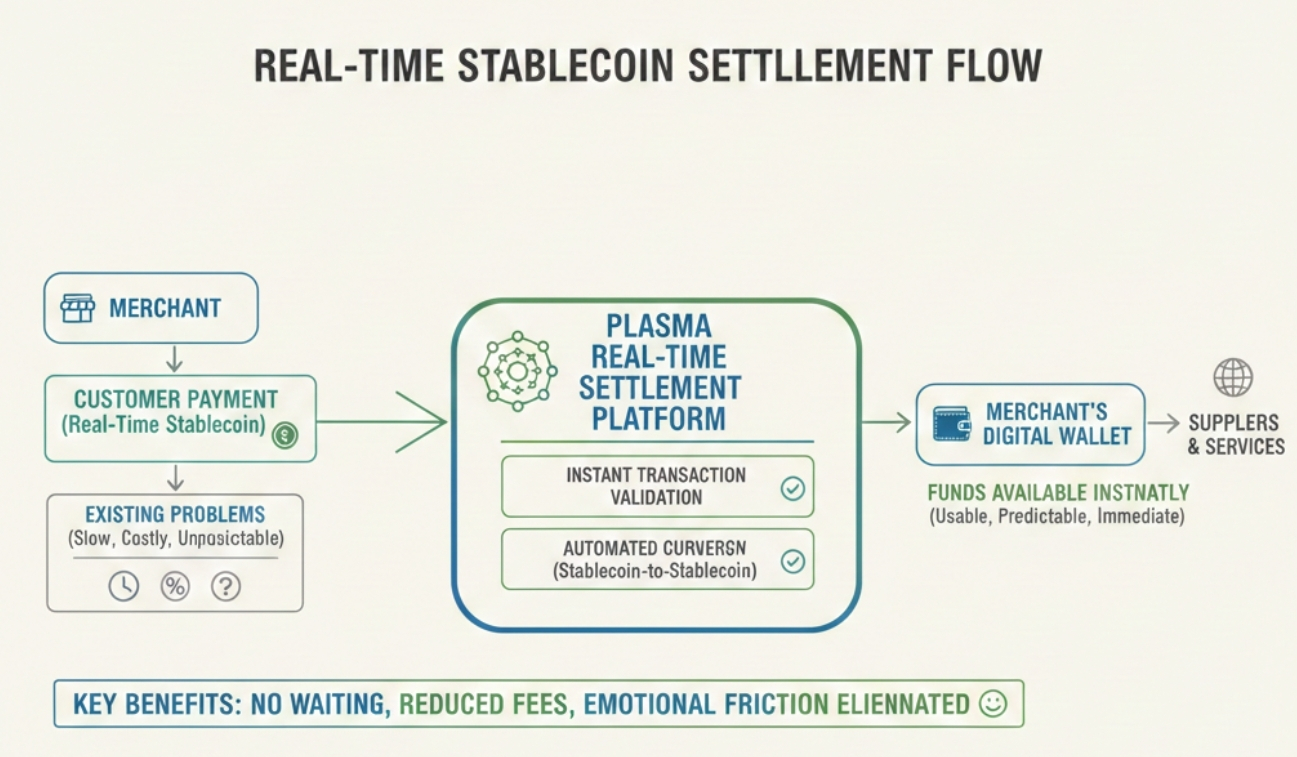

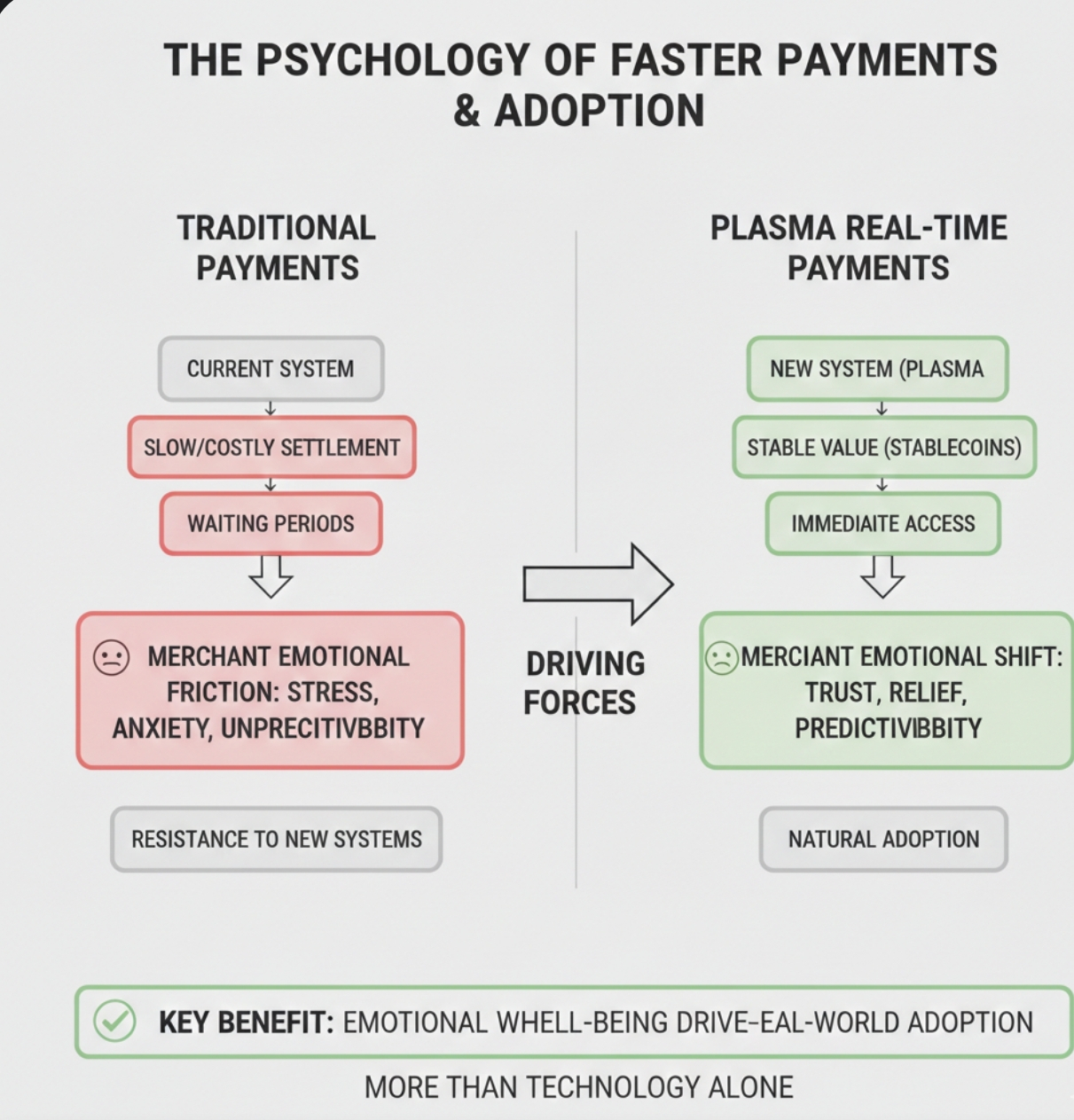

Plasma enters the conversation at a moment when merchants across the world are quietly rethinking how they get paid. Not because they want to experiment with new technology or chase crypto trends, but because they are simply tired of waiting. Waiting for cross border bank transfers. Waiting for settlement to finalize. Waiting for payment processors to clear funds. Waiting for currency conversions that slowly eat away at already thin margins. For many business owners, the most stressful part of a sale is not making it. It is receiving the money in a form that feels usable, predictable, and immediate. That emotional friction is what makes the idea of real time stablecoin settlement so powerful. It is not about hype or speculation. It is about removing the anxiety around getting paid.

Stablecoins solved one of the biggest problems in crypto years ago. They removed volatility. A dollar pegged digital asset offers stability that most cryptocurrencies cannot. Merchants do not want to receive payments in assets that swing wildly in value. They want something that holds steady. But stability alone never guaranteed adoption. The real world experience of using stablecoins often required extra steps, technical knowledge, and patience. Businesses operate on tight schedules and tighter margins. They do not have time to navigate complicated wallets, unpredictable fees, or slow confirmations. They want payments to arrive instantly and remain stable in value. They want a system that works in the background without forcing them to learn an entirely new financial language. This is where Plasma begins to feel less like a typical crypto project and more like a payment network designed for everyday commerce.

