute a transaction. It should also know the conditions under which that transaction is allowed to happen. Maybe there's a spending limit. Maybe certain assets are off-limits. Maybe larger transactions require additional approval. Maybe specific jurisdictions require different rules. These kinds of boundaries already exist in the real world. The challenge has always been making them enforceable without slowing everything down.

That's where programmable policy starts to make sense.

Instead of treating compliance and governance as something that happens after an action, the rules become part of the action itself. The system isn't just asking whether something can happen; it's checking whether it should happen according to the policies that were defined beforehand.

That feels much closer to how mature financial infrastructure actually works.

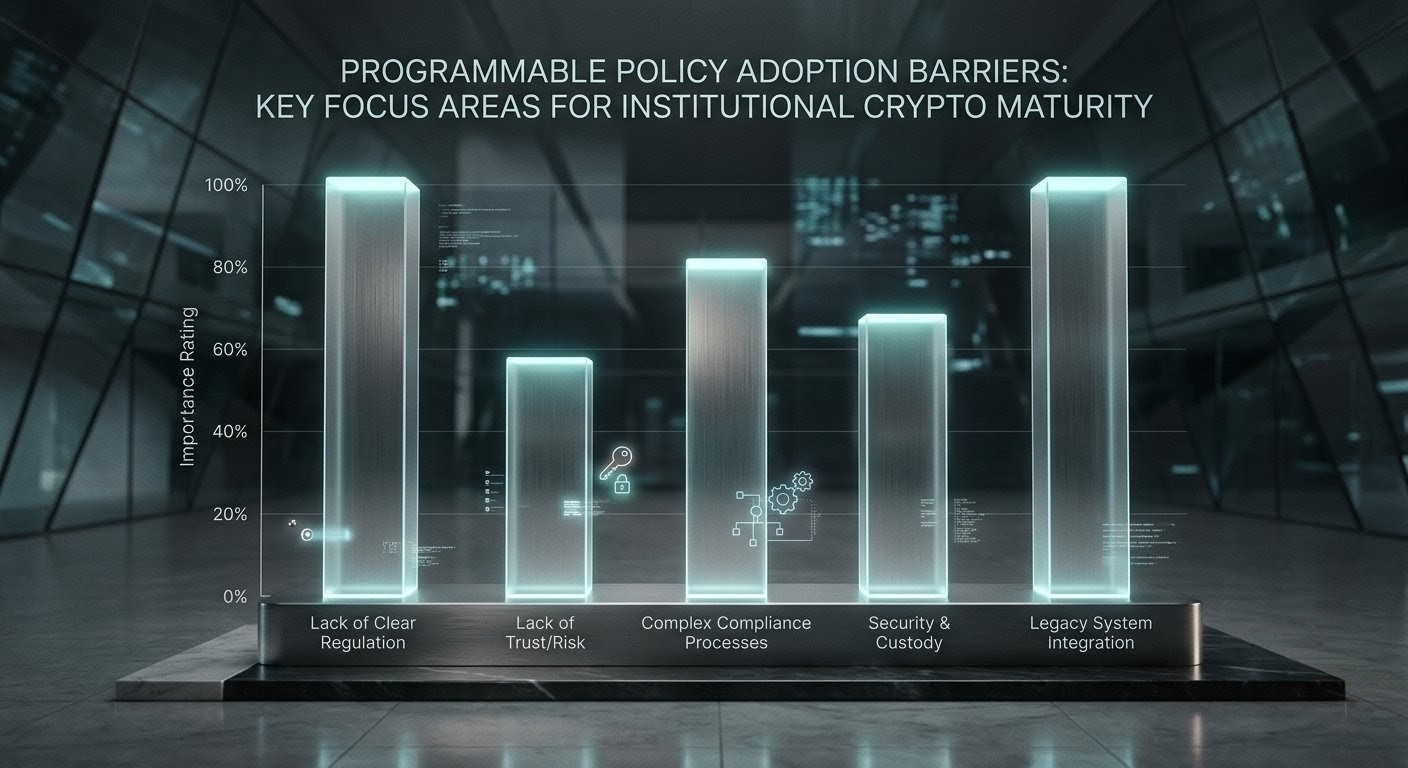

Something else that often gets overlooked is the cost of trust. Moving money isn't always the expensive part. Proving that it was moved correctly is. Banks, investment firms, and payment companies spend enormous amounts of time and money on audits, approvals, reconciliation, reporting, and compliance. Those processes exist because accountability matters whenever financial decisions are automated.

If infrastructure can make those rules programmable instead of procedural, it could remove a surprising amount of operational friction. Not by eliminating regulation, but by making compliance more consistent and easier to verify.

Of course, I don't think software can replace human judgment entirely. Real life is messy. Regulations change, businesses evolve, and no written policy can anticipate every possible situation. That's why I'm naturally skeptical whenever I hear people describe autonomous finance as if it can eventually run without oversight.

History usually teaches the opposite lesson.

Financial systems rarely fail because they weren't automated enough. They fail because someone assumed automation no longer needed supervision.

That's why I see Newton Protocol less as an AI project and more as an attempt to build better infrastructure for responsible automation. Whether it succeeds won't depend only on technical performance. It will depend on whether developers actually find it useful, whether institutions are comfortable building on it, and whether its policy framework can adapt as laws and business requirements inevitably change.

Those are difficult challenges, but they're also the ones that matter.

I don't think the first users of this kind of infrastructure will be everyday crypto traders looking for the next opportunity. They'll probably be developers building autonomous applications, fintech companies experimenting with AI, digital asset managers, and organizations that already operate under strict governance requirements. Those users aren't looking for unlimited freedom. They're looking for automation they can trust, explain, and defend.

In the end, that's why Newton Protocol stands out to me. It's trying to solve a quieter problem—one that doesn't generate the same excitement as faster blockchains or more advanced AI, but becomes impossible to ignore as crypto matures. If programmable policy can become as fundamental as programmable money, projects like Newton could play an important role in connecting decentralized technology with the realities of regulation, business, and human decision-making.

Whether it succeeds is still an open question, and I think it's healthy to remain skeptical. But if crypto is ever going to support truly autonomous systems at scale, trust won't come from automation alone. It will come from the rules that quietly shape how that automation behaves.