In August 2025, the Trump administration reportedly acquired a 10% stake in Intel at $20.47 per share.

Today, the stock trades above $85.

That alone would mean the government’s position grew from roughly $8.9 billion to nearly $37 billion a return exceeding 315% in less than a year.

Now, on May 21, 2026, the administration appears to be repeating the same strategy but on a much larger scale.

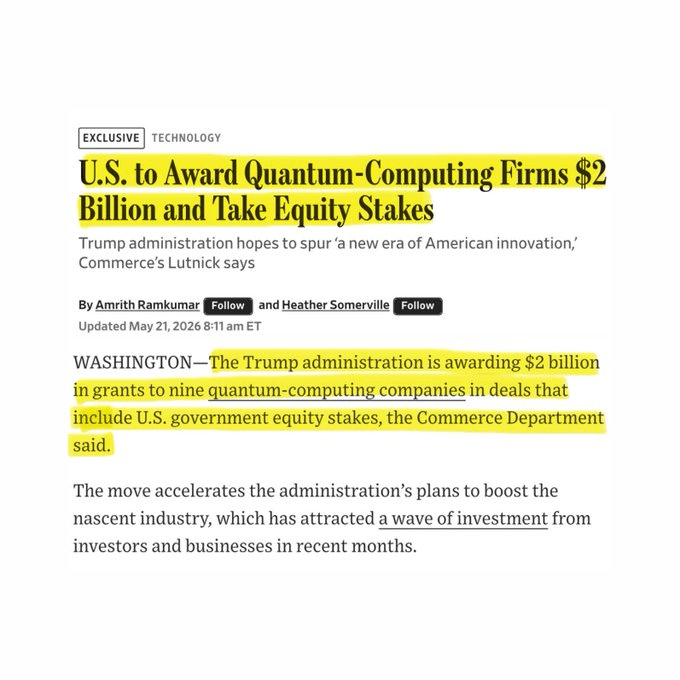

A new $2 billion initiative has been directed toward nine quantum computing companies.

And in return?

The government takes equity stakes in each of them.

IBM receives $1 billion, while committing another $1 billion of its own capital to build America’s first dedicated quantum chip fabrication facility in New York, called Anderon.

GlobalFoundries receives $375 million in exchange for 1% equity.

Rigetti, D-Wave, and Infleqtion each receive $100 million.

Australian startup Diraq receives $38 million.

The market reaction was immediate.

Rigetti surged 24%.

Infleqtion jumped 35%.

IBM rose 8%.

GlobalFoundries gained 11%.

D-Wave climbed 5.34%.

The market understood the message before most analysts did.

This is about far more than government subsidies.

The U.S. government is now behaving like a sovereign venture capital fund.

It identifies sectors considered strategically critical, injects capital into them, and positions itself to participate in future upside.

The money itself is not new.

Much of it originates from the CHIPS Act passed under Biden in 2022.

But the deployment model has completely changed.

Subsidies are becoming ownership.

The American taxpayer is becoming a shareholder.

And the real objective behind all of this?

The technology race with China.

Quantum computing is not a laboratory science experiment anymore.

IBM estimates the global quantum economy could reach $850 billion by 2040.

Whoever dominates this technology could eventually influence everything from banking systems to military encryption.

The United States cannot afford to leave this race entirely to markets or chance.

So Washington has decided to become a player not merely a referee.

What’s even more striking is that this model is expanding.

Positions in Intel. Investments tied to MP Materials and rare earth supply chains. Lithium Americas. Trilogy Metals.

The U.S. government is quietly building a strategic portfolio across industries considered essential weapons in the new Cold War.

And that raises the real question:

If the government itself is buying these sectors…

What does the policymaker see that the broader market still does not?

And in the end, who captures the greater upside?

The companies building the technology… or the state financing it?