Hyperliquid's core perpetuals business has roughly halved since its peak. But underneath that cooldown, a different kind of trading is quietly growing on the very same infrastructure.

Key Takeaways

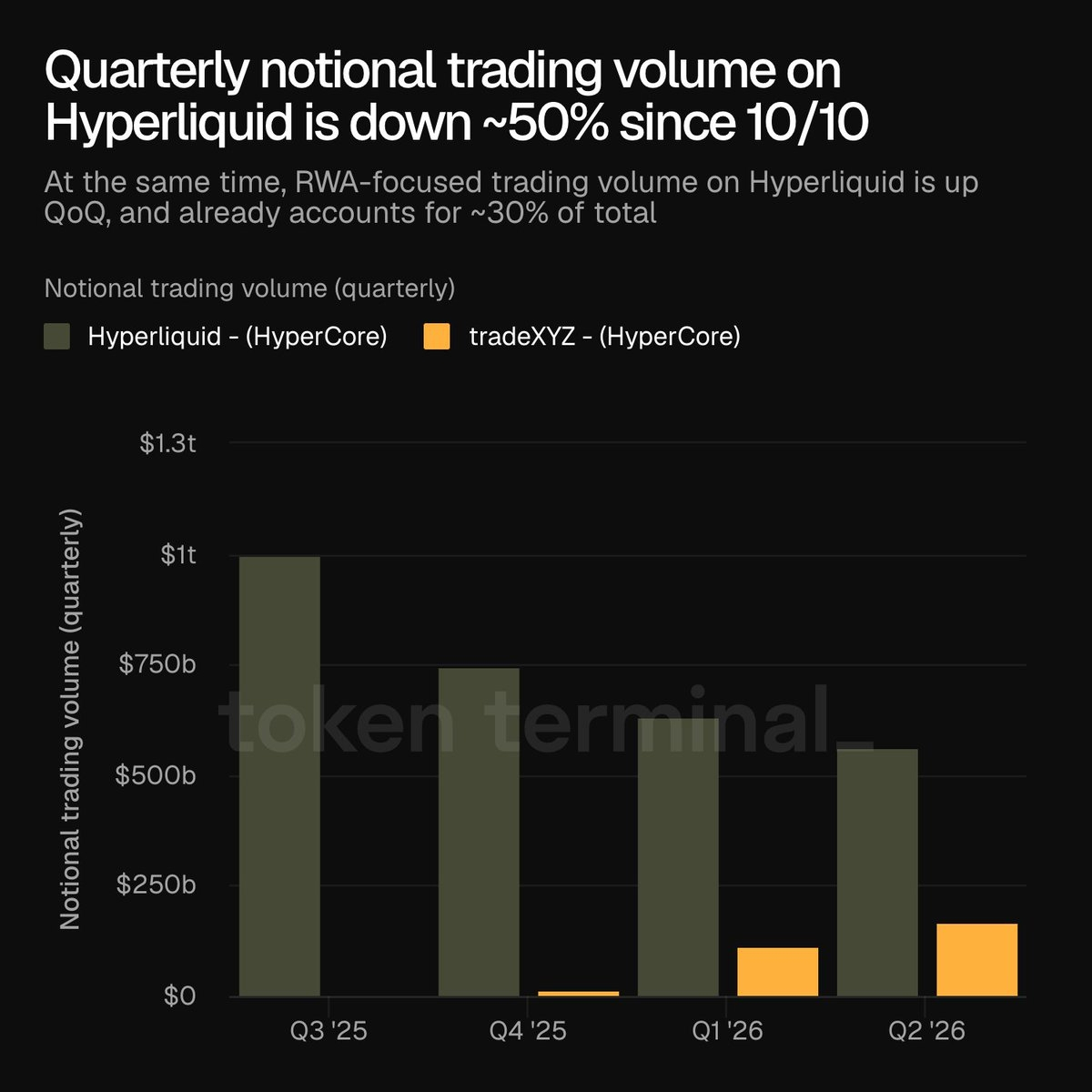

Hyperliquid's total notional trading volume is down roughly 50% since October.

RWA trading via tradeXYZ is up quarter over quarter, now about 30% of the total.

Both the core business and tradeXYZ run on the same engine, HyperCore.

RWA growth is softening the decline, not reversing it.

Since hitting its ceiling around the now-infamous October 10 crash, Hyperliquid's quarterly notional trading volume has been in a steady retreat. The data peaked near $1 trillion in Q3 2025, then slid to roughly $750 billion in Q4, around $600 billion in Q1 2026, and about $550 billion in Q2 according to data, shared by TokenTerminal. That's close to a 50% drawdown from the top.

None of this is mysterious. Hyperliquid built its name on crypto perps, and crypto perps cool when the broader market cools. The decline mostly tracks a quieter market, not a broken product. But the headline number isn't the interesting part. The interesting part is what's growing while the total shrinks.

The Silent Offset

Here's where the story turns. tradeXYZ, a trading venue focused on real-world assets, runs on the same engine that powers Hyperliquid's crypto markets, HyperCore. A year ago it barely registered. By Q1 2026 it was doing roughly $100 billion in notional volume, and by Q2 it had grown to around $150 billion, enough to account for close to 30% of total HyperCore volume.

Sit with how fast that happened. From a rounding error to nearly a third of the platform's volume in about two quarters. The same rails that process volatile crypto bets are now handling real-world-asset trading at meaningful scale, through a completely separate front-end.

The Tension in the Data

Now the part that keeps this honest, because it's easy to overhype. tradeXYZ is not rescuing Hyperliquid's volume. The total is still falling quarter over quarter even with the RWA growth counted in. The new vertical is softening the decline, not reversing it. In fact, because the overall total dropped by half while RWA grew its share to nearly a third, the core crypto business has actually shrunk by more than half on its own, with the RWA growth masking part of that slide.

So the net picture is still compression, just with a more interesting shape than before. Where Hyperliquid was once almost purely a crypto-perps venue, it's now a mixed platform, one whose volume is split between speculative crypto and tokenized real-world assets. That's a different company than it was a year ago, even if the top-line number is down.

Why It Actually Matters

Ultimately, the takeaway is about the infrastructure, not the headline. The most useful thing this data shows is that HyperCore can process more than volatile crypto perps, it can run real-world-asset trading at real scale through a separate front-end. For the underlying technology, that's a genuinely encouraging signal, because it means Hyperliquid's engine isn't a one-trick system tied entirely to crypto's mood.

That's also the bet worth watching. If the crypto market reheats and the RWA vertical keeps climbing, Hyperliquid would have two growth engines instead of one. If crypto stays cool, the question becomes whether RWA volume can grow fast enough to do more than cushion the fall. Either way, the diversification is real, and it changed quietly while everyone was watching the total volume drop.