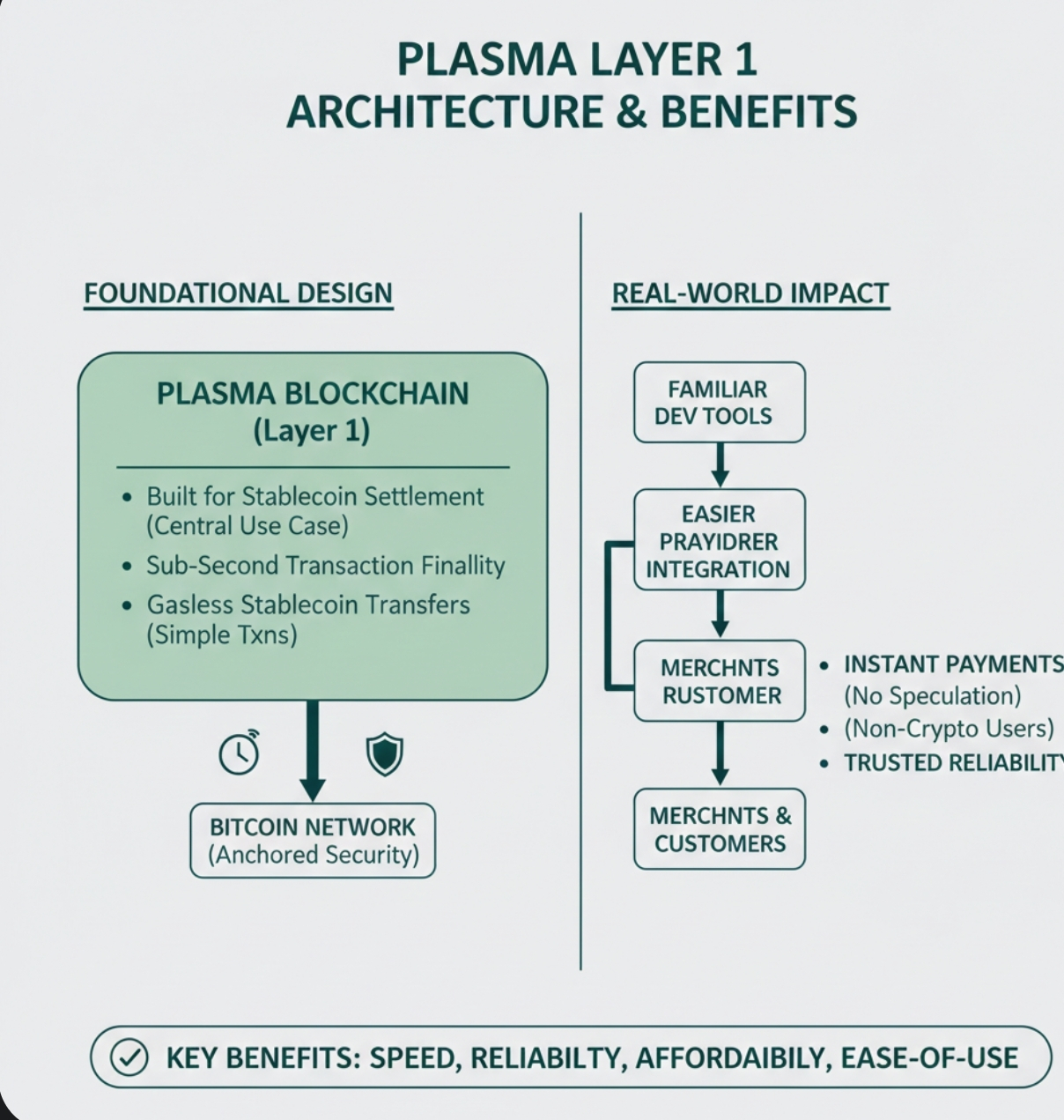

At its foundation, Plasma is a Layer 1 blockchain built specifically for stablecoin settlement. Instead of treating stablecoins as just another token on a general purpose chain, it treats them as the central use case. That shift in design philosophy matters more than it may appear at first glance. Sub second finality allows transactions to confirm quickly enough for merchants to treat them like real payments rather than speculative transfers. Full compatibility with familiar development tools makes it easier for payment providers and platforms to integrate without rebuilding their entire systems. Gasless stablecoin transfers for simple transactions remove one of the biggest barriers for non crypto users. By anchoring its security approach to Bitcoin, the network aims to borrow credibility from the most trusted chain in the space while focusing on speed and reliability for payments.

When looking at the broader market, the timing of this approach makes sense. Global commerce is increasingly digital and increasingly borderless. A freelancer in one country might work with clients across multiple regions. An online store can sell to customers worldwide from day one. Yet traditional payment systems were not built for this level of global interaction. International transfers can take days to clear. Fees accumulate at each step in the process. Currency conversions introduce uncertainty. For many individuals and businesses, stablecoins already act as a workaround because they move faster and hold value better than local currencies in some regions. The next logical step is making them seamless enough for merchants to rely on every day.

From an analyst perspective, reliable stablecoin settlement infrastructure could reshape how digital commerce operates. Payment networks that support real transactions create a different kind of value than networks driven purely by trading and speculation. Trading activity rises and falls with market sentiment. Merchant payments tend to remain consistent. Businesses process transactions daily regardless of whether the market is bullish or bearish. If stablecoin payments become embedded in retail and online commerce, the networks supporting them could benefit from steady usage rather than temporary spikes in activity.

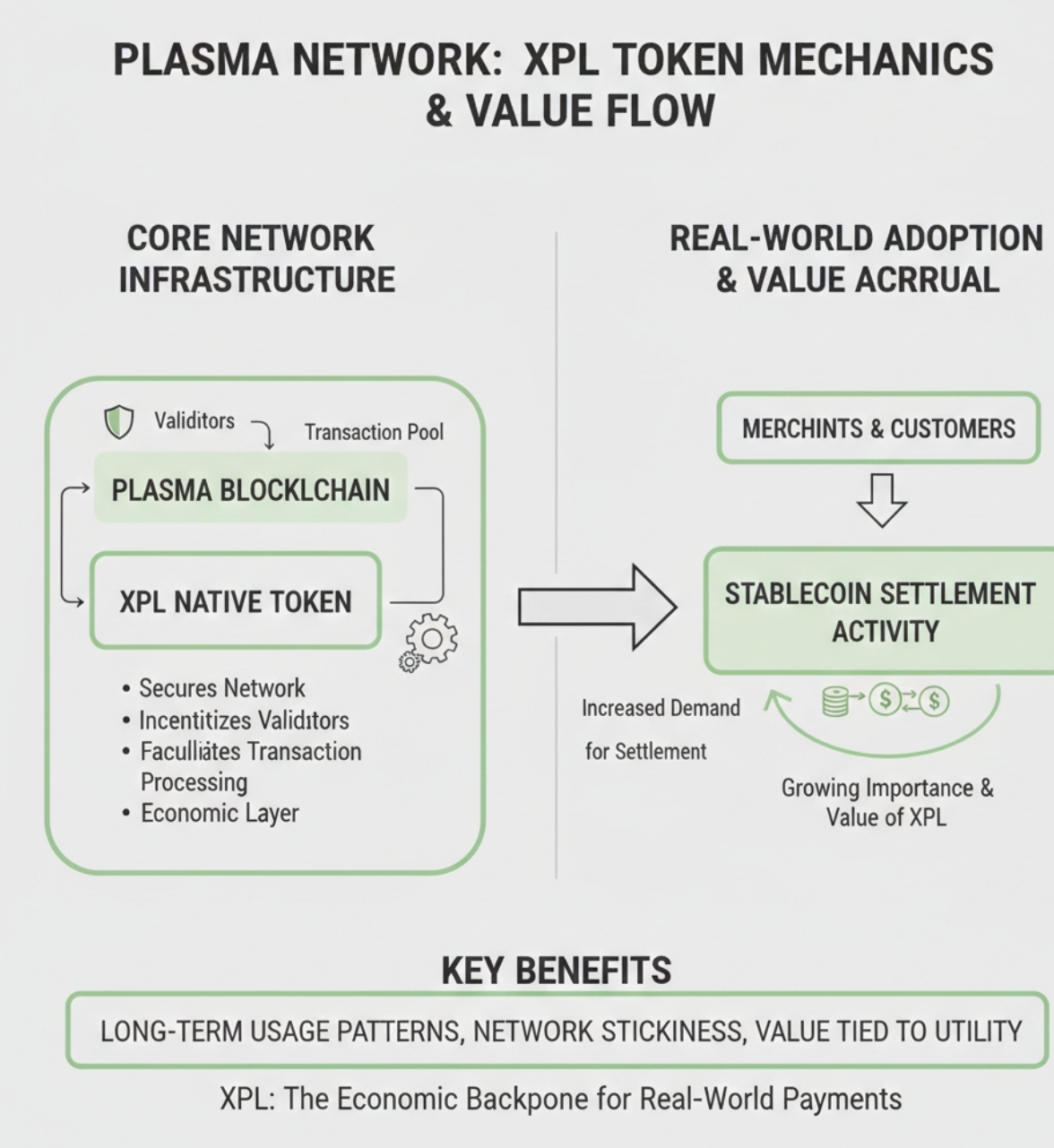

Investor psychology often gravitates toward fast moving narratives. Tokens tied to infrastructure rarely create immediate excitement. Yet history shows that payment rails and financial infrastructure often become extremely valuable once adoption reaches a certain threshold. Merchants do not switch payment systems easily. Once they trust a network with their revenue, they stay. That stickiness creates long term usage patterns that can outlast market cycles. In the context of Plasma, this is where the native token XPL fits naturally into the system. XPL functions as the economic layer that supports validators, network operations, and transaction processing. While merchants may interact primarily with stablecoins, the network itself relies on XPL to maintain security and performance. If settlement activity grows, the importance of the token grows with it because it underpins the infrastructure enabling those transactions.

There is also a human element that often gets overlooked in technical discussions. Running a business involves constant decisions around cash flow. When payments settle instantly, working capital becomes more flexible. Inventory can be ordered sooner. Employees can be paid without delay. Financial planning becomes easier because there is less uncertainty about when funds will arrive. These practical benefits matter more to merchants than technical specifications. If a network like Plasma can deliver consistent real time settlement, it addresses a real problem rather than offering a purely theoretical improvement.

The adoption path for merchant stablecoin payments will likely be gradual. Businesses rarely replace existing systems overnight. They test new options alongside traditional methods. If the new system proves faster, cheaper, and more reliable, usage grows organically. Payment providers and platforms will play a key role in this process. Integration into familiar checkout flows and accounting systems reduces friction for merchants. Over time, what begins as an alternative payment option can become a preferred method if it consistently delivers better results.

Of course, there are risks. Regulatory frameworks around stablecoins continue to evolve and could influence how merchants use them. Networks designed for settlement must maintain extremely high reliability because downtime or security issues could quickly erode trust. Competition from traditional fintech companies and other blockchain networks remains strong. Success will depend on execution, partnerships, and the ability to scale while maintaining low costs and fast confirmations. Recognizing these risks does not weaken the opportunity. It highlights the importance of careful development and real world testing.

Looking ahead, the broader trend toward digital payments shows no signs of slowing. Consumers expect instant experiences. Businesses seek efficiency and lower costs. Stablecoins offer a form of digital cash that can move globally without the same friction as traditional systems. The missing piece has been infrastructure optimized specifically for their use in commerce. Plasma represents one attempt to build that infrastructure from the ground up rather than adapting existing networks designed for other purposes.

If stablecoin settlement becomes as seamless as sending a message or swiping a card, the impact on global commerce could be significant. Small businesses could operate more easily across borders. Freelancers could receive payments without waiting days for bank transfers. Merchants in high inflation regions could accept stable currency without complex conversion processes. These scenarios highlight the practical value of reliable settlement rather than the speculative appeal of digital assets.

The most interesting aspect of this shift may be psychological. When merchants stop thinking about crypto and start thinking about faster payments, adoption becomes natural. They do not need to believe in a technological movement. They simply need a system that works better than the one they already use. When payments arrive instantly and remain stable in value, the emotional stress around settlement begins to fade. That emotional shift can drive adoption as much as any technical feature.

Plasma’s focus on stablecoin settlement positions it within this broader narrative. It is not trying to replace traditional finance overnight but to offer an alternative that feels practical and reliable for merchants operating globally. If stablecoins continue to gain traction as a medium of exchange, networks optimized for their settlement could become essential components of digital commerce. The transition will be gradual, but gradual adoption often leads to lasting change.

In a market often dominated by hype cycles, the idea of building infrastructure for everyday payments may seem understated. Yet the most meaningful transformations often happen quietly. When a merchant receives payment instantly and can use those funds immediately, the technology behind that transaction becomes invisible. What remains is a smoother business experience and greater confidence in cash flow. If Plasma and similar networks can deliver that consistency, they may play a role in shaping how money moves in the digital economy for years to come.